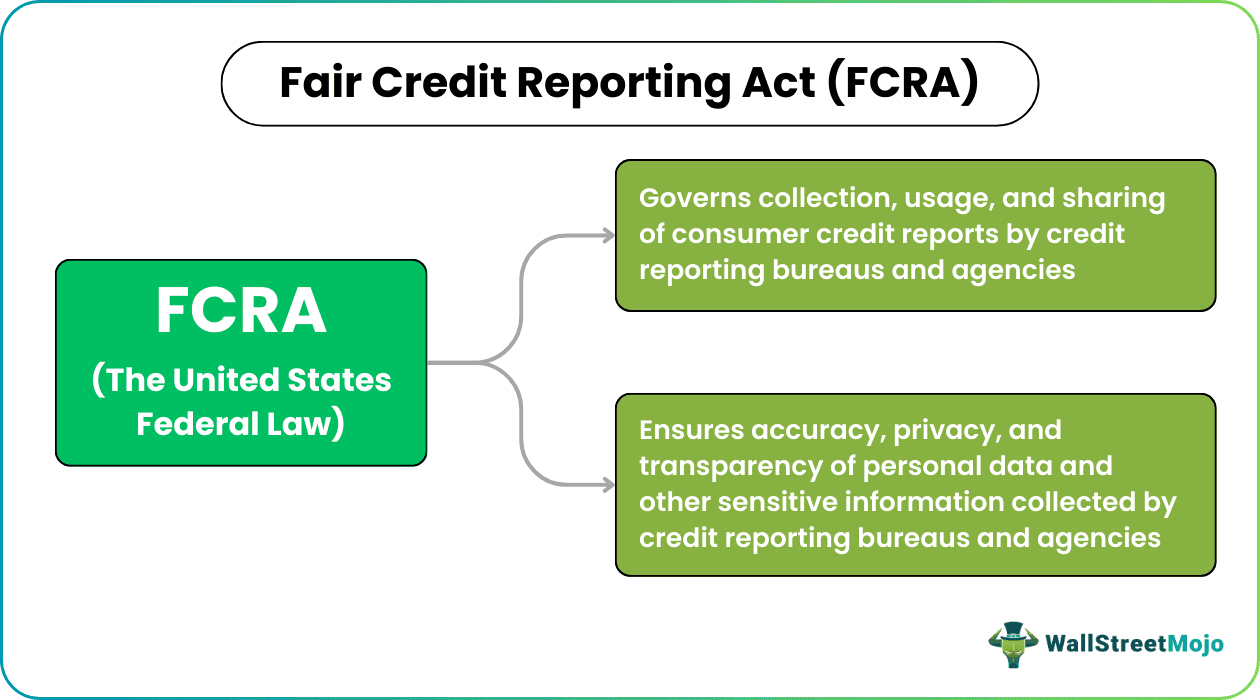

What Is Fair Credit Reporting Act (FCRA)?

The Fair Credit Reporting Act (FCRA) is a federal law in the United States that governs how credit reporting bureaus and agencies can collect, use, and share consumer credit reports. Furthermore, it ensures accuracy, privacy, and transparency of personal data and other sensitive information in the documents compiled by such agencies.

