Part of our Fixed Assets and Depreciation guide

What Is Capitalized Interest?

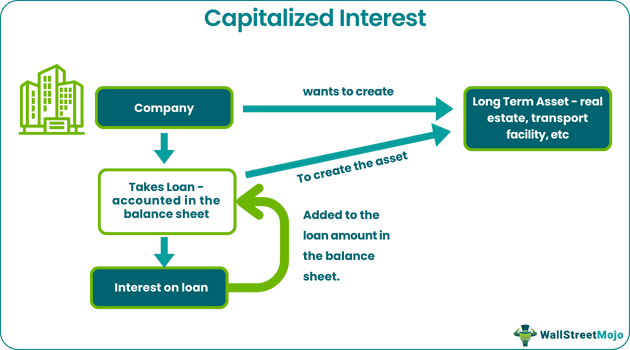

Capitalized interest is the cost of borrowing incurred by the company to acquire or construct the long term asset to be used in the business and is added to the value of the asset to be shown in the balance sheet of the company instead of showing it as an interest expense in the company’s income statement.

In simple words, Capitalized Interest is interest accrued during the construction of long-term assets. Therefore, it is included as the initial cost of assets on the balance sheet instead of being charged as interest expense on the income statement. The Generally Accepted Accounting Principles (GAAP) allow this method for companies that take loans for long-term assets.

How Does Capitalized Interest Work?

Capitalized interest on loan is the interest part of a loan taken for the purpose of building a long-term asset for business use and the interest is shown in the balance sheet instead of the income statement as an expense.

This method is useful only if it increases the value of the company’s financial statements. The interest expense is not reported in the income statement, whereas the capitalized interest is added to the cost of the long-term asset. It helps in raising the fixed asset’s total value.

Under the accrual basis of accounting, it is reported in the balance sheet as the total amount of fixed assets. An organization using a construction loan to build its corporate headquarters is another example of such a situation.

It becomes a part of the long-term asset and is depreciated over the useful life as a depreciation expense.

Therefore, capitalized interest on loan is part of the historical cost of setting the acquiring assets up for their intended use. The GAAP allows firms to avoid expensing interest on the debt. Many companies finance the construction of long-term assets with debt and include it on their balance sheets as a component of the historical cost of long-term assets. Various production facilities, ships, and real estate involve long-term assets for which capitalized interest accounting is allowed. In inventories that are manufactured repeatedly in large quantities, capitalizing interest is not permitted for them.

Capitalized Interest Video Explanation

Features

- Capitalizing interest helps a user of financial statements, from the perspective of accrual accounting, to better allocate costs to earnings in the periods when an acquired asset is being used and obtain an accurate measure of the acquisition cost of an asset.

- Capitalized interest balance can then be booked if an impact on a company’s financial statements is material; otherwise, there is no need.

- It has no immediate effect on a company’s income statement when booked, and it appears on the income statement through a depreciation expense instead.

- Since the last payment, it considers the total interest it owes on a loan balance or long-term asset. Adding the total interest owed to the total cost of the loan balance or long-term asset capitalizes it.

- For students to defer the loan, Capitalized Interest is the most common way where interest is added to the principal of the loan, which increases the interest owed monthly.

How To Calculate?

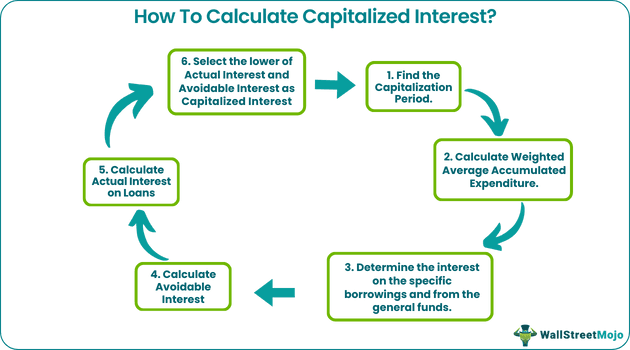

It can be calculated using the following steps –

Below are the steps for capitalized interest accounting –

- Find the Capitalization Period – The first step to calculate capitalized interest is to understand the time period until when the construction of the fixed asset will take place and when the asset will be ready for use. Capitalization of borrowing costs terminates when the asset has been prepared for its intended use and has substantially completed all activities needed. The capitalization period will not be extended by work on minor modifications. If the entity can use some parts while construction continues on other parts, it should discontinue capitalization of borrowing costs on the parts it completes.

