Part of our Monetary Policy guide

What is Federal Funds Rate?

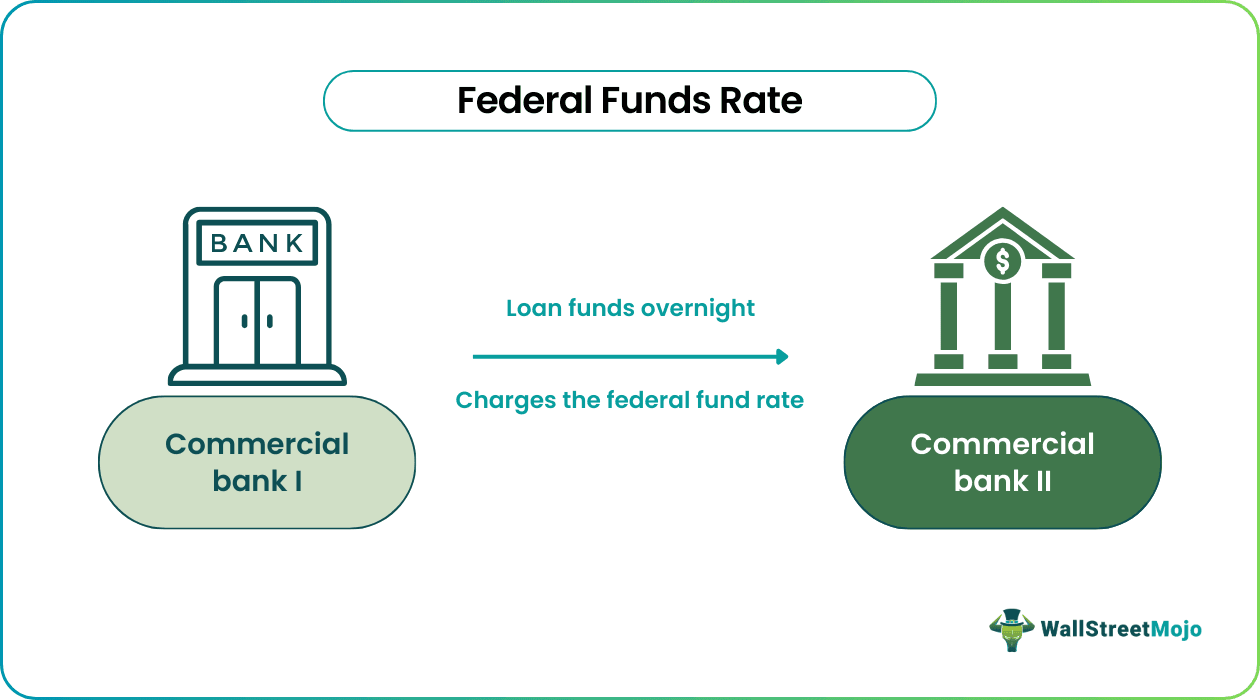

The federal funds rate (FFR) is the interest rate that commercial banks charge each other for overnight loans. The Federal fund rate is set by the Federal Open Market Committee (FOMC). The committee revises FFR eight times a year. It fluctuates in accordance with market conditions.

US commercial banks are mandated to hold a percentage of capital overnight with the Federal Reserve. To meet Fed’s reserve requirements, commercial banks borrow from each other, when they face liquidity issues. For example, in November 2022, the FFR fluctuated between 3.75% – 4%.

- The Federal Funds Rate is the rate US commercial banks charge each other for overnight borrowing and lending.

- Commercial banks facilitate hundreds of transactions on a daily basis; It is common for a bank to run out of liquid cash. Thus, to meet Fed’s overnight reserve requirements commercial banks borrow from each other.

- FFR impacts inflation, and economic growth by triggering changes in short-term interest rates.

Federal Funds Rate Explained

The federal funds rate is the interest rate charged by a commercial bank when it lends an overnight loan to another commercial bank. In the US, this rate is regulated by the Federal Open Markets Committee (FOMC). The FOMC meets eight times annually and sets an FFR based on prevailing market conditions.

Commercial banks facilitate hundreds of transactions on a daily basis; be it loan repayments, deposits, sanctions, or withdrawals. Amidst that, it is mandatory for every commercial bank to deposit a certain percentage with the Federal Reserve. But transactional amount fluctuates and cannot be entirely predicted. It is common for a commercial bank to run out of liquid cash.

Therefore, commercial banks lend from each other to fulfill the Federal Reserve limit. These are overnight loans. Again, Federal Funds Rate is the interest rate charged by US commercial banks when they lend to each other.

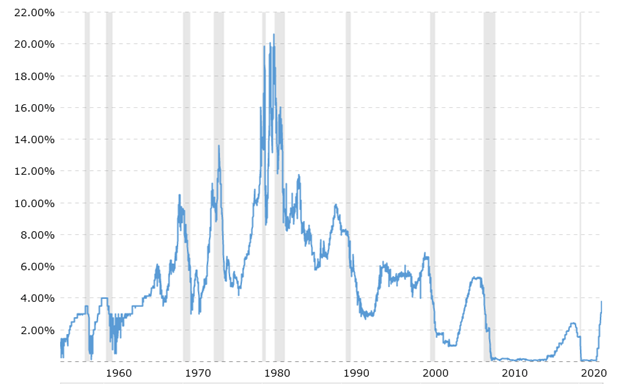

The Fed can increase the rate by changing the reserve amount. This can be done by selling government securities to commercial banks. The FFR chart depicts that Fed fund rates have been increasing over the years. In contrast, to reduce the FFR, the Federal Reserve can buy US treasury bonds back from commercial banks—lowering the reserve.

