Part of our Interest Rates guide

Interest Meaning

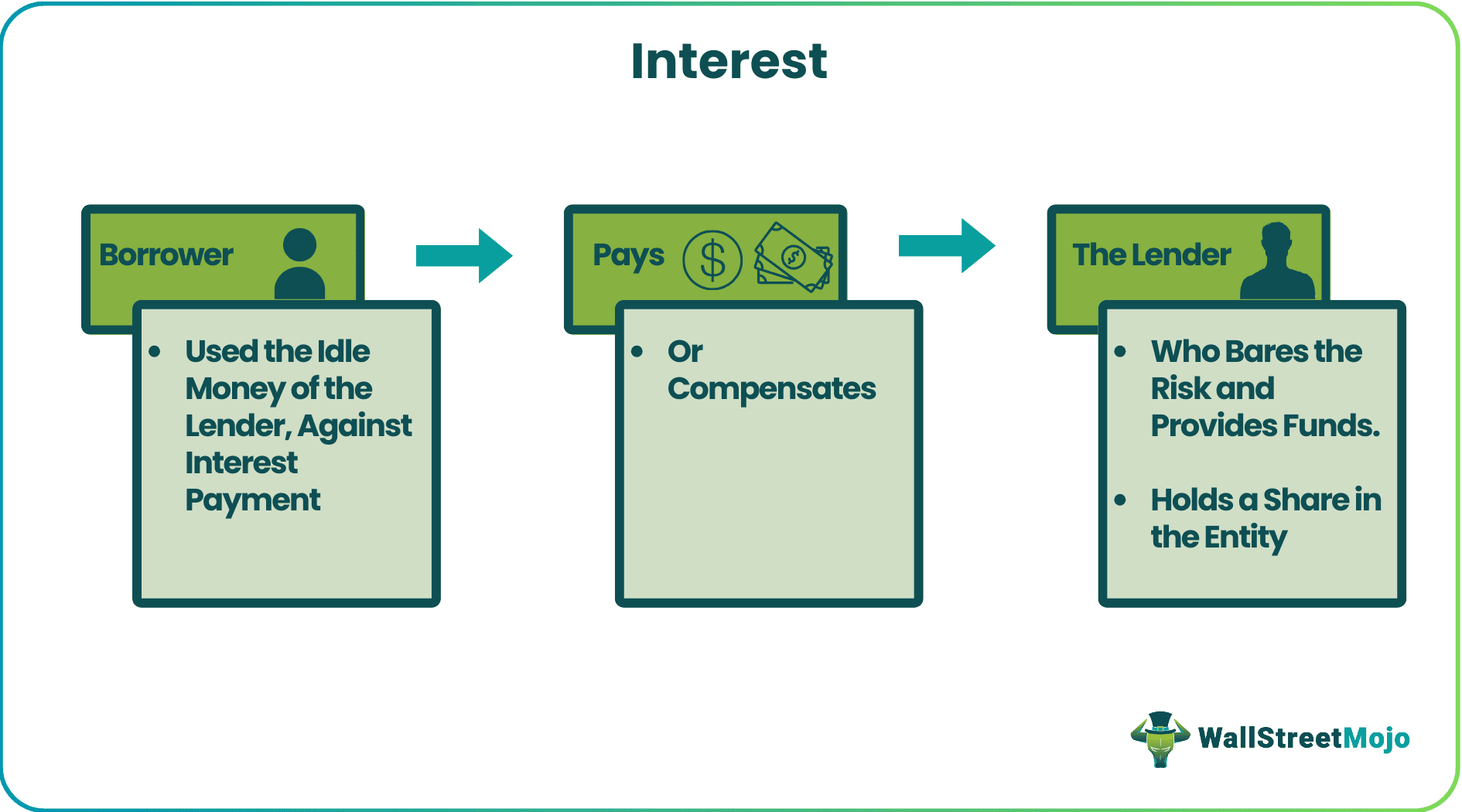

Interest is the monetary revenue that a lender or financial institution earns for lending money. This amount represents a monetary value in dollars and indicates the annual percentage rate (APR) applicable to the borrower. It is a way to compensate the lender for bearing the risk of lending and holding part ownership.

Interest is applicable on car or educational loans, mortgages, credit cards, savings accounts, or overdraft protections. Mostly, it is predetermined between the lender and the borrower to eliminate the risk of late payments, inflationary pressures, and other factors. Thus, an equilibrium price determines the interest liability of the borrower and revenue for the lender.

- Interest refers to the monetary value or annual percentage rate chargeable for lending money.

- A rate or incentive encourages a lender to credit money to a borrower and earn revenue from idle or excess funds in exchange.

- It can also represent the shareholding of an investor or lender in a company that uses the investor’s funds for business operations.

- The central bank or Federal Reserve dictates these rates to control the money supply in the economy and thereby mitigate inflation.

Interest Explained

Interest revenue incentivizes a lender or an investor to lend their money or capital to the borrower. It allows them to make extra income. Thus, a higher rate incentivizes lenders and savings account holders. As a result, the borrower’s borrowing cost is one type of interest chargeable on loans. But on the other hand, the additional income is also earned in the savings account.

Lenders such as financial institutions or entities will lend to earn revenue through returns or dividends. Thus, they will efficiently use their idle money or capital and earn comfortably through interest revenue. Lending provides them with additional cash flow and generates passive income. Extra income compensates a lender for the risks involved as they decide the cost of borrowing depending on the borrower’s credit rating and score.

Thus, if a risky investment usually involves a higher principal amount of borrowing or in case of a poor credit score, then a lender will also seek higher returns or dividends. Similarly, borrowers who wish to attract lower charges should maintain a good credit score by making timely payments.

