Part of our Fixed Assets and Depreciation guide

What Is Capitalization Cost?

Capitalization Cost is an expense that the company makes to acquire an asset that they will use for their business, and such costs are shown on the company’s balance sheet at the year-end. These costs are not deducted from the income, but they are depreciated or amortized.

It helps the organization when it comes to investment, which the company makes in big assets, and that asset qualifies; the criteria should be capitalized. Still, on the contrary, the company should take extra care while finalizing its accounts because all big expenses related to the assets cannot be considered Capitalization Costs. That has to be expensed off during the period it is incurred.

Capitalization Cost Explained

The term capitalization cost refers to the expense incurred in the business for acquisition of fixed cost. The value is added to the balance sheet. The acquisition can be in the form of purchase or building it for the purpose of growth and expansion.

Net capitalization cost is considered to be a fixed asset which has a depreciation or amortization cost that is expense over the life of the asset. But even in some cases, the items like wage and salary is also capitalized.

Capitalization is done for assets shown in the fixed asset in the balance sheet. Then they are depreciated over a period. It is an expense to acquire the asset to put it to use in the business. There are several expenses that a company incurs.

Therefore, the asset purchased is expected to give benefit and generate revenue over a long period of time. The cost incurred during building construction is a perfect example of the same, where the cost of construction and the interest payment on borrowed amount, both are capitalized. Sometimes assets like machinery and plant are renovated or upgraded to bring them to a working condition. For the purpose of net capitalization cost, there may be various charges like installation cost, labor and transportation charges, purchase of latest machinery parts, chemicals etc, which are required to upgrade it. These expenses are often capitalized in the balance sheet.

The concept follows the matching principle according to which cost incurred while buying or setting up of the asset should match with the revenue earned from it. The process allows companies to spread heavy expenses over a long period of time due to which the company can avoid showing a huge and substantial cost incurred during one financial year, which may adversely affect profitability.

Capitalization Vs Expensing Explanation Video

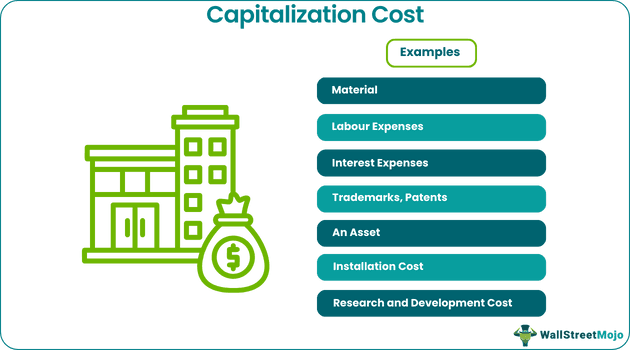

Examples

Let us understand the concept with the help of some examples.

Example #1

- Material is to be used to construct the asset, which is capitalized over the years.

- Labour Expenses for the work of completion of the fixed asset construction.

- Interest Expenses are also an example of capitalization if the interest is associated with the loan element used to purchase the asset.

- Trademarks, Patents are also capitalized because the amortization will be calculated and deducted from them every year.

- An Asset that the company is purchasing will be put to use.

- Installation Cost associated with the asset, if any;

- Research and Development Cost in the later stages of the software development company.

Example #2

Suppose a company makes a payment of $ 10000 on paying salaries to their employees or paying rent of the business premises, then it is not a capitalization cost. It is a normal expense that a company will incur.

However, suppose the company makes a $10000 payment to buy a machine that it will use in the business. It is a capitalization of the cost of the company. It will get depreciated over the useful life of the asset. Therefore, whenever the company invests money to acquire an asset that will be useful for the company, which is considered a capitalization cost.

How To Calculate?

- The asset is purchased for the company and will be use in the business.

- Determine the approx useful life of the asset or the duration of the asset in which it can be used.

- Consider the salvage value of the asset as per the market condition and the asset’s condition.

- Add up all the expenses associated with the asset to make it useful for the organization, for example, maintenance, repair, oiling expenses, etc.

- Calculate the entire interest element associated with the loan if taken to acquire the asset.

- Now we can calculate it by subtracting the profits from the cost associated with the asset.

- We calculate it as a percentage of the total cost, and from there, we can determine the asset’s present value.

Journal Entry

→ Explore all 30 Journal Entries articles

Let us understand the journal entry used for the purpose.

We treat it as an asset for the company, which will be depreciated. In the books of accounts, we have to debit the asset with the purchase amount and credit the account which paid for the asset, i.e., Cash or Bank a/c.

Reduction

Since the cost is ultimately a cash outflow for the company, even though it is spread out over a long period to reduce its negative effect, it is necessary to identify ways and means to reduce it or keep it under control so that the financial resource allocation is done in an optimum manner in various areas of the business.

In case of borrowing, the borrower has to make a down payment that reduces the total amount required as loan. Therefore, a great way to reduce the capitalization cost of buying an asset like real estate by taking loan is to make maximum possible down payment. The overall financing cost is lowered due to less loan and less interest payment.

Heavy goods like vehicles, machinery are often leased instead of directly buying them. Leasing requires less financing because it is similar to renting, which is suitable for borrowers with limited budget. In lease, the depreciation is to be charged only for the number of years of leasing.

It is also necessary to do some negotiation while purchasing any asset that will be capitalized. Many financial institutions offer rebates or trade-in allowance or some kind of incentives and discounts to customers. This can bring down the cost significantly.

Thus, the above are some of the ways in which capitalization cost can be controlled or reduced to get a better deal.

Advantages

Some advantages of the concept are given below.

- It helps to enhance the company’s income because the costs capitalized for the assets will be depreciated over time. Thus this will help the company avoid taxes and thus helps in the profit maximization of the company.

- The companies are not required to book the expenses made for the asset, which is capitalized. Rather, the cost is equally distributed throughout the asset’s useful life.

- Capitalization enhances the asset’s value as well because it includes the asset value and the amount which is levied to bring the asset to its use, i.e., installation cost, shipping cost, etc.

- The capitalization will also have a positive impact on the cash flow because the capitalized costs will show a higher income earned in the year, there is an increase in the value of the asset, and the equity is lowered. Thus the cash flow will show a positive impact.

Disadvantages

Here are some disadvantages of the concept.

- It is not that beneficial when it comes to capitalizing on the interestto get the asset. The company cannot reduce the tax obligation since the interest payments get deferred over the period. The taxes levied may harm the income of the organization. The company will not be able to enjoy the tax benefit of that transaction.

- The company sometimes makes too much capitalization of its assets. It has been witnessed in the software companies that the management decides to capitalize on the entire software cost related to the research and development of the software. Whereas the early-stage research and development should be expensed off, and the rest can be capitalized, they show the entire research and development cost in their balance sheet and not in their profit and loss account statement.

- The companies invite the manipulations when it comes to deciding whether the cost is to be expensed off or should be capitalized. Thus, they end up making wrong accounting treatments.

It helps the organization when it comes to investment, which the company makes in big assets, and that asset qualifies; the criteria should be capitalized. Still, on the contrary, the company should take extra care while finalizing its accounts because all big expenses related to the assets cannot be considered Capitalization Costs. That has to be expensed off during the period it is incurred.

Recommended Articles

This article has been a guide to what is Capitalization Cost. We explain reduction of the cost & how to calculate it along with journal entry & examples. You can learn more about it from the following articles –