Part of our Interest Rates guide

What is Prime Rate?

Prime Rate (also known as Prime Lending Rate, i.e., PLR) is an interest rate offered by banks for their most creditworthy customers. These customers are generally huge corporates with a spotless credit history. These rates are not centralized and can vary from bank to bank.It forms the basis for interest rates on business loans, personal loans, vehicle loans, home loans, mortgages, etc.

There is no standard authority for publishing prime rate interests. Each bank sets its own rates based on the federal fund’s rates. Generally, banks use fed rates plus three to determine their rates for lending. These rates are annually calculated to form the Annual Percentage Rate (APR). Other customers are charged interest based on their credit scores.

Key Takeaways

- The prime rate is determined by individual commercial banks, typically based on the federal funds rate or the equivalent benchmark interest rate set by the country’s central bank.

- It is levied between commercial banks (levied from the lending bank to the borrowing bank). It is the foundation for interest rates on loans for businesses, individuals, cars, homes, mortgages, etc.

- The Federal Open Market Committee, or FOMC, can determine the base or target rates for Federal Funds. Banks enter the picture to determine which prime rate will be used.

- It aids in locating the bank’s riskier assets. Banks might use this information to estimate the rate they can provide depositors to decide on their profitability.

Prime Rate Explained

The prime rate is the interest rate charged by banks for their top customers with significantly high creditworthiness. These rates are not centralized; as in, they are furnished by each bank separately based on the federal fund rates.

Generally, the fed rates plus three is a normal practice banks follow for their top customers’ bank prime rate, who are generally large corporations. For all other customers, their credit score determines the interest rates that might be charged to them.

Suppose you take a home loan from a commercial bank at an interest rate of 7% per annum with a tenure of 15 years. Have you ever thought about what this 7% comprises? Let’s dig into the same –

Interest Rate to Charged = Prime Rate + Risk Premium + Inflation Premium

Let’s assume the following figures:

- Prime Rate = 3%

- Risk Premium = 2% (Risk Premium is the extra interest charged upon various factors such as the creditworthiness of the customer, income factors, growth factors, the value of a home, etc.)

- Inflation Premium = 2% (Inflation Premium is charged on the basis inflation situations around the country)

That makes the interest rate charged by the bank to you. So, we were talking about the basic charge, i.e., the prime rate. If you see, most creditworthy customers are not charged with the risk premium. In that case, the interest rate goes with Prime Rate + little margin.

It is decided as follows –

Prime Rate = Feds Target Rate + 3% Usually

The federal funds target rate is the benchmark rate every six weeks. If the Feds Target rate changes, the prime rate also changes. In response to the economic disruptions caused by the COVID-19 pandemic, the Federal Reserve significantly reduced the federal funds target rate to a range of 0% to 0.25% in March 2020. This action led to a corresponding decrease in the U.S. prime rate to 3.25% as of March 15, 2020.

Since then, the Federal Reserve has gradually increased interest rates to address rising inflation and stabilize the economy. As of April 21, 2025, the federal funds target rate stands at 4.25% to 4.50%, and the U.S. prime rate is 7.50%.

The Federal Reserve continues to monitor economic indicators closely to determine future adjustments to interest rates.

