Part of our Fixed Assets and Depreciation guide

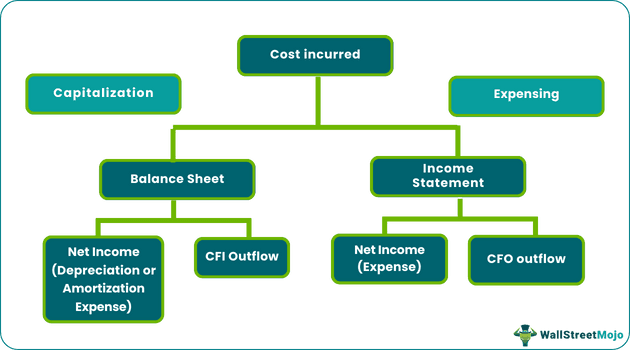

Capitalization vs Expensing

Capitalization is the recording of an expense or an asset. It is done when it is believed that the benefits of such expenses will be derived for an extended period. For instance, office goods are believed to get spent fast. Thereby, they are treated to be spent simultaneously. On the other hand, a vehicle is recorded as an immovable asset and expected to be spent significantly over time via depreciation. The vehicle is expected to get consumed over a much longer period than the office supplies.

Expensing assumes any expenditure like an operating expense instead of a capital investment. Considering taxation, an expense is reduced from income directly. Whereas an asset is depreciated or any business undertakes a series of reductions over the asset’s useful life.

Capitalization Example

Suppose a company buys a car worth $50,000 in 2017. Since the company has paid for this expense, should we take this expense ($50,000) in the Income statement for 2017, or should we record this expense as something else? You got it!

Let us assume that a car has a useful life of 10 years. The company can benefit from this car until the 10th year. Therefore it will not be wise to record all the expenditures in the Income Statement. Instead, we should capitalize on this expense of $50,000 and reduce it by the value derived each year.

The value derived each year = $50,000/10 = $5,000

Therefore, we record the expense of $50,000 in the asset at the beginning of 2017. During the year, we use $5000 worth of value, therefore the end of year Asset = $50,000 – $5000 = $45,000.

The above-discussed expense all through accounting is referred to as Depreciation.

Capitalization vs Expensing Explained in Video

Capitalization vs Expensing – Key Differences (Summary)

The major suggestion for choosing between expensing and capitalizing is to report profit every period. If one chooses to capitalize on any asset against expense, it leads to greater profits while successively leading to greater taxes and improved business value. However, selecting expenses for any asset rather than its capitalization would deliver just the opposite results.

| Capitalization | Expensing |

|---|---|

| Cost recorded as an asset on the balance sheet | Cost recorded as operating expenditure on the income statement |

| While capitalizing any cost and later amortizing it results in the cost distributed over a longer time period | Under normal conditions, the complete expense is incurred while making any purchase |

| For asset capitalization, it should possess a valuable life that covers more than the existing year. These assets must be capable of running the entire business. However, any inventory being sold to customers doesn’t qualify to become a capital asset. Fixed assets are generally considered like equipment or a range of intangible assets like patents or copyrights. Usually, fixed assets ought to be depreciated as against being amortized. | While starting or purchasing a business, IRS enables one to remunerate the business beginning or procurement costs. The expenditures made to consume a patent, copyright, trademark, or comparable rational property may be amortized. One may repay goodwill that is generally expected to be realized during sales owing to the ongoing usage of the reputation or name of any product or business that you intend to acquire. Generally, IRS allows one to repay geological expenditures that are intended to develop or locate petroleum wells all across the United States. One could even repay their research expenditures. |

| A General Rule: Any procurement beyond a specified dollar range is counted to be capital expenditure or capitalization | A General Rule: Purchasing lesser than the allocated dollar range is treated as an operating expenditure |

| As per accounting, upon an asset’s capitalization, it is assumed that the asset still has economic value, and it is believed to benefit prospective periods and thus is mentioned over a balance sheet. | An expense comprises of the core economic costs that are incurred by any business through daily operations for earning revenue. Every business is permitted to write-off all the tax-deductible expenditures on their specific returns for income taxes to minimize the taxable income, hence the tax liability. Most common business expenditures comprise of supplier payments, wages to employees, factory lease, and depreciation of equipment. |

A General Rule: Any procurement beyond a specified dollar range is counted to be capital expenditure or capitalization A General Rule: Purchasing lesser than the allocated dollar range is treated as an operating expenditure

As per accounting, upon an asset’s capitalization, it is assumed that the asset still has economic value. It is believed to benefit prospective periods and thus is mentioned over a balance sheet. An expense comprises the core economic costs incurred by any business through daily operations for earning revenue. Every business is permitted to write off all the tax-deductible expenditures on their specific returns for income taxes to minimize the taxable income, hence the tax liability. Most common business expenditures include supplier payments, employees’ wages, factory leases, and equipment depreciation.

