Part of our Estate Planning guide

What Is Fair Credit Billing Act (FCBA)?

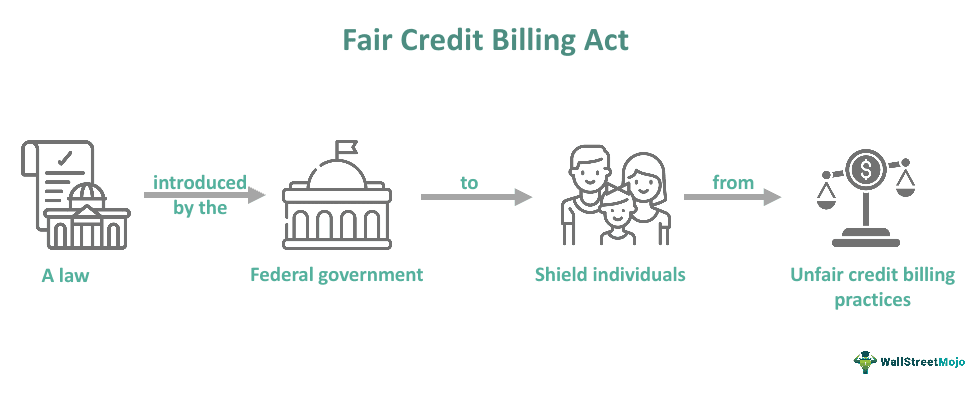

The Fair Credit Billing Act refers to a federal law that came into existence in 1974 to safeguard consumers from the exploitation carried out by creditors via unreasonable billing practices. This law allows a consumer to dispute billing errors or unauthorized charges made on their account.

Per the act, if a consumer disputes a billing error, the creditor must respond to it. However, the consumer need not pay the disputed amount until the investigations are in progress. This law covers unauthorized charges only on revolving or open-end accounts, for example, a HELOC or home equity line of credit and a credit card.

- The Fair Credit Billing Act definition refers to a law enacted by the federal government to shield consumers from being exploited by credit card companies and lenders. This act lets consumers file a complaint regarding billing errors or unauthorized credit card charges.

- The major provisions of the Fair Credit Billing Act are applicable for an open-end account, not closed-end credit.

- While the FCBA aims to protect individuals from exploitations by lenders and card issuers, the FCRA governs the reporting and collection of consumers’ credit details.

- Lenders must complete their investigation within a maximum of 90 days.

Fair Credit Billing Act Explained

The Fair Credit Billing Act definition refers to a government law enacted to protect consumers from credit billing practices that are unfair, thus building consumer confidence. It defines billing errors and enables consumers to dispute fraudulent or incorrect credit charges. The federal government introduced the Fair Credit Billing Act of 1974 to amend the TILA or Truth in Lending Act.

This law does not cover installment loans or debt transactions that give borrowers a certain duration to repay the loan. As noted above, the act’s provisions only apply to an open-end credit account.

According to this act, unfair billing practices may include:

- Incorrect billing amount

- A billing statement that was delivered to a wrong address

- Computation errors

- Charges not authorized by a consumer

- Charges for services and products not received by the consumer

- Failure to accurately reflect the charges with the correct date to charge or credit accounts

- Charges for incorrect goods or services delivered

Rules

Let us discuss the rules for consumers and creditors according to the major provisions of the Fair Credit Billing Act.

#1 – For Consumers

- Only charges exceeding $50 are eligible for dispute.

- If unauthorized users make purchases using a credit card, the credit cardholders’ liabilities do not exceed $50.

- Consumers must file a complaint in writing.

- If a consumer disputes a billing error with a lender, the former may ask the latter to withhold the payment till the latter solves the issue.

- Consumers are able to challenge the results of investigations conducted by lenders within a period of up to 10 days.

- If a credit card is stolen or lost, a consumer can choose to dispute charges via phone instead of filing a complaint in writing.

