Part of our Shareholder Equity guide

What Is The General Reserve?

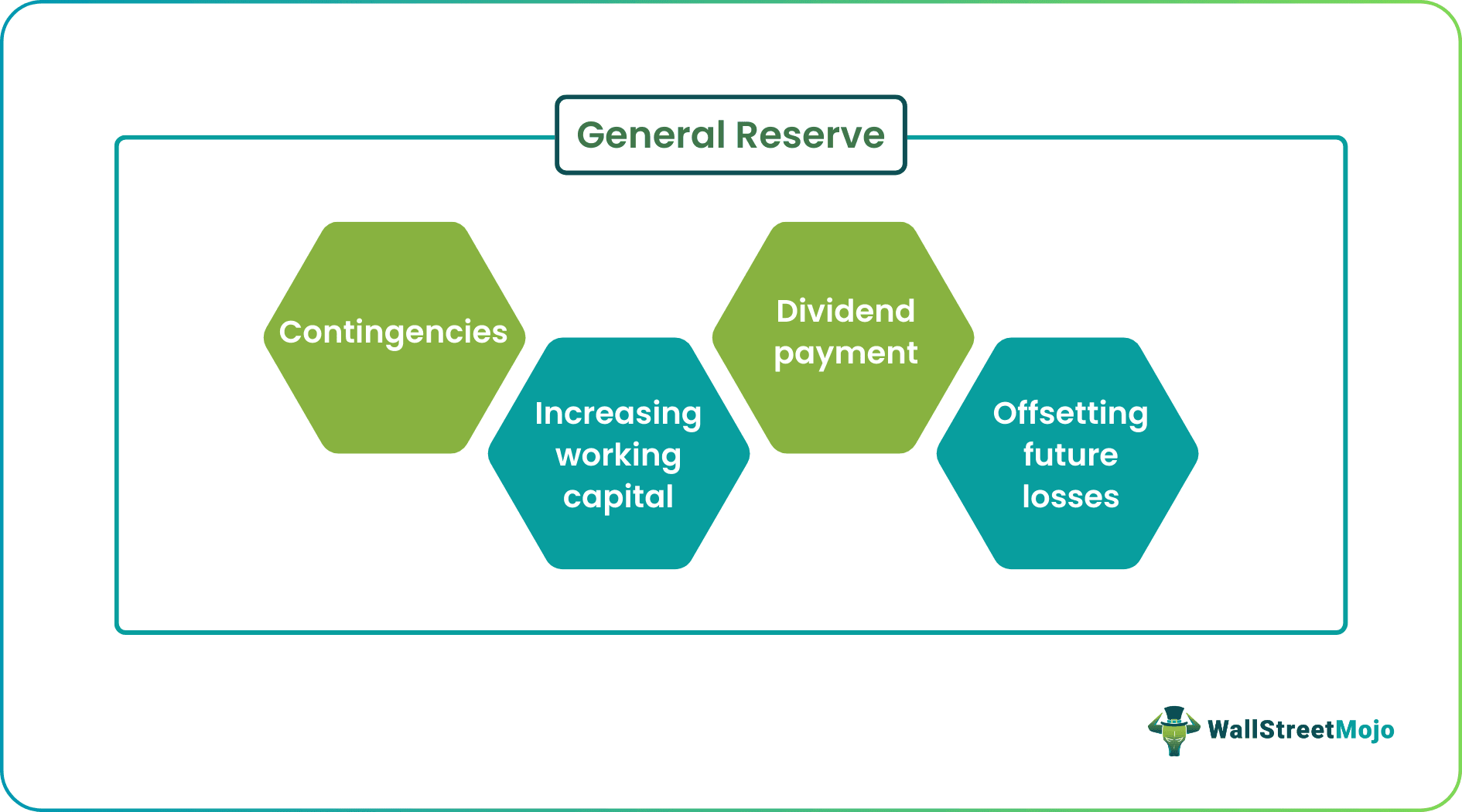

General Reserve is part of the profit and loss appropriation account. General Reserve is the amount kept aside from the company’s profit during its normal operation to meet future needs. I.e., contingencies, strengthening the company’s financial position, increasing working capital, paying dividends to the shareholders, offsetting specific future losses, etc. appropriation account.

Generally, a general reserve fund is used to meet future uncertainties like future losses of the business, future litigations, etc., and there is no prescribed percentage for the creation of reserves. It is the company’s discretion how much reserve it wants to accumulate. In case of losses, reserves are not created by the company.

General Reserve Explained

General reserve is a specific percentage of money set aside by a company from their profits. The funds in this reserve are used to fulfil future contingencies, paying dividends to their shareholders, and offset specific future losses.

It is the reserve created by the company without any specific purpose using the profit generated during the period and is kept aside by the company for meeting future liabilities.

