What Is LIFO Reserve?

LIFO reserve is the difference between what the company’s ending inventory would have been under FIFO accounting and its corresponding value under LIFO accounting. Companies that use the LIFO Inventory method are required to disclose this reserve which can be used to adjust the LIFO cost of goods sold and closing Inventory to their FIFO equivalent values to make it comparable.

Companies can choose to cost their Inventory based on various cost flow methods (namely FIFO inventory, LIFO inventory, Weighted Average Cost, and Specific Identification Method). This choice of inventory method affects the Income Statement, Balance Sheet. It directly impacts the various financial ratios that various stakeholders use in analyzing the performance of various companies. Additionally, it impacts a company’s Tax liability and cash flow.

LIFO Reserve Explained

LIFO reserve accounting is a concept in the books of accounts that explains the difference between the cost of the closing inventory calculated using LIFO method and the cost of closing inventory derived form FIFO(First In First Out) method. The above are two different but widely used procedures for evaluation of closing balance of inventory. But due to their difference in calculation, the resultant figures will vary.

Under the LIFO, it is assumed that the inventory that arrives most recently is the one that is used or consumed up first. Therefore, in LIFO reserve equation, the value of cost of goods sold will be the cost of the inventory that is used first. This helps the business by bringing down the taxable income in the income statement because if the cost of current raw materials go up, then the value of the remaining old stock is lower, which is displayed in the balance sheet and a higher COGS lowers the income.

Hence, when comparing two companies – Company A, which follows the LIFO method of Inventory, and Company B, which follows the FIFO method of Inventory, the financial performance and ratios of the two companies become incomparable.

Therefore, we convert LIFO Inventory into FIFO inventory by using this reserve to make them comparable.

US GAAP requires that all companies that use LIFO to also report a LIFO reserve.

US GAAP requires that all companies that use LIFO to also report a LIFO reserve. This reserve is mainly used for taxation purpose in US because it allows companies to defer the tax payments as mentioned above. However, tis concept is limited to the US mainly because the LIFO metgod is allowed only as per the Generally Accepted Accounting Principles (GAAP). The LIFO accounting is not allowed by the International Financial Reporting Standard (IFRS), thereby making the rules of accounting different based on the method followed by the particular country.

Formula

The following are the different steps of the calculation of LIFO reserve accounting used in finding out the reserve value for the business.

- LIFO Reserve formula = FIFO Inventory – LIFO Inventory

When the company provides this reserve, we can easily calculate FIFO inventory using the below formula.

- FIFO Inventory = LIFO Inventory + LIFO Reserves

Similarly, Cost of goods sold can be adjusted as follows:

- COGS (using FIFO) = COGS (using LIFO) – changes in LIFO Reserve during the Year

Thus by making such necessary adjustments, the financials can be made comparable, and the impact of using the LIFO method of Inventory reporting, if any, can be neutralized, and also any profit attributed due to LIFO Liquidation (discussed above) can also be ascertained to make a better Financial Analysis of the Company.

Journal Entry

→ Explore all 30 Journal Entries articles

As we are already aware, the LIFO reserve calculation will represent the difference between the value of closing inventory calculated using both LIFO and FIFO. This has already been explained in the formula above. However, any change in the reserve value will be due to changes occurring in the closing inventory calculated using the two methods.

Since any variation in the inventory value is a part of the COGS, the double entry in the accounting books will be doen as follows:

Cost Of Goods Sold A/c Debit

To LIFO Reserve A/c

As the above entry shows, the value of COG rises due to higher value of the recent materials that will move out of the inventory stock first.

Disclosure

Under the LIFO reserve equation, LIFO reserve is the difference between the cost of Inventory computed using the FIFO Method and the LIFO Method.

- Using the LIFO method of Inventory, Costing companies can increase their cost of goods sold, which results in lower Net income and, consequently, lower taxes in an inflationary period.

- It is also known as Revaluation to LIFO, Excess of FIFO over LIFO cost, and LIFO Allowance and helps different stakeholders to make a better comparison of the Net Profits reported by the Companies and various financial metrics.

LIFO Liquidation

A declining reserve is an important indicator that can be used for analyzing the profitability of a company and its sustainability. This method is quite popular in the United States and is allowed under US GAAP (LIFO Method is prohibited under IFRS). Companies opting for the LIFO method of Inventory are required to disclose Last in First Out Reserve in the footnotes of their financial statements.

- The change in the Reserve account balance during the Year is referred to as the LIFO Effect.

