Mortgage Meaning

A mortgage loan is an agreement that gives the lender the right to forfeit the mortgaged property or assets in case of failure to repay the borrowed sum and interest. An asset or real estate secures them. These types of loans are considered relatively safe as an asset secures them.

The lender has the right to sell the property to cover expenses due to the borrower’s inability to pay. Therefore, the lender’s associated risk can be low as long as the amount of loan sanctioned is less than the calculated value of the property.

- Mortgage loans are an agreement between a lender and a borrower where the lender has the right to sell the property to recover costs incurred due to the borrower’s failure to pay.

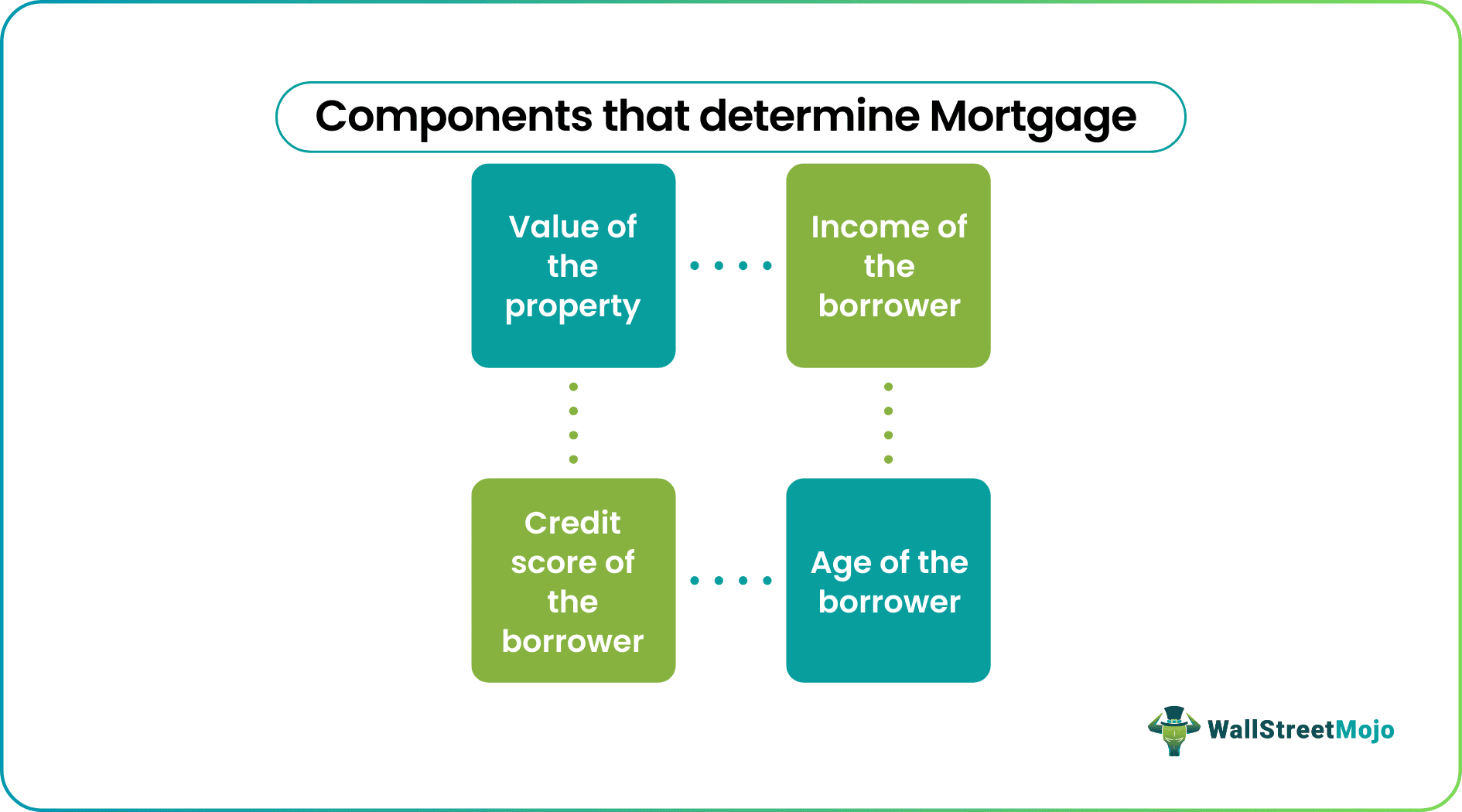

- Economic conditions, the borrower’s credit score, income, age, and the size of the loan amount concerning the property’s worth are all factors that influence mortgage rates.