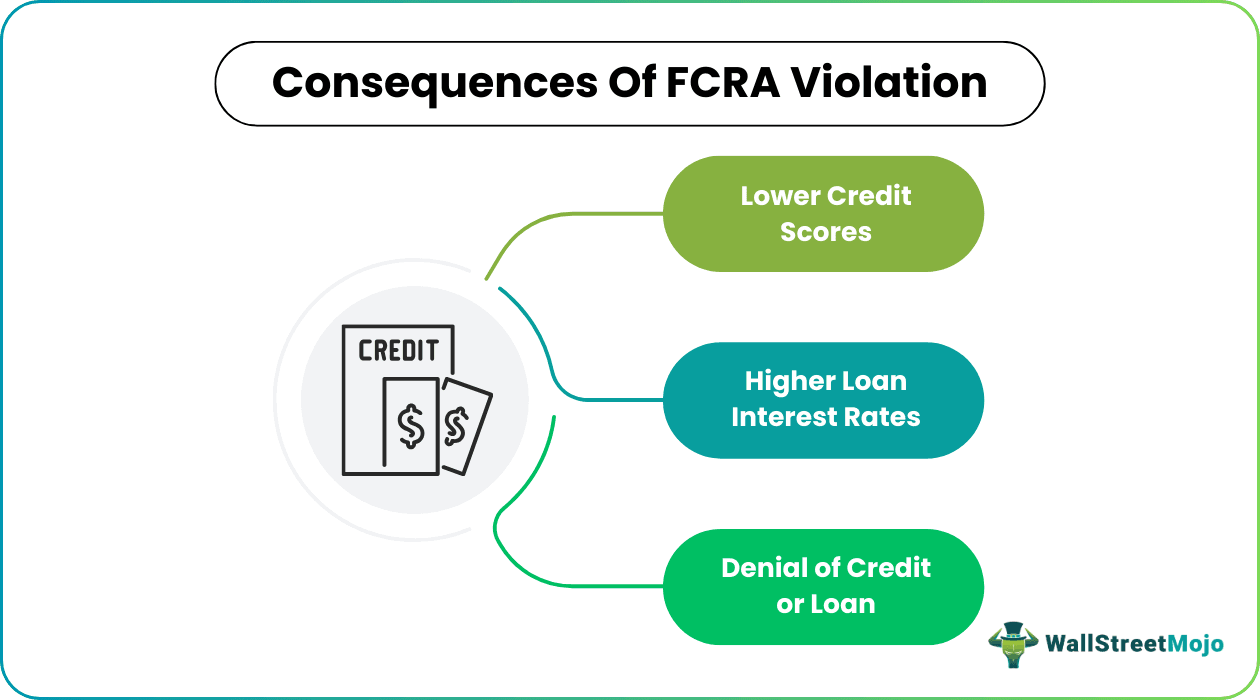

Under FCRA, an individual gets some consumer rights like fair treatment by banks, lenders, and creditors. These parties’ violation of Fair Credit Reporting Act can result in lower credit scores, higher loan interest rates, and denial of credit. The law benefits for consumers include accessing their credit information and disputing incomplete or inaccurate details.

- Fair Credit Reporting Act or FCRA is federal legislation of the U.S. enacted in 1970 to regulate the collection, dissemination, and use of a consumer’s credit, payment history, and financial position.

- When applying for a mortgage or a loan, banks and credit unions often check the consumer’s credit reports.

- FCRA regulations ensure that consumers have some rights, are in optimal authority, and are aware of exercising them.

- Experian, TransUnion, and Equifax are the three most renowned credit reporting bureaus reporting consumer credit information.

How Does FCRA Work?

The Fair Credit Reporting Act definition suggests a federal law passed in 1970 in the U.S. to regulate the collection of credit, payment history, and financial status of a consumer. Credit reporting agencies manage these records of consumers from time to time.

Every person leaves a paper trail and digital footprint of transaction history, credit score, debt, and other crucial details whenever they make a transaction. The credit reports are information that is highly private and confidential.

FCRA is followed by credit reporting agencies responsible for accumulating consumer data and selling it to third parties for reference and background check. They quintessentially gather consumer information like their addresses, employment details, sources of income, payment history, previous loans, current debts, etc.

Credit reporting bureaus keep a strict eye on consumers’ credit reports and records. FCRA puts specific regulations to maintain consumer privacy. For example, how well they are maintained, how many people have access to them, and how long they hold them. It also questions the need for it and the use for others to access these credit reports, including the consumer.

Even though the act may sometimes seem unnecessary or lengthy to follow, it safeguards consumer finances and the credit system.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Purpose Of FCRA

The U.S. Consumer Financial Protection Bureau enforces FCRA regulations. The primary purpose of Fair Credit Reporting Act is to make sure the consumer is well informed about their credit scores, debts, previous loans, and current financial status in the creditors market. It also empowers them to take appropriate actions in case of any discrepancies in the said credit information.

People take loans and mortgages for personal reasons and medical emergencies. In doing so, consumer credit bureaus, such as Equifax, Experian, TransUnion, banks, and credit unions, verify consumer credit history to determine their creditworthiness.

For instance, two brothers took individual loans. One was sincere with financial planning and money management, while the other did not care much about it. In comparison, the smart brother always paid monthly installments without any delay. The other brother missed deadlines, and interest rates grew, penalties were charged. He finally went broke, eventually facing legal issues and bankruptcy.

Sometime later, both brothers applied for another loan from another bank. All banks were happy to lend money to the smart one, but they did not entertain the other and rejected his loan application. The bank had credit reports of both of them, showing how the other took installments for granted.

It is an easy to comprehend example of how credit reports determine one’s worthiness and financial status.

Tip: It is not only essential to have a credit report secured but to have a good credit score as well.