Also, check out – Capital Lease vs Operating Lease

Capitalization vs Expensing Example

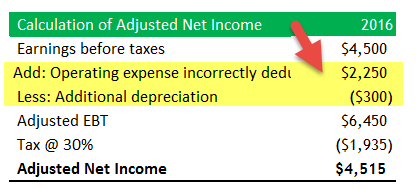

In 2016, the company discovered that $2,250 of its operating expenses should have been capitalized, which would also have increased depreciation expenses by $300.

Calculate Adjusted Total Assets & Equity

For calculating the Adjusted Total assets, we need to make the following changes –

- Since the expense is capitalized, we should add it to the Total Assets ($2,250)

- Incremental depreciation due to this capitalized expense should be deducted from the total asset base ($300)

- Total Adjusted Equity = $15,300 + 2250 – 300 = $17,250

Calculate the Adjusted Income

Here again, there are two adjustments.

- Operating Expense of $2250 should be added back to the Earnings Before Taxes.

- Additional Depreciation expense of $300 should be reduced.

Calculate Ratios – Capitalization vs Expensing

Profit Margin

- Adjusted Profit Margin = Adjusted Net Income / Sales

- Adjusted Profit Margin = $4,515 / $60,000 = 7.5%

- Adjusted Profit Margin increases due to increase in the Net Income

Return on Capital

- Adjusted Return on Capital = (Adjusted Net Income + Interest Expense) / Average Asset

- Adjusted Return on Capital = ($4,515 + $750) / (29,100 + 32,850)/2 = 17%

- In this formula, the numerator increases an increase in the adjusted net income; however, denominator increases due to an increase in the adjusted Asset of 2016.

- We note that the impact of the increase in the numerator is higher than that of the denominator, thereby increasing this ratio from 13% to 17%

Cash Flow from Operations

- Adjusted Cash flow from Operations = Cash flow from operations (before adjustment) + Operating expenses incorrectly deducted.

- Adjusted Cash flow from Operations = $3,300 + 2250 = $5,550

Cash Flow from Investing

- Adjusted Cash flow from Investments = Cash flow from investments (before adjustment) – Capitalized expense

- Adjusted Cash flow from Operations = -$1,500 – 2250 = – $3,750

Total Cash Flows

- If we ignore the tax impact due to changes in the Net Income, the total cash flow remains the same at $150

Long Term Debt / Equity

- Adjusted Long Term Debt to Equity = Long Term Debt / Adjusted Equity = $9,150/17,250 = 53%

Summary of the Adjustment after Capitalization of Expense

We note that most of the ratios have shown a positive impact after capitalization.

Capitalization vs Expensing – Effect on Financial Statements

→ Explore all 65 Financial Statements articles

Capitalizing the costs would usually impact the firm’s financial statements. Some critical areas involved while performing asset capitalization coupled with the way they may alter the firm’s financial statements include,

Balance Sheet Effect – Capitalization vs Expensing

- The firm’s consolidated assets would grow upon capitalization of its costs.

- The impact on shareholders’ equity would be negligible over the longer term; however, in the beginning, stockholder’s equity would be greater.

| Balance Sheet | Expensing | Capitalizing |

|---|---|---|

| Asset and Liability | Lower | Higher |

| Leverage Ratios (debt/equity, debt/asset) | Higher | Lower due to higher base |

| Book Value/Share | Lower | Higher |

Income Statement Effect – Capitalization vs Expensing

- The capitalization of costs would normalize the inconsistency of the firm’s reported income since the cost would get shared between statements.

- From the profitability point of view, the company should enjoy greater profitability in the beginning.

| Income Statement | Expensing | Capitalizing |

|---|---|---|

| Income Variability | Greater variability | Smoothening effect on net income from year to year |

| Matching of revenues | Less matching of revenues and costs | Cost deferred and matched with revenues |

| Profitability (Early years) | Lower as all expenses flow through the IS | Higher as the cost is amortized |

| Profitability (Later years) | Higher as all cost has been expensed | Lower due to amortization of the capitalized cost |

Cash Flow Effect – Capitalization vs Expensing

- Suppose the firm capitalizes its expenditures. The influence would be just on cash flow from operations and cash flow from Investments

| Cash Flow | Expensing | Capitalizing |

|---|---|---|

| Cash Flow from Operations | Lower | Higher |

| Cash Flow from Investing | Higher | Lower |

| Total Cash Flows | Same | Same |

Recommended Articles

For more on Fixed Assets and Depreciation, explore these related articles from our Fixed Assets and Depreciation guide.

