Part of our Banking Ratios & Metrics guide

What is the Reserve Ratio?

The reserve ratio is the minimum percentage of the amount defined by the central bank to park aside by every commercial bank, it is a requirement that every bank must adhere to as per the regulations, and the central authority holds the right to increase or decrease this ratio as per the economic requirement.

- The reserve ratio is the minimum percentage of funds that every commercial bank must set aside, as mandated by the Central Bank’s regulations. The central authority can adjust this ratio based on economic needs.

- The reserve ratio is an essential factor in the financial system and can be used to balance the nation’s economy effectively.

- When the Central Bank lowers the reserve ratio, banks are allowed more money to lend, boosting the economy. If the intention is to reduce the cash supply and keep inflation under control, on the other hand, the reserve proportion is increased.

Calculate Reserve Requirement

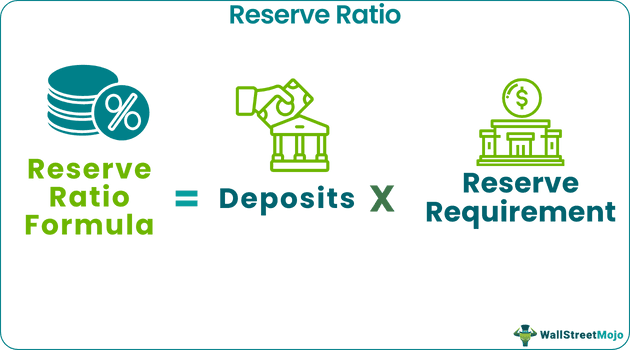

The simple and straightforward calculation of reserve requirement as it is directly correlated to the amount of deposits liability the bank has-

Reserve Ratio = Deposits * Reserve Requirement

Example: If the European Central bank (ECB), the central bank for the banks operating in the eurozone, has set a reserve requirement of 8%, and a bank has deposits of 2 billion €.

So, the bank must keep 2 billion € * 8% = 160 million € as a reserve requirement.

Reserve Requirements in the USA by Federal Bank

The below snapshot illustrates the reserve requirement by the fed for commercial banks in the USA.

Source: federalreserve.gov

- Inside limits indicated by law, the federal reserve board of governors has the sole authority over changes available for later necessities. In January 2019, the Fed refreshed its hold necessities for storehouse establishments of various sizes.

- Banks with more than $124.2 million in net exchange records must keep up a save of 10% of net exchange accounts.

- Banks with more than $16.3 million to $124.2 million must save 3% of net exchange accounts.

- Banks with net exchange records of up to $16.3 million or less don’t have a hold necessity. Most banks in the United states fall into the main class.

- The Fed set a 0% prerequisite for nonpersonal time stores and eurocurrency liabilities.

The Functioning of Reserve Ratio

- The reserve prerequisite is the reason for all the Fed’s different instruments. If the bank needs more available to meet its requirements, it can acquire from different banks. It might likewise acquire from the federal reserve rebate window.

- The cash banks acquire or loan to one another to satisfy the reserve prerequisite is federal funds. The fed fund rate is the interest they charge each other to get sustained assets. All other loan fees depend on that rate. The Fed uses these instruments to control liquidity in the financial framework.

- The higher the reserve prerequisite, the less benefit a bank makes with its money. A high prerequisite is particularly hard on small banks. They don’t have a lot to loan out in any case. The Fed has excluded small banks from the prerequisite. A small bank is unified with $16.3 million or less in deposits.

- Changing the reserve requirement is costly for the banks. It compels them to change their systems. Subsequently, the fed board occasionally changes the reserve ratio.

Effects of Change in Reserve Ratio

The following are the effects of change in reserve ratio.

#1 – Bank Credit and Money Stock

- Reserves are the level of cash that banks must hold for possible later use and not loan out. For instance, with a 10 percent save prerequisite on net exchange accounts, a bank that encounters a net increment of $200 million in these deposits would be required to build its necessary savings by $20 million.

- The bank would have the option to loan the remaining $180 million of cash, bringing about an expansion in bank credit. As those assets are loaned, they make extra deposits in the financial framework.

- The fluctuations in deposits influence the cash stock and bank credit:

- Expanding the (reserve requirement) ratio diminishes the volume of deposits that a given prerequisite level can support. Without different activities, it lessens the cash stock and raises the expense of credit.

- Diminishing the requirement leaves banks with an abundance of savings at first, which can instigate the development of bank credit and store levels and a decrease in financing costs.

#2 – Interest Rate

- Raising the reserve ratio lessens the measure of cash banks need to lend. Since the cash inventory is lower, banks can charge more to loan it. That sends financing costs up, and similarly, interest rates go down if banks have less reserve requirement and more liquidity at their disposal to lend.

- In any case, changing the prerequisite is costly for banks. Hence, national banks would prefer not to modify the necessity each time they move money-related strategies. Rather, they have numerous instruments that have a similar impact as changing the hold necessity.

- For instance, the federal open market committee sets an objective for the fed funds rate at its regular meetings. In an event when the fed funds rate is high, it costs more for banks to loan to one another medium-term. That has a similar impact as raising the reserve ratio.

Importance of Reserve Ratio

The following are the importance of the reserve ratio.

- Reserve Ratio is a crucial part of monetary policy. The federal reserve can bring down the hold proportion, for instance, to authorize expansionary money-related strategy and empower financial development.

- The decrease allows banks to loan a greater amount of their cash to other bank clients and procure premiums. These clients thus deposit the advance in their accounts, and the procedure proceeds inconclusively.

- This expansion in the supply of accessible funds brings down the cost of those funds (i.e., the lending rate), making obligations less expensive and alluring to borrowers.

- On the contrary, if the federal reserve expands the hold proportion (which leaves to a lesser extent a bank’s stores accessible for loaning), the turnaround occurs, and the federal reserve can contract the economy.

- As a method for guaranteeing the security of the country’s budgetary foundations, the monetary authority sets minimum proportions, so banks consistently have some cash close by to counteract a run. Due to mass withdrawal, banks still have sufficient funds to avoid panic among the customers.

Conclusion

Reserve Ratio is a key component in the financial system and can also be used as an effective tool in balancing the monetary structure of the nation; lastly, the central bank brings down the reserve ratio to give banks more cash to loan and lift the economy and expands the reserve proportion when it needs to decrease the cash supply and control inflation.

Frequently Asked Questions (FAQs)

What is the legal reserve ratio?

The legal reserve ratio is the minimum amount of cash banks must keep on hand from the deposits they receive. The Central Bank sets this ratio.

What is the statutory reserve ratio?

The Statutory Reserve Requirement (SRR) is the number of deposit liabilities that Licensed Commercial Banks (LCBs) must keep as a cash deposit with the Central Bank. Hence, this is mandated by the Monetary Law Act (MLA), which sets rates for the reserves LCBs must maintain with the Central Bank.

What does increasing the required reserve ratio do?

When the reserve requirement ratio is increased, fewer deposits will be supported by the same amount of reserves. Therefore, this may result in a decrease in the money stock and an increase in the cost of credit unless other actions are taken.

Recommended Articles

For more on Banking Ratios & Metrics, explore these related articles from our Banking Ratios & Metrics guide.