- Common types of mortgages are fixed-rate mortgages, ARMs, Government-backed loans, etc.

- Closing expenses Prepayment penalties, balloon clauses, interest-only features, and negative amortization are points to consider when getting a mortgage.

Mortgage Explained

Mortgages work similarly to other loans. It provides a borrower with a specific amount of money for a particular period, which they should be then repay with interest. However, mortgages differ from other loans, such as personal loans or student loans. They have secured loans secured by an asset or real estate. As a result, the lender obtains a hold over it and can foreclose if the borrower doesn’t pay.

People use mortgage loans to buy any real estate or borrow money against the property’s value already owned. Mortgage financing is also commonly used for mortgages on foreclosed homes, allowing eligible buyers to purchase bank-owned properties while taking advantage of financing options that fit their budget and long-term goals. The property provided acts as collateral for the loan taken. The lender will assess the value of the collateral provided to let the borrower know how much they are qualified to borrow. A simple online search can reveal the mortgage rates offered by different financial institutions. Similarly, individuals can use online calculators to calculate mortgage payments. Borrowers can also contact a mortgage broker to save time and effort during the application process. They are intermediaries who connect the borrower with the lender. However, as a precaution, the borrowers must go through the varied mortgage loan options available and choose the best one. This will save a lot of money by way of interest.

A type of mortgage is suited especially for senior citizens called a reverse mortgage. Like a standard mortgage, it allows owners to borrow money while securing the loan with their property. When a person takes a reverse mortgage loan, the title to the property remains in the borrower’s name. Unlike the standard mortgages, they need not make monthly mortgage payments with a reverse mortgage loan. The loan is repaid when the borrower is no longer living on that property. Interest and fees are added to the loan balance every month, increasing the total. The owners or successors will have to repay the debt, typically selling the house.

Types of Mortgage

Given below are some of the common mortgage types:-

Fixed-rate mortgages

Fixed-rate mortgages have fixed interest rates. The interest rate will remain the fixed or same as when the borrower took the loan. Hence, institutions will not alter the rates.

A mortgage with an adjustable rate (ARM)

ARMs have lower interest rates, to begin with than fixed-rate mortgages. This initial rate could remain constant for months, years, or years. Interest rates will change when the introductory period ends, and the amount due will most likely increase. A portion of the interest rate paid links with an index, which is a broader measure of interest rates. When the interest rate index rises, the payment also increases. When interest rates decrease, institutions may reduce payments. Some ARMs have a maximum and minimum interest rate cap that borrowers can pay.

Government-Backed Loans

They are of two types- direct issue and insured. Government agencies offer direct issue loans such as the federal housing administration, the U.S. Department of Agriculture (USDA), or the Department of Veterans Affairs. These usually suits low-income households or individuals who cannot afford large down payments.

On the other hand, insured loans are loans that confirm certain lending standards set forth by the FHA (Federal Housing Administration) to qualify. They include programs administered by agencies like USDA and those issued by banks and other lenders, sold to Fannie Mae or Freddie Mac(mortgage companies).

Jumbo Loans

They are similar to conforming loans that Fannie Mae and Freddie Mac buys. However, they exceed the maximum loan amount under conforming loans. Any home loan that exceeds $647,200 in most areas of the United States is a jumbo loan, which may come with additional restrictions or higher interest rates $970,800 in high-cost locations).

Balloon Loans

They are loans that borrowers cannot fully repay through normally required payments. Instead, the borrower has to pay a lump sum or balloon payment at the end of the loan term. It is a larger one-time payment than usual at the end of the loan term.