- A consumer has 60 days from the date of receiving the loan or credit card bill to dispute unfair billing practices with the lender or credit card issuer.

- If authorized card users utilize their credit cards to make unauthorized purchases, this act does not cover the charges. The cardholder will be liable for such charges in this case, per the Fair Credit Billing Act of 1974.

#2 – For Creditors

- If lenders deem the dispute valid, they must rectify the error and initiate a refund of the interest or fee imposed on the consumers.

- A lender must finish an investigation within 90 days. During this period, they must not ask for payment from the consumer. Moreover, the lender must report the disputed amount to the credit bureaus.

- Lenders or credit card issuers may acknowledge a complaint filed by a consumer within 30 days.

- If lenders find out that a dispute is invalid, they must provide documentation and an explanation of their findings to consumers.

Examples

Let us look at a few Fair Credit Billing Act examples to understand the concept better.

Example #1

The CFPB, or Consumer Financial Protection Bureau or filed a lawsuit against Citizens Bank in the U.S. District Court, alleging that the bank did not fairly investigate and address billing errors. Moreover, the bureau alleged that Citizens Bank was only partially able to fund customer accounts when billing errors or unauthorized utilization occurred due to the latter not refunding finance charges or fees sometimes.

In court papers, the CFPB alleged that the practices conducted by Citizens Bank violated multiple federal laws, for example, the Truth in Lending Act, the Credit Card Accountability Responsibility and Disclosure or CARD Act, and the Fair Credit Billing Act.

In May 2023, the bank reached a pact worth $9 million with regulators, settling the charges that the former failed to adhere to federal law by unfairly denying consumers’ fraud claims and credit card disputes.

Example #2

Suppose John, a credit cardholder, noticed that his card issuer, ABC Company, charged an interest of $100 during the financial year 2023. After comprehensively checking his credit card statements, he filed a written complaint to the card issuer, disputing the accumulation of interest charges. After completing a thorough investigation for 40 days, ABC Bank resolved the issue, accepting that no such charges were applicable. John did not have to pay any amount.

Fair Credit Billing Act vs Fair Credit Reporting Act

Many individuals, especially those to finance, are under the impression that FCBA and the Fair Credit Reporting Act or FCRA are the same. However, their meaning and purpose are not the same. One must know their critical differences to comprehend the two concepts fully. So let us look at some of their key distinguishing features.

| Fair Credit Billing Act | Fair Credit Reporting Act |

|---|---|

| FCBA safeguards consumers from unfair credit billing practices conducted by credit card issuers and lenders. | The Fair Credit Reporting Act refers to a federal law governing the accumulation and the reporting of credit-related information concerning consumers. |

| This law came into existence in 1974. | The federal government passed this law in 1970. |

| This law’s enforcement falls to the FTC or Federal Trade Commission. | The FTC and the CFPB enforce this law. |

Frequently Asked Questions (FAQs)

1.Does the fair credit billing act apply to businesses?

The provisions of the FCBA do not apply to businesses. The federal government passed this law to safeguard only the consumers from lenders’ unfair billing practices.

2.What happens if fair credit billing act is violated?

If a lender or a credit card issuer violates consumers’ rights under the FCBA, the latter is entitled to statutory damages of a maximum of $5,000, actual damages. One may also receive punitive damages in case the lender or credit card issuer has a track record of consumers’ rights in the same manner.

3.How do I dispute a charge on the Fair Credit Billing Act?

Under this act, consumers must notify credit card companies by writing a brief letter mentioning any billing error they can spot. The letter must include the consumer’s address, account number, name, and the error amount. Moreover, one must precisely describe the credit billing error in the written complaint.

Recommended Articles

This article has been a guide to what is Fair Credit Billing Act. Here, we explain it with its examples, rules, and a comparison with the Fair Credit Reporting Act. You may also find some useful articles here –

Recommended Articles

Continue with these closely related articles from the same guide.