Part of our Fixed Assets and Depreciation guide

What is the Capital Expenditure Formula?

Capital Expenditure is the total amount that a Company spends to buy & upgrade its fixed assets like PP&E (Property, Plant, Equipment), technology, & vehicles, etc. The formula of Capex is the addition of net change in Property Plant and Equipment (PP&E) value over a given period to the depreciation expense for the same year.

The incorporation of the net capital expenditure formula enhances the competitiveness and long-term productivity of the organization. It attracts growth through investments in assets such as machinery, infrastructure, and technology. However, the risk of over-leveraging and locking up a sizable amount of resources is always a problem in this regard, as market volatility and other such factors can seriously hamper the returns from such investments.

Key Takeaways

- The capital expenditure (CapEx) formula calculates how much a company spends on acquiring or upgrading long-term assets, such as property, plant, and equipment (PP&E).

- The formula for capital expenditure is: CapEx = Ending PP&E – Beginning PP&E + Depreciation.

- Capital expenditure represents investments made by a company to maintain or expand its operations, improve efficiency, or support future growth.

- Analyzing capital expenditure helps assess a company’s commitment to long-term investments, ability to generate future cash flows, and strategic focus.

Capital Expenditure Formula Explained

Capital expenditure formula is applied to expenses incurred by a business or organization towards pivotal aspects that influence the long-term financial growth and competitiveness of the company. Also referred to as Capex, it involves a significant amount of investment in assets that generate value over an extended period.

The assets in discussion here could be machinery, facilities, technology, or infrastructure such as buildings, offices, or plants. These expenditures are imperative for organizations as these become the tools for the production of their products or services that in-turn generate revenue, and ultimately profits.

The importance of applying the net capital expenditure formula is made clear when it shows the long-term productivity of the organization and the longevity of its competitiveness in the market. It shows how the company can allocate resources to a particular asset that can generate significant returns in the future for the company.

For instance, for a manufacturing unit, inclusion of a conveyor belt could be a significant cost. However, the increased pace of production and packing can lead to higher productivity and ultimately more sales and profits.

However, it is also important to maintain a sense of balance within the organization, as overinvesting in Capex could limit the liquidity of the company, and underinvesting could lead to underutilization of the funds available at the company’s disposal.

Moreover, technological advancements and market volatility make it trickier to invest in such expenses as the return on such huge investments becomes all the more uncertain. Therefore, a clear understanding of the business, market, and the external business environment is vital to ensure the effective utilization of resources.

Capital Expenditure Formula Explanation in Video

Formula

The total capital expenditure formula is as follows:

CAPEX Formula = Net Increase in PP&E + Depreciation Expense

How To Calculate?

The calculation of thenet capital expenditure formulacan be done by using the following three steps:

- Firstly, the PPE value at the beginning of the year and the end of the year is collected from the asset side of the balance sheet. Then, the net increase in PPE value is calculated by deducting the PPE value at the beginning of the year from the PPE value at the end of the year.

- Net increase in PPE = PPE at the end of the year – PPE at the beginning of the year

- Next, the accumulated depreciation at the beginning and the end of the year is collected from the balance sheet. Then, the depreciation expense during the year is calculated by deducting the accumulated depreciation at the beginning of the year from the accumulated depreciation at the end of the year. Conversely, the depreciation expense incurred during the year can also be directly collected from the income statement, which is captured as a separate line item.

- Dep. expense = Accum. Dep. at the end of the year – Accum. Dep. at the beginning of the year

- Finally, the capital expenditure incurred during the year can be calculated as either,

Capex Formula = (PPE at the end of the year – PPE at the beginning of the year) + (Accum. dep. at the end of the year – Accum. dep. at the Beginning of the year)orCapital Expenditure Formula= (PPE at the end of the year – PPE at the beginning of the year) + Dep. expense

Examples

Let’s see some simple to advanced examples to understand the calculation of Capital Expenditure.

Example #1

Let us take the example of the company ABC Ltd and calculation of capital expenditure in 2018 based on the following information:

- Depreciation expense is $10,500 in the income statement

- PP&E value at the end of 2018 is $45,500 on the balance sheet

- PP&E value at the beginning of 2018 is $40,000 on the balance sheet

Therefore,

Net increase in PP&E = PP&E value at the end of 2018 – PP&E value at the beginning of 2018

Consequently,

Capital Expenditure (capex) Formula = Net increase in PP&E + Depreciation expense

Therefore, the calculation of Capital Expenditure incurred during 2018 is $16,000.