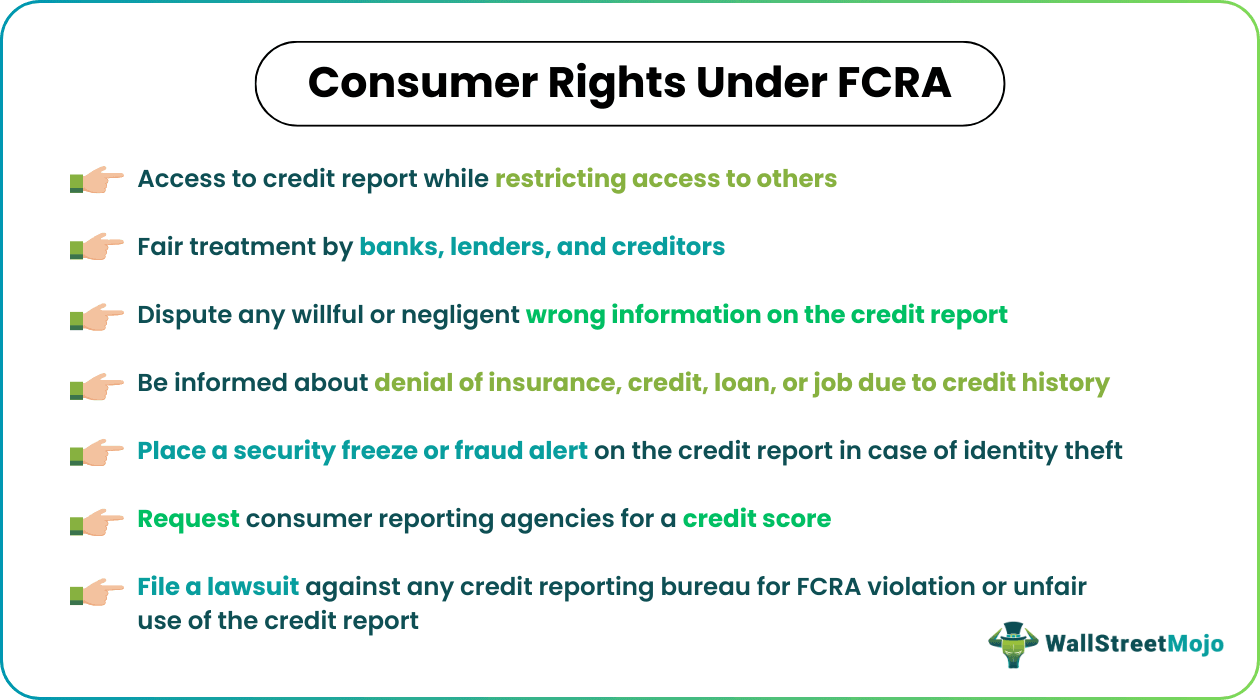

Consumer Rights Under FCRA

FCRA regulations work under complex terms and guidelines, and not everyone can remember each of them. With that said, an individual may exercise consumer rights under FCRA for the following reasons –

- Gain access to credit reports while restricting access to others, excluding landlords, insurers, creditors, and employers (consumer consent required)

- Get all the information a credit reporting agency has on its file, primarily for free

- Ask the consumer reporting agencies for a credit score (may incur a charge for it)

- Request a free copy of the credit report from a credit bureau every 12 months

- Identity theft victims can place a security freeze or fraud alert on the credit report

- Be informed about any adverse actions, such as denial of insurance, credit, loan, or employment due to credit history

- Dispute any willful or negligent wrong information on the credit report to the consumer reporting agency. The data must be corrected or deleted within one and a half months

- File a lawsuit against any credit reporting bureau for the federal Fair Credit Reporting Act violation and inappropriate and unfair use of the credit report and data

Recently, at the onset of the COVID-19 crisis, many credit bureaus offered access to free weekly credit reports until 20th April 2021. They have also announced a free credit report extension till April 2022.

Fair Credit Reporting Act Violations

The consumers may exercise their rights to sue the state, legal institutions, and federal court for damages and non-granted access to their credit reports. The FCRA violation may result in fines and further penalties. The most common breaches of FCRA include –

- The credit bureau duplicating credit records with someone having a similar Social Security Number

- Bureaus messing up personal data and critical information with people of similar first and last names

- The creditor reporting late payments even when these have been made on time

- Creditors sharing credit records with potential identity theft accounts

- The creditor inappropriately filing information like balance due, past debts, and credit scores

- Credit reporting agencies violating consumer privacy by sharing credit records with anybody without any legal permission, warrant, or need

There is a whole list of FCRA violations with legal charges, penalties, and damages paid. However, there are remedies available to willful violations, such as –

- Claiming for basic damages that fluctuate between $100 to $1000 or more

- Claiming for provable damages with no limit to the compensation

- Suing the consumer reporting agency, credit bureau, creditor, or user of consumer information like a bank or credit union in the federal court

- Claiming for punitive damages and legal fees

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

What does the Fair Credit Reporting Act do?

FCRA governs credit reporting agencies’ collection, use, and disclosure of consumer credit information to third parties. Also, it assures that personal data and other sensitive information in documents created by such entities are accurate, private, and transparent.

What are the consumer rights under FCRA?

Individuals may utilize their consumer rights under the FCRA for the following reasons:

#1 – Access credit reports as per requirement

#2 – Request a free copy of the credit report every 12 months

#3 – Place a security freeze on the credit report

#4 – Dispute willful or negligent wrong credit information

#5 – Sue bureau, creditor, or user of consumer information like a bank or credit union in the federal court for not treating them fairly.

What are legal remedies for FCRA violations?

The consumer may sue the state, legal institutions, and federal court for damages ranging from $100 to $1000 and sometimes more, depending upon the harm done.

Recommended Articles

This has been a guide to what is a fair credit reporting act. Here we discuss how does FCRA works along with purposes, consumer rights, and violations. You may also learn more about financing from the following articles –