Mortgage Payments

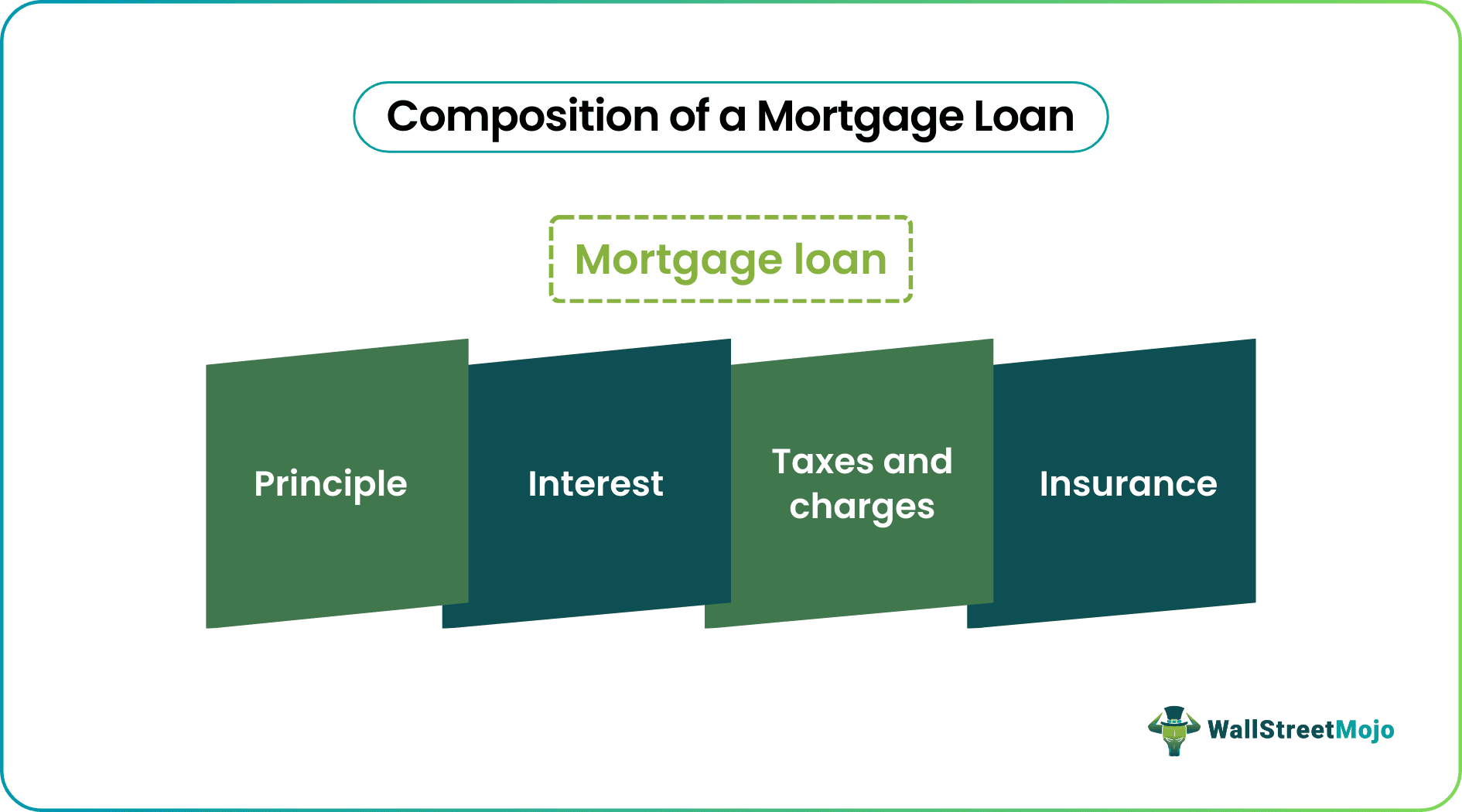

Mortgage payments are mostly monthly and they comprise of:

Principle

It is the total amount of the loan. For example, if the individual takes out a loan for $100,000, that is the principal amount. The down payment is different from the principal amount; it is a percentage of the property’s value after appraisal. The total purchase value of the property, including the principal, will usually be higher.

