Part of our Investment Performance Metrics guide

Excess Return Definition

Excess return refers to the return from an investment above the benchmark. It indicates whether the investment is outperforming the market or not. Hence it helps in evaluating the investment performance. Alpha is an example of this metric.

In simple words, it is the difference between total return and expected return. Obtaining factors like beta value and the risk-free rate are important for its calculation. The value can be positive, zero, or negative. Its calculation and forecasting are becoming important in quantitative trading and stock price prediction based on machine learning.

- Excess return refers to the return from an investment above the benchmark.

- The measure helps evaluate the investment performance and checks the presence of high return, compensating for the additional risk.

- It indicates whether the investment is outperforming the market or not. A positive value reflects the outperformance, whereas a negative value indicates the underperformance.

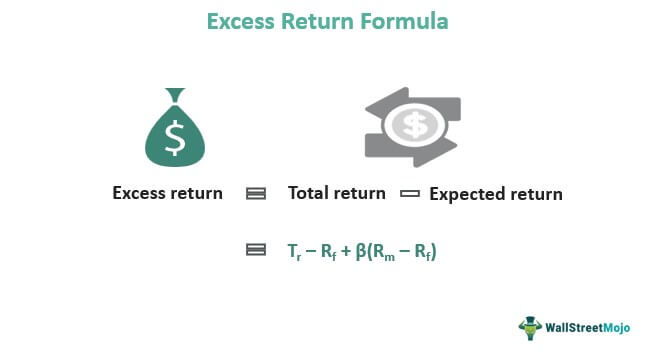

- The formula to calculate is: Excess return = Total return – Expected return = Tr – (Risk-free rate – (Beta*Market risk premium)) = Tr – Rf + β(Rm – Rf)

Excess Return Explained

Excess return is an important investment term. It is the additional return on an investment by which it rises above the benchmark rate. Generally, the benchmark is a rate based on U.S. Government securities. Also, the additional return indicates that the investment contained an additional risk of loss because the return potential increases with risk. Hence pointing to the risk-return trade-off.

A high alpha or excess return value is always good. If this value is high for a specific mutual fund, it attracts investors. Fund managers, through careful analysis, select the assets and incorporate diversification to optimize the portfolio and generate higher alpha. A high alpha of the fund indicates its outperformance against the benchmark, and a negative value indicates the underperformance. An outperformance is always attributed to the fund manager’s skills and asset selection strategies. The value is always calculated under the capital asset pricing model (CAPM).

An example of an investment option mostly exhibiting high alpha is MBS (Mortgage-backed securities) in the United States. Different factors drive the alpha in the case of MBS like new home sales, industrial productions, refinancing proxy, etc. Furthermore, in a highly volatile market, various factors contribute to alpha. For example, there are scenarios of mispricing securities due to over-reacting or under-reacting to any piece of information and high returns due to social media influence like in the case of meme stocks, etc.

Excess Return Formula

The formula based on the CAPM is the following:

Expected Return = Risk-free rate + (Beta*Market risk premium)

= Rf + β(Rm – Rf)

Excess return = Total return – Expected return

Applying the expected return formula to the above:

= Tr – Rf + β(Rm – Rf)

Here,

- Rf: Risk-free rate

- β: Beta of the security

- (Rm – Rf): Market risk premium

- Rm: The expected return of the market

- Tr: Actual or total return from the security

The Sharpe ratio is another essential performance metric, often known as the Sharpe index. It may assess the performance of investment while accounting for risk. The greater the ratio, the better the investment. The Sharpe ratio is calculated by dividing the “Portfolio return – Risk-free rate” over a particular period by the standard deviation of the portfolio’s excess return.

Sharpe ratio = (Portfolio return-Risk-free rate) / Portfolio Standard Deviation

Calculation Example

Let’s consider an example to understand how to calculate excess return.

Kate is interested in risk-free Treasury Bills but wants to explore other investment opportunities. She has surface-level knowledge of the stock market. Kate knows that the stock market can be risky; with her rudimentary understanding, she is scared of a big market crash and losing her hard-earned money. But at the same time, she is also tempted to get a much higher return than T-Bills when the market is strong and moves up.

Kate is curious about how much extra return she can get by investing in a mutual fund instead of a T-bill. Kate notices that a Mutual Fund, “ABC,” had a return of 10% last year. The risk-free rate on T-Bills was only 4%, which means that the additional return enjoyed by the investors of the ABC mutual fund are:

Excess returns = Total return – Expected return

- =10% – 4%

- = 6%.

Kate missed a 6% return by letting her money stay invested in T-Bills.

Excess Return vs. Total Return

Both evaluate performance. Excess return value depicts an index’s or investment’s total return after deducting the benchmark value. When an investment outperforms the market, this occurs. Its value will be zero If no outperformance or underperformance is exhibited. On the other hand, the total return is the actual rate of return on an investment over a specified period considered. Total return includes interest, capital gains, dividends, other distributions, etc., earned during the assessment period.

Frequently Asked Questions (FAQs)

What is the excess return of the stock?

It refers to the return exceeding the benchmark return rate. It is calculated by deducting the expected return from the total return. Using it helps in the investment’s performance evaluation process, and it acts as an input to investment decision-making.

What is the difference between excess return and total return?

When an investment beats the market, the excess return value is the return of an index or investment after removing the benchmark value. In contrast, the total return is the actual rate of return on investment.

Is excess return the same as Alpha?

It also refers to and is close to the concept of alpha, which defines the investment’s ability to beat the market. It showcases how much the asset has outperformed the benchmark index. Alpha can be negative or positive.

Recommended Articles

This has been a Guide to What is Excess Return. We explain how to calculate it using the formula, example, and vs. total return. You can learn more from the following articles –