The company can utilize the available reserves for various purposes, such as settling any unknown future contingencies, strengthening the company’s financial position, increasing working capital, paying dividends to the shareholders, offsetting some specific future losses, etc.

As the amount available in the general reserve account is accumulated to meet the company’s future obligations, it helps improve the financial position by helping the company meet the uncertain financial contingencies.

There is no prescribed percentage mentioned anywhere for the creation of the available reserves by the company, and it is at the company’s discretion how much reserve it wants to accumulate.

The company creates them only in case it earns a profit during the period, and if there arise losses in the business, then the reserves are not created by the company.They are shown in the head’s reserves and surplus on the liabilities side of the balance sheet.

It is the free reserve that the company can utilize for any purpose it requires after fulfilling certain types of conditions. They provide resources and the funds required for the expansion of business activities and meeting the company’s future obligations, thereby improving the financial position. No prescribed percentage is mentioned anywhere for the company’s creation of the general reserves. It is at the company’s discretion on how much reserve it wants to accumulate.

How To Calculate?

Any organization irrespective of its size and stature, looks to settle its immediate financial obligations such as salary to employees, payments to suppliers and vendors, rent, and other such obligations.

Therefore, accounting for these expenses, the management calculates their total receivables and comes to a conclusion on the percentage they want to set aside to meet contingencies in the future.

After these expenses are accounted for, the company shifts a certain percentage of its revenue by passing a general reserve entry.

For instance, if company XYZ had revenue of $100,000 in a particular year. The management decided to keep 15% of their revenue as a reserve. Therefore, their reserve would hold $15,000.

Examples

Let us understand the concept of maintain a general reserve fund with the help of a couple of examples. These examples shall give us a practical overview of the concept and its intricacies.