Interest

It is the monthly payment that the borrower must pay to give profit over the lent amount.

Taxes and insurance

Mortgage payments mostly include property tax and municipal taxes, calculated on the property’s value. However, the lender will include that amount if insurance is present in the charges.

While choosing a mortgage plan, the borrower shall consider the following factors:-

The size of the loan

The amount borrowed shall be within the payable limit of the borrower.

The interest rate, term, and associated points

The length or duration of the loan determines the amount the borrower should pay between certain intervals. Mortgage points are upfront costs that borrowers pay for a lower interest rate on loan. These fees enable saving money on interest over the loan’s lifetime. However, it’s vital to check loan terms because not all mortgages charge points.

The closing costs of the loan

If the borrower decides to close the loan before the lending tenure, the institution may charge an additional fee to cover the loss of interest. The lender shall also consider other payments, such as the lender’s fee on closure.

The annual percentage rate

The annual percentage rate estimates the proportion of the principal the borrower pays each year by factoring in items like monthly payments. It is a broader measure of the cost of borrowing money than the interest rate. It includes all the reflects the interest rates, fees, and related charges that the borrower need to pay to secure the loan. For that reason, your APR is usually higher than interest rates.

The type of interest rate

Whether the interest rate that the borrower has to pay is static or flexible. Each has its perks and the borrower chose it according to their wish.

Other terms and conditions

The borrower must carefully read and decide upon other risky elements of the loan, such as prepayment penalties, balloon clause, an interest-only feature, or negative amortization points. Amortization is paying away a loan over a period to reduce the amount owed with each payment. Conversely, negative amortization means that the debt will grow even after one pays the interests because the amount is insufficient to pay off the interest. If there is a balloon payment on the mortgage, the charges may be lower in the years leading up to the due date, but the borrower may owe a large sum after the loan. Interest-only feature indicates that the borrower only has to pay the interest on the loan for a specific amount of time. The person returns the principal in a lump sum at a predetermined date or in installments.

Example of Mortgage

Dave wants to take a mortgage loan. He takes a loan for $1,00,000 for a tenure of 25 years at an interest rate of 7%. Dave has to pay a monthly amount of $707. This is because the total amount to be payable comes to $2 12,035, spanning 25 years.

If he choses the tenure for 30 years, but with the same interest, the monthly payment is reduced to $665 per month. Similarly, if the amount is increased to 250,000 with the same interest rate of 7% for a tenure of 25 years, the monthly interest to be paid will be $1,767. The values vary when different parameters are adjusted. This demonstrates the significance of choosing the right amount and length of time. The interest chosen shall be within the paying capacity of the borrower.

Note: financial institutions choose the amount to be lent after estimating the property’s market value.

Frequently Asked Questions (FAQs)

What is the difference between a mortgage and a loan?

A loan is an amount of money or fund borrowed from a financial institution. These institutions could secure it without collateral, whereas a mortgage is an immovable property or asset used to secure a loan.

What percentage of income should the mortgage be?

Mortgage rates depend on many factors, including the individual’s credit score, income, age, the value of the collateral, etc. The financial institutions choose what amount to be given for the property. Therefore, the individual should calculate mortgage payments beforehand and decide what is affordable and not overbearing.

Are mortgage payments tax deductible?

Borrowers can deduct mortgage interest payments on the first $750,000 ($375,000 if married filing separately) of debt. However, if mortgage interest is deducted from debt incurred before December 16, 2017, the limits are higher ($1 million ;$500,000 if married filing separately).

How are mortgage rates determined?

Mortgage rates are arrived at by considering a combination of market and personal factors, including economic conditions, the borrower’s credit score, income, age, and the size of the loan amount concerning the value of the property.

Recommended Articles

This has been a guide to Mortgage and its meaning. Here we discuss the types, components of payments and example of mortgage loan.. You can learn more from the following articles –