Part of our Option Pricing Models guide

What Are Option Greeks?

Option Greeks are variables used to measure changes in factors, such as price movement, time-value loss, and volatility of the underlying asset that affect the value of an options contract. The term ‘Greeks’ refer to Greek letters or symbols assigned to underlying parameters of the options pricing model.

Delta, Theta, Gamma, Vega, and Rho are the five variables that represent the sensitivity of the price of options to any change in their underlying security. Options Greeks determine the value of options contract. Traders can use these variables to make informed decisions about trading Option Greeks while also being aware of risks associated with it.

Key Takeaways

- Option Greeks are variables that quantify changes in parameters of an underlying asset or security, such as price movement, time-value loss, and volatility that affect the value of an options contract.

- The five Greeks are Delta (Δ), Gamma (Γ), Vega (ν), Theta (θ), and Rho (ρ). These variables have an Option Greeks formula each for calculation using the options pricing model.

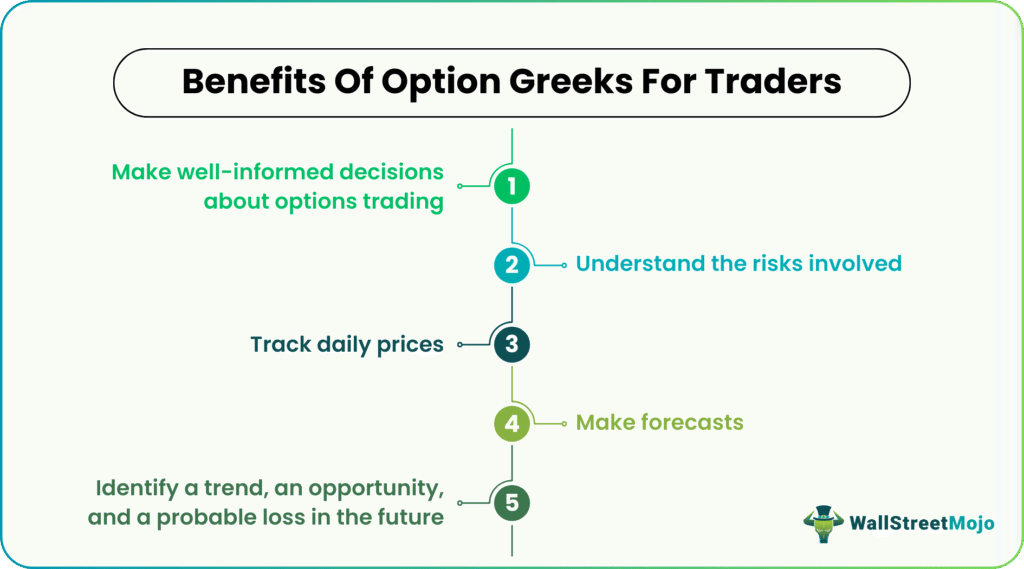

- Option Greeks determine the value of an options contract, allowing traders to make well-informed decisions about options trading while understanding the risks involved.

- Understanding Option Greeks also assist traders in keeping track of daily prices and identifying a trend, an opportunity, or a probable loss in the future.

Option Greeks Explained

Option Greeks allow investors and traders to understand the impact of factors, including the price, expiration date, and volatility of the underlying asset or security on option prices. Since these factors keep changing, traders can use theoretical pricing models to calculate Option Greeks and their impact in response to changes in the security value. Eventually, Greeks let them assess potential risks and rewards associated with their options positions.

An option is a contract to purchase or sell an underlying asset or security at a predetermined price (strike price) for a specified period (expiration date). To buy an options contract, the investor pays a fee (premium), which is a percentage of the total value of the asset. Greeks enable investors to hedge a portfolio to offset any losses in other investments and speculate on an asset’s future price movements.

The two most common types of Option Greeks are – the call option and the put option. While the call option permits an options investor to buy the underlying security, the put option allows the holder to sell the underlying asset. In other words, it dissects the intrinsic value of call and put options before examining the price movement.