The FFR significantly affects the US economy, as it sets the tone. The FFR becomes a reference point for several other interest rates. It can trigger other important economic issues like inflation, financial crisis, or market stagnation (long-term).

Usually, FFR is raised to hike the cost of credit in the economy. When interest rates increase, citizens postpone or cancel purchases. Thus, its hike causes stagnation in money circulation. But this is helpful in reducing inflation.

Examples

Let us look at federal funds rate examples to understand the concept better.

Example #1

The Federal Reserve mandates commercial banks to hold a percentage of liquid assets overnight. It is a safety measure. It prevents banks from taking unreasonable risks. Thus, commercial banks cannot lend every single penny. The Fed acts as an emergency fund (reserve) for the entire economy.

When commercial banks lend to each other overnight they submit collaterals. But, during the 2008 financial crisis, the authenticity of the collaterals was in question. Banks were unsure of the financial strengths of their counterparts. One commercial bank was unsure about the other’s ability to repay the overnight loan.

Thus, the frequency of interbank loans fell drastically. The Fed tried to lend directly to commercial banks. But banks were paranoid about borrowing from the Fed. It was a game of appearances; borrowing from the Fed would send a signal, that the particular bank was in trouble. This crisis among US banks further triggered an issue in overseas currency swap markets.

Example #2

Let us look at another example.

Let us assume that Jordan wants to buy a home for his family. The property dealer informs Jordan that the house would cost him $1,080,000. Jordan plans to pay a 20% down payment and the remainder as a loan. Banks offer the remaining $900,000 as an 18-year fixed interest rate loan and charge Jordan with a 3.6% interest.

If Jordan decides to go ahead, he will make a monthly repayment of $5667. By the time he repays completely, he would pay a total of $1,224,178. Of that, the bank will earn 324,178 in the form of interest.

Meanwhile, the Fed increases the effective FFR by 1%; the bank in turn charges an extra 1% from Jordan.

Now, Jordan recalculates the numbers; his monthly payment would increase to $6135. Over the tenure of the loan, he would pay a sum of $1325070. That is, with the hike in rates, Jordan would pay a total of $425070 in interest alone.

Over the period, the small change ends up becoming a substantial amount, and Jordan decides to postpone his purchase.

This hypothetical is a good example of how FFR has a serious impact on banking and the economy.

Chart

The federal funds rate chart is as follows.

(Source)

The FFR has a history of constant fluctuations. The above chart depicts how it has changed substantially over the years.

Federal Funds Rate Vs Discount Rate Vs Prime Rate Vs LIBOR

Now, let us look at federal funds rate vs discount rate vs prime rate vs LIBOR comparisons to distinguish between the terms.

- Federal Funds Rate is the rate at which US commercial banks borrow or lend money, The central bank imposes a discount rate (interest) when it lends to commercial banks (without collateral). The prime rate is the interest charged by commercial banks to their most creditworthy borrowers. The LIBOR, on the other hand, acts as an interest rate for mortgages and corporate loans.

- FFR is regulated by the FOMC. Whereas the discount rate is set by the Federal Reserve. Meanwhile, prime rates vary, as they are set by commercial banks themselves. LIBOR (London Interbank Offer) is governed by the Intercontinental Exchange.

- FFRs affect the entire economy. Discount rates and prime rates affect monthly loan repayments— car loans and mortgage loans.

- FOMC revises the FFR eight times a year. The Federal Reserve, on the other hand, alters the prime rate every six weeks. By June 2023, LIBOR will be replaced by another parameter altogether—The Secured Overnight Financing Rate (SOFR).

Frequently Asked Questions (FAQs)

What is the current federal funds rate?

In November 2022, Federal Funds Rate fluctuated between 3.75% to 4%. FFR is a percentage of capital that commercial banks need to retain with the Federal Reserve. It is a security measure; the Fed prevents US commercial banks from lending to the last dollar. The Fed is like an emergency fund for the entire economy.

Who sets the federal funds rate?

The Federal Open Markets Committee (FOMC) sets the FFR and alters it eight times a year. FFR fluctuates in accordance with market conditions. The FFR graph depicts that Fed fund rates have been increasing over the years.

How can the federal funds rate affect interest rates?

The federal government lowers federal funds rate to stimulate economic growth. When FFR reduces, banks retain more capital and end up lowering interest rates imposed on borrowers. Increased borrowing triggers increased money circulation in the markets. Thus, FFR has a serious impact on inflation, unemployment, and economic growth.

Recommended Articles

This article has been a guide to what is a Federal Funds Rate. Here we explain its examples, chart, and federal funds rate vs discount rate vs prime rate vs LIBOR comparisons. You can learn more about it from the following articles –