Example #2

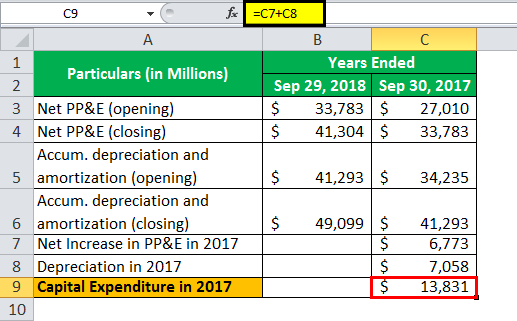

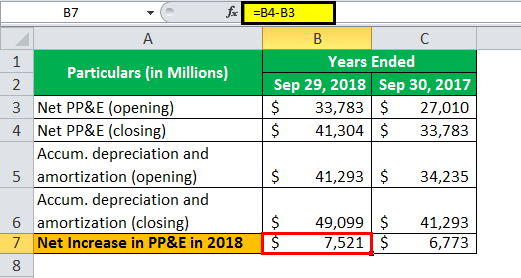

Let us take the example of Apple Inc. and the calculation of capital expenditure in 2017 and 2018 based on the following information:

| Particulars (in Millions) | Sep 29, 2018 | Sep 30, 2017 |

|---|---|---|

| Net PP&E (opening) | $33,783 | $27,010 |

| Net PP&E (closing) | $41,304 | $33,783 |

| Accum. depreciation and amortization (opening) | $41,293 | $34,235 |

| Accum. depreciation and amortization (closing) | $49,099 | $41,293 |

Net increase in PP&E in 2017 = $33,783 – $27,010

Depreciation in 2017 = $41,293 – $34,235

Consequently,

The Calculation of Capital expenditure in 2017 = $6,773 + $7,058

Again,

Net increase in PP&E in 2018 = $41,304 – $33,783

Depreciation in 2018 = $49,099 – $41,293

Consequently,

The Calculation of Capital Expenditure in 2018 = $7,521 + $7,806

Difference Between Capital Expenditure and Revenue Expenditure

Businesses have a set of expenses that are inevitable and cannot be ignored. The majority of such expenses are capex and revenue expenditures. Let us understand the differences between the two through the comparison below.

Capital Expenditure

- Involves significant ticket size in investments towards long-term assets that directly benefit the business.

- These expenses improve the overall efficiency and production capacity of the business.

- These costs are generally capitalized and are applicable for depreciation over their useful life.

- The primary aim is to equip the company with better resources to increase economic benefits for a prolonged period and remain competitive for a longer time frame.

- Examples include machinery, technology, buildings, office space, or a production plant.

Revenue Expenditure

- Revenue expenditures refer to the daily operational expenses incurred by the company that are necessary to sustain the business.

- These are short-term costs that do not involve the acquisition of long-term assets.

- These costs are accounted for immediately and are deducted from the current year’s revenue.

- The primary agenda of such expenses is to ensure the business operations run smoothly and generate immediate benefits.

- Examples of revenue expenditure include salaries, maintenance costs, and utilities.

Frequently Asked Questions (FAQs)

Why is depreciation included in the capital expenditure formula?

Depreciation is included in the formula because it represents the annual reduction in the value of long-term assets due to wear and tear or obsolescence. Including depreciation in the procedure accounts for the impact of asset depreciation on the company’s capital expenditure.

What is the significance of calculating capital expenditure?

Calculating capital expenditure helps evaluate a company’s spending on long-term assets and its commitment to maintaining or expanding its operations. It provides insights into the company’s investment strategy, future growth prospects, and financial health.

Can capital expenditure be negative?

Yes, capital expenditure can be negative in some instances. A negative capital expenditure indicates a reduction in long-term assets, which can occur when a company sells or disposes of existing assets. Negative capital expenditure implies a decrease in investments in long-term assets.

How is capital expenditure different from operational expenses?

Capital expenditure represents investments in long-term assets that are expected to generate benefits over multiple accounting periods. Operational expenses, on the other hand, are day-to-day expenses incurred to support the business’s ongoing operations.

Recommended Articles

This article has been a guide to Capital Expenditure Formula. Here, we explain how to calculate it, give examples, and compare it with revenue expenditure. You can learn more about financial analysis from the following articles –