However, a lender may face risks even after ensuring and studying the borrower’s profile. These might include irregular monthly payments of both interest and loan principal amounts. Additionally, with increasing income in the form of profits, the tax liability of the creditor shall increase as the dividend income shall also be taxed.

A higher rate usually disincentivizes a borrower, debtor, homebuyer, or purchaser. Higher rates increase the liability and repayment value for the borrower. It is important to note that calculating interest involves the principal amount or the amount a borrower borrows as its basis. Consequently, the interest gets added to the principal amount.

Simple And Compound Interest

The basic formula for the interest calculator is multiplying the interest rate with the principal or borrowed amount.

Interest = Interest Rate x Principal Amount

There are two types of interest borrowers might pay on their loan amount. Firstly, simple interest is a fixed rate of interest chargeable on the original amount borrowed by the debtor. It applies only to the original amount the borrower becomes indebted to and thus does not accrue over time. As a result, it leads to slower growth of investment or savings.

Secondly, it is compound interest. Its calculation involves the principal amount and the compounding returns previously paid on the loan amount. It is also known as interest on interest. For example, an individual deposits $100 in a bank at a rate of 8% each year. At the end of the first year, their bank balance will be $108. Similarly, at the end of the second year, the same individual will have $116.64 in their bank account.

Today, most financial institutions, investors, or creditors calculate dividends or returns through the compounding method. However, compound interest charges for a borrower leads to higher debt in case of accumulating monthly payments.

Examples

Let us now see the application of interest in an economy for its consumers, borrowers, businesses, etc.

Example #1

One of the major outcomes of the credit economy is that it feeds on consumerism and generates higher demand. For instance, car loan interest rates offered by commercial banks, car dealers, or other financial institutions in an economy enable an individual or household to decide whether they can afford to make an auto purchase.

Buying a car is an expensive deal, thus making it difficult for individuals or households to pay the entire cost upfront. Thus, a car loan breaks the huge amount into monthly payments, which makes it affordable for the buyer. The car loans vary between a few thousand dollars to $100,000 and with a repayment term of 24 to 84 months. However, deciding on the car loan interest rate depends on the lender and the borrower’s risk profile.

Here, it is important to note that equated monthly installments or EMI as a monthly dividend to the lender shall be higher if the borrower chooses a shorter repayment period. On the contrary, the borrower might opt for a longer repayment cycle, increasing their debt amount.

Example #2

The Federal funds rate or interest rate in the U.S. dictates and controls the cost of money in the economy. The Federal Reserve, the U.S.’s apex bank, regulates other commercial banks in the economy to maintain their stability and solvency. As a result, the Federal or base rates require banks to maintain a certain share of their total deposits as reserves for unforeseen emergencies and economic stability.

Consequently, banks pass these base rates onto the customers within the loan scheme and earn continuous profits by charging borrowers. Additionally, while notifying interest rates, commercial banks consider the risk profile, collaterals, and earnings from a particular customer.

Although, for long-term sustainability, stability of interest rates is necessary along with changing macroeconomic policy objectives. For instance, currently, the federal funds rate is at 3%-3.25%, which it has set to manage the money supply in the economy. However, during the peak of the covid-19 pandemic, a reduction in Federal rates to 0% aimed to mitigate the economic challenges. Thus, it aimed to sustain business activities by making available low-cost credit and keeping the economy away from recession.

Similarly, an increase in this rate shall restrict the flow of credit or make loans expensive by increasing the credit charges.

Interest vs Inflation

Interest rate is a tool utilized by the Federal Reserve in the U.S. or other central banks worldwide to manage the inflationary pressures in an economy. Inflation refers to the general rise in price levels due to increased money supply, supply shortages, or other fiscal stimuli the government provides. Thus, the Federal Reserve aims to achieve stable price levels while maintaining the pace of economic growth. Consequently, inflation rate targeting enables stable changes in the interest rates that sustain economic activity and employment levels.

An increase in the price levels could result from increasing output levels, rising demand, higher incomes, or an increase in the standard of living. Thus, to sustain economic growth, an economy shall have stable and increasing price levels of goods and services.

However, economic crises such as supply shortages or increasing money supply can cause a peak in the prices of goods and services. In such instances, the central bank may intentionally increase interest rates and cool the overheating economy due to inflationary pressures. Similarly, in the case of a deflationary situation, the central banks aim to reduce interest rates to boost economic activity and employment.

However, the central bank follows a particular macroeconomic policy approach or a predictable monetary policy path that allows businesses and governments to adjust their policy accordingly. It allows them to transition smoothly from higher to lower interest rates which mitigates inflationary pressures in the economy overall.

Frequently Asked Questions (FAQs)

1.When interest rates go up?

It may arise due to increasing inflationary pressures on an economy, excess demand, or supply shortage. Thus, to ensure the affordability of goods and services, the central bank increases rates to pull extra money or liquidity from the economy.

2.How interest works on credit cards?

Credit cards usually attract high rates, which are chargeable to the user monthly or annually. So it is because consumers use a credit card to make immediate purchases and pay a small share of interest charges to credit card companies. These returns then accumulate to generate higher overall earnings for credit card issuers annually.

3.Is interest income taxable?

Yes, interest income is taxable, and increasing revenue for a lender or investor automatically pushes them into a higher tax-paying bracket. Many investors and lenders see this adversely. However, an individual might still decide to lend to a borrower to earn extra income from their excess and idle funds.

Recommended Articles

This article has been a guide to Interest and its meaning. We explain how it works, its two types with examples and a comparison with inflation. You can also go through our recommended articles on corporate finance –