Rationale for Expensing or Capitalization

While determining whether any cost must be either expensed or capitalized, firms often employ an easier technique of separating assets into two key segments,

- Assets that deliver prospective gains

- Assets that don’t deliver any prospective gains

Some of the firm’s costs would just deliver a one-time benefit for the firm and, thus, comes under the second segment. These are usually expensed costs since the business is not believed to enjoy prospective gains through them.

Instead, assets that offer prospective gains may frequently stand capitalized, and hence, the expenses would be distributed across financial statements.

An easy instance may be the payment of an insurance policy. The firm may purchase a fixed-dated policy for two years while paying the entire cost in one go. As the insurance would also assist the firm, it may capitalize on the expenditures.

Capitalization of Intangibles

Organizations may even come across intangible assets that are non-monetary properties and don’t have any physical matter; however, they still deliver benefits for the company. Some examples of intangible assets include copyrights, patents, or research and development expenditures.

Patents

- Internally developed patents don’t show up in the Balance Sheet

- SFAS 2 requires all costs incurred with the development of the patents be expensed as they are incurred

- Patents acquired in an arm’s length transaction will show up in the balance sheet at the cost paid to buy it

- Patents are amortized using the legal life or the useful life, whichever is shorter

Goodwill

- Goodwill can only be recorded when a firm buys another firm

- Arm’s length transaction is evidence of the value of Goodwill

- Under SFAS 142, Goodwill is no longer amortized but tested for impairment

- When Goodwill is impaired, it is written down & loss passed through the income statement in the current period

- Managers may have incentives to write down a lot of goodwill, or never write down goodwill at all

Advertisements

- Advertising is expenditures to inform potential customers about the product or services of the firm.

- The benefits of successful advertising may extend for many periods into the future. However, any such benefits are very difficult to measure

- GAAP requires immediate expensing of most advertising costs

- More conservative than capitalization!

Accounting for Research and Development

- Future benefits from R&D expenditures is highly uncertain at the start of a project

- SFAS 2 requires virtually all R&D expenditures to be expensed as incurred

- Principle of conservatism accounting is applied in case of R&D

- However, when one firm buys another firm, the total purchase price must be apportioned among the individual assets acquired

- SFAS 2 requires that a portion of the purchase price be allocated to in-process R&D and be immediately written off

- Managers have a strong incentive to allocate a large portion of the purchase price to purchased in-process R&D

Accounting for Software Development Costs

- More liberal for accounting internal expenditures for software development

- Software development cost is a major cost for many small, growth service companies, and that’s their main asset.

- It prompted FASB to be more liberal while formulating SFAS 86

Capitalization

- The thumb rule for any asset capitalization is that if that asset has a long-term gain or value growth for the firm, there seem to be some drawbacks to this law. For instance, the costs of research & development (R & R & R & R&D) costs are incapable of being capitalized, although such assets strictly offer long-term benefits to the company.

- One key reason most nations deny the capitalization of R&D expenditures is to overcome the doubt about the gains. Evaluating whether the prospective gains from an investment would be problematic, and consequently, it is simpler to expense such costs.

- However, local accountants in different countries may use different ways of analyzing R&D costs.

- In addition, an asset’s capitalization may exaggerate the values of assets, as depicted on the firm’s balance sheet, which can influence the company’s financial statements to some extent.

- Lastly, it is crucial to recollect that inventory costs can’t be capitalized. Even after one may be willing to hold that inventory over the long term and plans to sell it in the forthcoming business cycle, expenses cannot be capitalized.

Expensing

- While beginning a business, there are some critical limitations regarding expenses. In several cases, instant costs may be capitalized despite not necessarily falling under the firm’s capitalization rules for the starting financial year.

- As R&D costs are usually taken as an expense, some legal fees related to the asset’s acquisition can be capitalized, coupled with the patent fees.

- Furthermore, one must remain cautious while expending costs related to upgrades or repairs. If an item’s value improves notably or the item’s lifespan increases, the costs may better be capitalized.

- Lastly, expense lowers the business’s total income earned, and hence, one must be cautious about ensuring that the near-term funds can adjust this modification.

Conclusion – Capitalization vs Expensing

Capitalization against spending is a vital aspect of any business’ financial policymaking. Costs may significantly impact the company’s business finances, while it is crucial to acquire the capability to harness benefits from both capitalization and expense.

The accounting management of expenditures can be a critical difference between any lucrative income statement and the one that illustrates a loss. As a result, it could be challenging to select from these options. However, at large, capitalization against expenses may offer the business significant growth opportunities while keeping the company’s future bright.