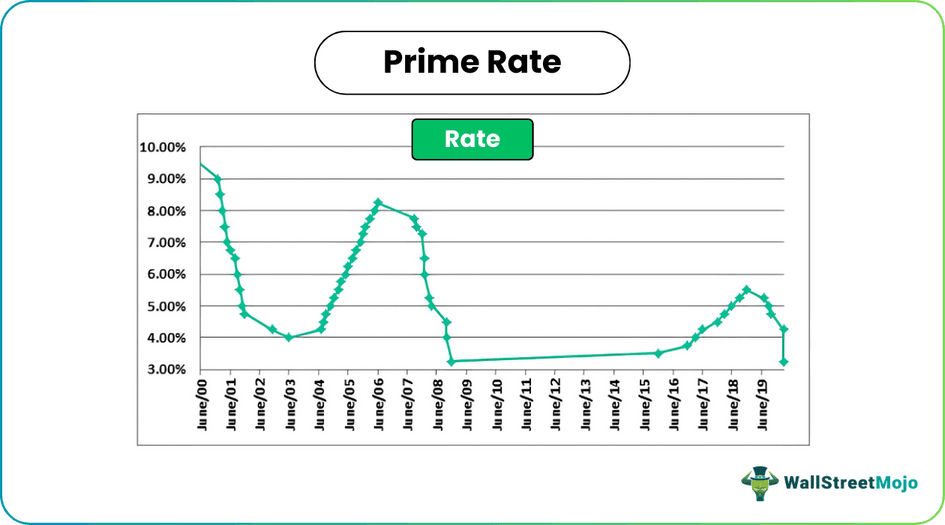

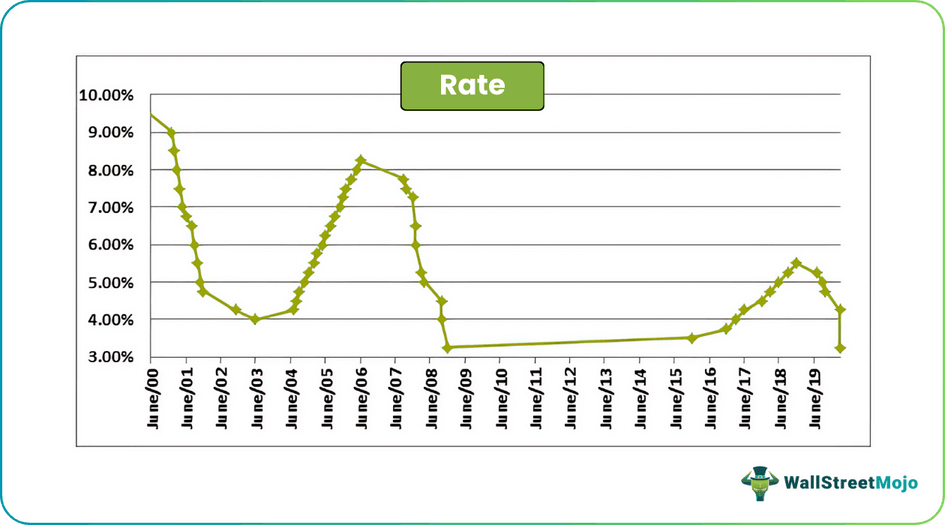

History

Let us understand the history of prime rate interest to understand how far it has evolved and the ebbs and flows of the concept by dialing back into time.

Since the turn of the century in the year 2000, the prime rate was 8.75% and almost two and a half decades later in 2023, the rates rowed back to 8.25%. However, in the 23 years in between the rates went up aggressively and plummeted many times based on the fed rates.

Economic conditions in different countries lead to different centralized interest rates which in turn boil down to the end customer- common men and women who seek loans for their needs and wants.

The chart below shows an overview of the rates since 2000:

Determining the Prime Rate

The bank prime rate can be fixed by each bank based on the fed rates and their internal reserves. However, there are a few other points that need to be taken into consideration which we shall learn from the explanation below.

- Every bank has the right to decide its rate. However, each bank must keep the lending rate near the prime rate.

- As said earlier, firstly, the committee decides the base rate, i.e., the Federal Funds Target Rate (which currently is 0 to 0.25%). After determining the same, each bank uses it as a base for deciding the prime lending rate.

- For deciding this rate, banks consider the minimum default risk amongst the customers. Bank would charge lower for lower defaults high & vice-versa.

- So, you can now guess that there is no single rate as such & it is usually the average rate charged by the largest banks.

Who Sets It?

Despite the fact that there is no centralized publishing authority, the bank prime rate vastly depends on the base rate set by the feds. Therefore, indirectly, the federal reserve can influence the changes in rates. Let us understand how they do so through the explanation below.

- Firstly, the FOMC (i.e., Federal Open Market Committee) is the authority to decide the base rate, i.e., the Federal fund’s target rate. It meets every six weeks & in such a meeting; it is decided whether to change the base rate. If the base rate changes, the prime rate changes accordingly.

- The banks then come into play to decide the prime rate to prevail.

Uses

It is natural for anyone to wonder how two different interest rates for different customers help the banks. In fact, the large corporations that hardly default would be great ways to earn more in interest income.

It makes sense for the banks to lend at a marginally lower interest rate to these customers as the amount is generally large and there are other factors involved as well. Let us understand them and the uses of prime rate interest through the points below.

- Since the base rate is the same, it helps compare the interest rates offered by two banking institutions. Thus, it helps in deciding a business person whether to borrow from Bank A or Bank B.

- It helps identify the riskier assets of the bank, i.e., those loans where the bank has charged a higher interest rate compared to others.

- It helps banks determine the rate they can offer to the deposit holders so that they can decide on their profitability.

- It helps to keep inflation under the control of the government.

- It forms the basis for the other loan products offered by the bank. Thus, this assures the minimum revenue for banks.

Why it’s Important?

Now that we have understood its uses, who sets it, and how it is determined, is vital for us to understand why it is important to fully understand the concept and its related factors. Let us discuss the importance of prime rate interest through the points below.

- The interest rate charged by the bank is primarily based on the prime rate & then a little margin over it. So, you can see that all products of any bank, let it be Thus, when the Federal Open Market Committee increases or decreases the base rate, the consequential prime rate will change & thereby, it changes the variable interest rates offered on the products. That’s how this rate is important for any financial institution.

- This is the ultimate rate that changes the minimum amount due on your credit card usage, the Equated-Monthly-Installments, the principal component from your EMIs, the interest rate on mortgages, and even on the student loans & whatnot.

Frequently Asked Questions (FAQs)

What occurs when the prime rate rises?

When the prime rate rises, the economy frequently contracts, and inflation fall. A lower prime rate often increases market activity as more people take advantage of the cheap rates to borrow and spend money.

What is the highest prime rate there has been?

On December 19, 1980, the prime rate reached a record-breaking 21.5%, making it the highest rate in history.

How is the prime rate decided upon?

While the Federal Reserve plays no direct involvement in determining the prime rate, many banks base their prime rates in part on the federal funds rate’s target level.

Recommended Articles

This has been a guide to what is Prime Rate. Here we explain its history, how Prime Rate is determined, along with examples, uses, and why it’s important. You can learn more about from the following articles –