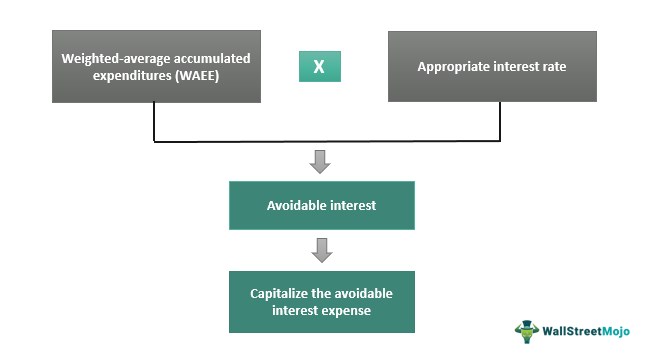

- Calculate Weighted Average Accumulated Expenditure – It is the product of the expenditure for constructing a fixed asset and is time-weighted for the accounting year. Weighted Average Accumulated Expenditure = Expenditure x (months in capitalization/12)

- Determine the interest in the specific borrowings and from the general funds – Suppose, the loan was specifically taken for the construction of fixed assets. In that case, the actual borrowing cost incurred is the borrowing cost to capitalize minus any investment income earned from the interim investment of those borrowings. For general corporate needs, borrowings may be handled centrally and could be obtained via a variety of debt instruments. During the period applicable to the asset, in this case, gain an interest rate from the weighted average of the entity’s borrowing costs. Using this method, the number of allowable borrowing costs at the entity’s total borrowing costs during the applicable period.

- Calculate Avoidable Interest

- Calculate Actual Interest on Loans – The actual interest on the overall loan is also straightforward. We can calculate capitalized interest directly, multiplying the corresponding interest rate by the debt raised.

- Select the lower of Actual Interest and Avoidable Interest. – Capitalized Interest = Lower (Actual Interest, Avoidable Interest)

Example

RKDF construction started the construction of a building that is to be used for production. The construction of the building will end by 31st December, and the building will be ready to use.

The following Debt was outstanding from 1st January 2017.

- $60,000 at a 10% interest rate (taken for the specific purpose of constructing the building)

- $75,000 at an 8% interest rate (general loan)

The following payments were made for the construction of the building –

- 1st February 2017 – $50,000

- 1st August 2017 – $75,000

Calculate Capitalized Interest?

Step 1 – Capitalizion Period

As given in the information above, the capitalization period will be from 1st January 2017 to 31st December 2017.

Step 2 – Calculate Weighted Average Accumulated Expenditure.

Weighted Average Accumulated Expenditure = 50,000 x (11/12) + $75,000 x (5/12) = $45,833 + $31,250 = $77,083

Step 3 – Determine the interest in the specific borrowings and from the general funds.

- $60,000 at a 10% interest rate (taken for the specific purpose of constructing the building)

- $75,000 at an 8% interest rate (general loan)

Step 4 – Calculate Avoidable Interest

Avoidable Interest = = $60,000 x 10% + (77,083 – $60,000) x 8% = $6000 + $1,367 = $7,367

Step 5 – Calculate Actual Interest on the Loans

Actual Interest on the Loans = $60,000 x 10% + $75,000 x 8% = $6,000 + $6,000 = $12,000

Step 6 – Lower of Actual Interest and Avoidable Interest

Capitalized Interest = ($7,367, $12,000) = $7,367

Capitalized Interest Vs Accrued Interest

Capitalized interest balance is one that is unpaid and added to the loan amount whereas accrued interest is the interest that the borrower is yet to pay. Some differences between them are as follows:

| Capitalized Interest | Accrued Interest |

|---|---|

| It is added to the loan amount on the balance sheet. | It is shown as interest expense in the income statement |

| It is related to loans for a long-term assets. | It is related to any kind of loan. |

| It is depreciated over time. | The borrower pays the interest at a regular interval |

Recommended Articles

This has been a guide to what is Capitalized Interest. We explain it, with examples, how to calculate, difference with accrued interest and features. You can learn more about accounting basics from the following articles –