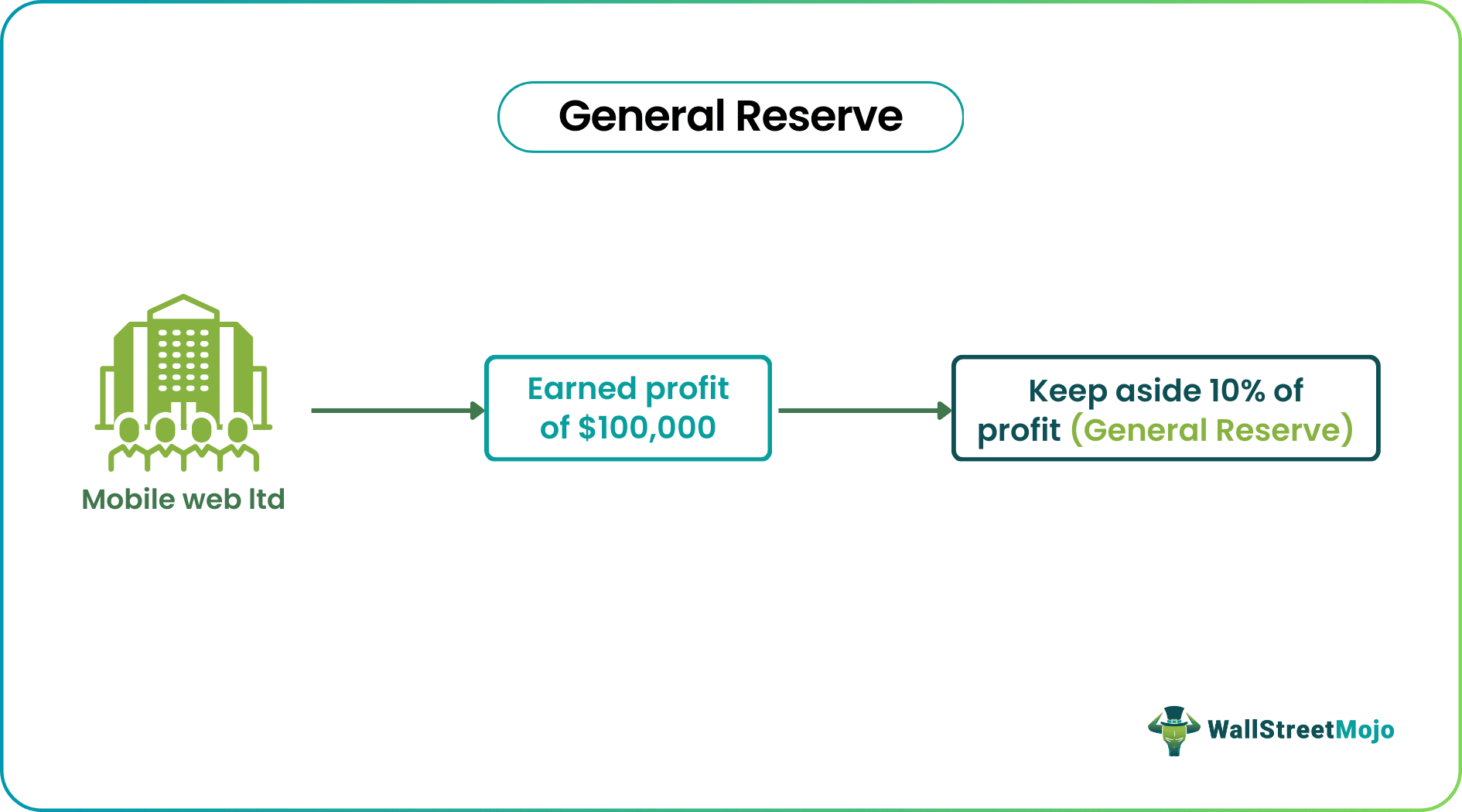

Example #1

Company Mobile Web Ltd. is doing the business of mobiles. During the financial year 2018 – 19, it earned a profit of $100,000 from its normal course of operation. The management of the company decides to keep aside 10 % of the profits earned during the financial year for meeting future liabilities and not for any specific purpose. Which reserve is the company creating, and where will it be shown in the Balance sheet of the company?

In the above case, the company kept aside 10 % of the profits, i.e., $ 10,000 ($100,000 * 10%) earned from its normal operation during the financial year without any specific purpose. This general reserve will be considered as part of the profit and loss appropriation account. It will be shown under the head’s reserves and surplus on the liabilities side of the company’s balance sheet. So this is an example the company has made.

Example #2

In September 2022, the Indian mining giant proposed in the meeting with the board that they seek to transfer ₹12,587 crores from their general reserve to retained earnings.

The transfer is up for vote from shareholders and the members of the board. Funds from the reserve shall be used to pay dividends to its shareholders. Out of the ₹12,587 crores, 70% will be transferred to its parent company- Vedanta Resources to pay off its debt obligations.

An extraordinary shareholders’ meeting was held on October 11 to pass this motion with the consent of the stakeholders of the company.

Advantages

Let us understand the advantages of maintaining a general reserve account through the explanation below.

- It is the primary source of financing through internal means. So they provide resources and the funds required for the expansion of business activities and meeting the company’s future obligations, thereby improving the financial position.

- One of the significant benefits of creating a general reserve is overcoming the losses that may occur shortly. So at the time of losses, a company can pay off its present liabilities with the help of available reserves.

- Reserves help maintain the required working capital in the company as it contributes towards the working capital in case there is any shortage of funds in the working capital.

- With the help of available reserves, the company creates an account. It helps to replace useless and obsolete assets with new assets without the requirement of borrowing funds from the outside.

- The amount available in the general reserve account can be used to distribute dividends. If the company wants to maintain a uniform rate of dividends, then if there is a lack of funds for the distribution of dividends, the amount can be withdrawn from the general reserves.

Disadvantages

Despite the advantages mentioned above, there are a few factors from the other end of the spectrum that prove to be a disadvantage for the company and its shareholders. Let us understand the disadvantages of passing a general reserve entry through the points below.

- If the company incurs losses during a financial year and has an existing general reserve, it will offset its losses using the available general reserve. It will not show the exact picture to the user of the financial statements. With the help of the general reserve, the company’s financial position will show a better picture than it is for the period under consideration

- As there is no specific purpose for which the general reserve is created, there exists the chance that the management of the company will not adequately utilize the reserve. There could be a misappropriation of the funds.

- The company creates the general reserve available from the profits earned during the period. It results in a reduction in the rate of the dividend.

General Reserve Vs Capital Reserve

Although both a general reserve account and a capital reserve are an amount set aside from the proceeds from the business, their uses and implications are quite different. Let us understand the differences through the comparison below.

General Reserve

- It is derived out of the revenue profits from a specific period and transferred into a specific account for no specific reasons.

- They can be used to meet future contingencies such as offsetting specific losses or paying dividends.

- It is reflected in the ‘Reserve and Surplus’ section of the balance sheet. However, it is appropriated through the profit and loss appropriation account.

- Since the use of these funds is not specific, it is unlimited how companies decide to use them.

Capital Reserve

- It is derived out of the capital profit of a company and cannot be used for general purposes such as declaring dividends.

- It is shown under ‘Reserves and Surplus’ in the balance sheet separately.

- The funds in this reserve can be used to write off capital losses or provide shares and debentures at a discounted price, or issue bonus shares.

- The use of the funds from this account is specific. Therefore, the scope is very limited.

Recommended Articles

This article has been a guide to what is General Reserve. Here we explain how to calculate it, its examples, and advantages, and compared it with capital reserve. You can learn more about accounting from the following articles –