- Usually, a declining reserve indicates LIFO Liquidation, which happens in cases where a firm is selling more Inventory than it purchases during inflationary periods; it reduces the cost of goods sold, thereby increasing the profits. However, such profits are not sustainable. Such profits reported by the company need to be adjusted to avoid the impact of such LIFO Liquidation to make them comparable with companies opting for the FIFO method.

- Hence, changes in LIFO Reserve should be closely analyzed. It allows a meaningful comparison of profits and various financial ratios reported by the company using the LIFO Method and company using the FIFO Method.

- Also, it acts as a good measure to understand the impact of the company’s reported Gross Margin on inflationary pressure.

Example

Let us study the concept of LIFO reserve calculation using LIFO reserve calculation with the help of some suitable examples.

Example#1

Kappa Corp. uses LIFO inventory accounting. The footnotes to 2007 financial statements contain the following.

| Particulars | 2006 | 2007 |

|---|---|---|

| COGS | 50000 | 60000 |

| LIFO Inventory | 400000 | 460000 |

| LIFO Reserves | 42000 | 45000 |

Calculate Kappa’s 2007 COGS under FIFO

- COGS (FIFO) = COGS (LIFO) – changes in LIFO Reserve

- COGS (FIFO) = 60,000 – (45,000-42,000) = 60,000 – 3,000 = $57,000

Example #2

Let’s understand the concept of the LIFO Liquidation with the help of an example:

XYZ International Limited uses the FIFO method for internal reporting and the LIFO method for external reporting. At the yearend Inventory as per FIFO stands at $100000 under the FIFO method and $70000 under the FIFO method. At the beginning of the Year, the company’s LIFO Reserve showed a credit balance of $25000.

- LIFO Reserve Formula = FIFO Inventory-LIFO Inventory = $100000-$70000 = $30000

- Thus LIFO liquidation effect for the Year will be $5000 ($30000-$25000).

Thus, the above examples clearly explain the concept. We see through a hypothetical example how the formula can be used to calculate the reserve and liquidation example also explains the procedure to calculate the same.

Accounting Adjustments

Now let us look at some of the important LIFO reserve adjustment that are to be made in the financial statements, namely the income statement and the balance sheet so that they reflect the true and correct value of inventory levels. This is very impoortnat form the management point of view as well as investor or other stakeholder point of view.

The steps involved in adjusting the financial statements of a company opting for the LIFO method to reflect the FIFO inventory cost method are as follows:

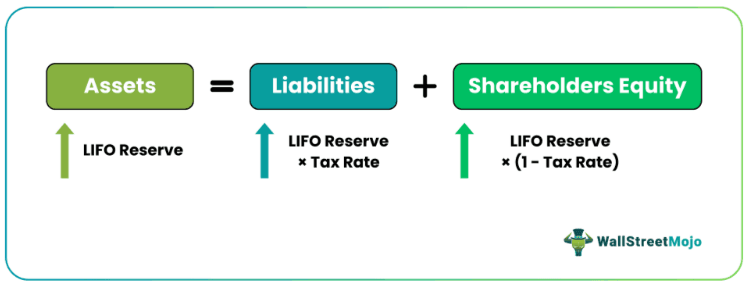

- Add the Reserve to Current Asset (Ending Inventory)

- Subtract the Income taxes on the Last in First Out Reserve from Current Assets (i.e., Cash Balance)

- Add Last in First Out Reserve (Net of Taxes) to Shareholders Equity

- Subtract the change in Last in First Out Reserve from Cost of goods sold

- Add the Income Taxes on the Last in First Out Reserve change to Income tax expenses in the Income Statement.

The above are some essential requirements during LIFO reserve adjustment, which will give the management an idea abou the closing inventory balance, how much it is able to save taxes for the company, the final asset and liability position and profitability position of the company. The investors and analysts also study these items to get a clear picture of the business.

LIFO Reserves are reported by the companies which use the LIFO method of inventory reporting as part of their financial statements in their footnotes. It holds relevance as it enables various stakeholders in the business and Analyst community to understand and compare the company’s reported profitability and various financial ratios with companies using the FIFO method of Inventory reporting in a better way.

Recommended Articles

This has been a guide to what is LIFO Reserve. We explain the formula and journal entry with examples, accounting adjustments, disclosure & LIFO liquidation. Additionally, we look at LIFO Liquidation along with its examples. You may learn more about accounting from the following articles –