How To Calculate Option Greeks?

There are five types of Option Greeks, each playing a crucial role in helping an investor make calculative trading decisions. Also, each variable has an Option Greeks formula for computation using the options pricing model:

| Delta (Δ) | Gamma (Γ) | Vega (ν) | Theta (θ) | Rho (ρ) |

| ∂V/∂S | ∂Δ/∂S = ∂2V/∂2S | ∂V/∂σ | -∂V/∂τ | ∂V/∂r |

Where,

∂ = First derivative

V = Option’s price (theoretical value)

S = Underlying asset’s price

σ = Underlying asset’s volatility

τ = Option’s time to maturity

r = Interest rate

Since multiple factors influence the options market, traders keep a tab on daily prices and make forecasts. In such scenarios, these five Option Greeks help them identify a trend, an opportunity, or a potential loss in the future. Investors can select from a range of Option Greeks calculators available online to assess the value and risks associated with trading Option Greeks.

Uses Of Option Greeks

As already stated, Options Greeks assess the impact of factors such as the underlying security’s price movement, time decay, and volatility on the option’s value. These help traders learn when and where to invest and what to expect.

| Delta | Gamma | Theta | Vega |

|---|---|---|---|

| Measures impact of any change in the price of the underlying security or asset | Measures the rate of change of Delta | Measures impact of a change in the time left for the maturity of the options contract | Measures impact of a change in the volatility of the options contract |

#1 -Delta (Δ)

It measures the change in the price (premium) of an options contract as the value of the underlying asset or security rises or falls. In simpler words, if the market rises or falls by 1 point, it will impact the option’s value. Delta calculates call (positive) and put (negative) options on the same strike price independently.

#2 – Gamma (Γ)

It essentially measures how much Delta varies as the value of the underlying asset or security increases or decreases. On the one hand, Delta tells an investor the difference in the option’s premium. On the other hand, Gamma indicates the speed of Delta’s variation. Traders can use this parameter to forecast price movements in the underlying asset.

#3 – Theta (θ)

This variable quantifies the loss in the price or premium of an options contract over time. To put it another way, when an option nears maturity, its value tends to decline. Since this parameter represents the loss of an option’s temporal value rather than its intrinsic value, it is always negative. That is why it favors sellers.

#4 – Vega (ν)

It determines the variation in the price (premium) of an option corresponding to an increase or decrease in the implied volatility of the underlying asset or security. Here, implied volatility is the projected future volatility of the underlying investment until the options contract matures. Simply put, increased volatility increases the value of put and call options, while decreased volatility decreases the value of put and call options.

#5 – Rho (ρ)

It measures the change in the option price owing to a percentage increase or decrease in the risk-free interest rates. Call options often exhibit a positive rho, and put options typically represent a negative rho.

Frequently Asked Questions (FAQs)

What do Option Greeks mean in options trading?

Option Greeks measure changes in underlying security parameters, such as price movement, loss of time value, and volatility that influence the value of an options contract. These variables carry Greek letters or symbols, hence termed Greeks.

What are the different types of Option Greeks?

The five types of Option Greeks are Delta (Δ), Gamma (Γ), Vega (ν), Theta (θ), and Rho (ρ) that use the options pricing model. Each contains a formula for calculating how much an option’s price changes as the underlying security’s value rises or falls.

Why are Option Greeks important?

Option Greeks evaluate the value of an options contract, allowing traders to make well-informed options trading decisions while also recognizing the risks involved. Knowing how to read them can help traders track daily prices, and spot a trend, an opportunity, or a potential loss in the future.

Recommended Articles

This has been a guide to Option Greeks and their Meaning. Here we discuss how to calculate option greeks and uses along with detailed explanations. You may also learn more from the following articles –

Recommended Articles

For more on Option Pricing Models, explore these related articles from our Option Pricing Models guide.