Part of our Option Pricing Models guide

What Is The Bjerksund-Stensland Model?

Bjerksund-Stensland Model is a pricing strategy used to price American options in the derivatives market. The primary purpose of this method is to act as an alternative to the Black-Scholes Model, which is usually used to price European options.

The name Bjerksund-Stensland Model originates from the works published by professors Norwegians Petter Bjerksund and Gunnar Stensland. In 1993, they developed this theory to focus more on American options. With the help of this model, pricing these options became easier. This model is mainly useful while pricing American options. Hence, it is not applied to European options.

Key Takeaways

- The Bjerksund-Stensland Model is a pricing strategy used by investors and firms to determine American option contracts’ value.

- It originated in 1993 and became visible through the works of Norwegians Petter Bjerksund and Gunnar Stensland.

- It is applied to American options to determine their value, and companies use it to find the right exercise boundary for dividend declarations.

- This model differs from other models or methods used for options pricing. It also differs from the Merton Jump Diffusion Model, as Merton Jump focuses more on asset price jumps.

- Some consider this model an extension or an improvement of the Black Scholes Model since it offers guidance on when an option should be exercised, in addition to helping with option pricing.

Bjerksund-Stensland Model Explained

Bjerksund-Stensland Model is a well-known pricing model for American options trading on the derivatives market. These options contracts allow parties to determine the underlying asset price. Also, they can exercise the contract before the expiration date. Investors also use it to determine the best time to execute an option contract.

The application of the Bjerksund-Stensland Model is visible largely for pricing American options. The model states that assets that trade frequently adhere to the geometric Brownian Motion. Plus, it also considers the probability of early exercise, which the Black-Scholes Model does not. So, using both assumptions, the model determines a breakeven point. This point acts as an optimal exercise boundary.

If investors try to execute the option contract at this point, they will suffer no loss. However, the reverse can invite a few losses. The Bjerksund-Stensland model formula is applied during the options pricing exercise. It not only calculates the option price but also determines the implied volatility of American options.

The Bjerksund-Stensland model calculator is a system that determines the price or value using specific programming tools. In short, it typically uses a dynamic model to estimate the option price. To determine the value, an option’s strike price, duration, and premium are required. In addition, investors also consider the interest rate and volatility associated with the instrument. This model is sometimes considered an extension of the Black Scholes Model because it helps investors decide if they should exercise an options contract at a given time.

Another use of the Bjerksund-Stensland model formula is to price options with constant returns, i.e., options that yield continuous or regular dividends. As dividends are crucial, the early exercise of options contracts can highly impact the overall financial health indicators.

Examples

Let us look at some examples of the Bjerksund-Stensland Model to understand how the pricing system works.

Example #1

Suppose ABC Ltd is a stock option with a strike price of $55 and an expiry of 90 days. The option premium is $3. Janice, an option buyer, considers using the Black-Scholes Model (BSM) to determine the option price. However, since it is an American option, using the Bjerksund-Stensland model calculator to calculate the price is recommended.

Considering the risk-free interest rate of 5% and the current stock price of $50, the option value, according to Black-Scholes, is $9. While the option price is available, the decision of whether it should be exercised is unclear. Using the Bjerksund-Stensland Model, Janice can determine the optimal exercise boundary. She can compute the exercise value (stock price less strike price) at different expiry dates. If the exercise value is low at 30 days, there is no use executing the option.

Example #2

Assume ABC Ltd is considering declaring dividends. They wish to announce interim or annual dividends of $3, and the Bjerksund-Stensland Model is used to calculate if this decision makes sense. The model will calculate risks and volatility. However, the company may only declare dividends at this stage if they anticipate a positive impact on its overall financial health. If a negative impact is expected, dividend declaration will be delayed.

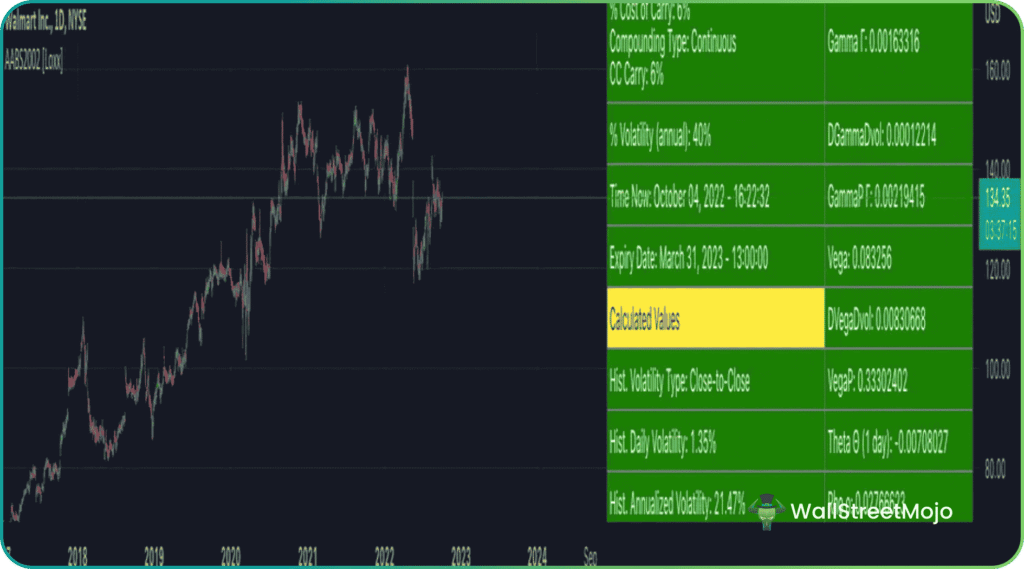

The concept can be explained further with the help of a TradingView chart, as given below. As per the chart of Walmart Inc., the maturity period is divided into two parts, and each part has a different exercise boundary. It is not only less time-consuming but also a very efficient method in terms of accuracy. There are various analytical Greeks, and they do not rely on closed-form solutions, which are typically used in the case of Black Scholes model parameters.

However, it is most suitable for daily timeframe trading. There are options to change the fonts and colors to fit the screen and make it clearer and easy to understand.

Advantages & Disadvantages

In this section, let us study the advantages and disadvantages of the Bjerksund-Stensland Model.

| Advantages | Disadvantages |

|---|---|

| It helps public companies determine whether dividends can be declared based on existing financial conditions. | It cannot be applied to options other than American options. |

| It enables the early exercise of options contracts. It can be applied to both calls and puts. | Since it primarily focuses on pricing American options, it cannot be used for other options. Hence, its usage is quite limited. |

| The Bjerksund-Stensland Model principle can be applied to implied volatility, spreads, and asset movement forecasting studies. | It involves a certain level of complexity. |

Bjerksund-Stensland Model vs Merton Jump Diffusion Model

Let us go through some differences between the Bjerksund-Stensland and Merton Jump Diffusion Model (a model for computing or estimating the “jump” in asset prices).

| Basis | Bjerksund Stensland Model | Merton Jump Diffusion Model |

|---|---|---|

| Meaning | It refers to the pricing model for American options. | It is an extension of the Black-Scholes model. |

| Objective | It allows investors to determine the exercise date for assets. | It helps determine the factors for the sudden rise in asset prices. |

| Types of Dividends | This model considers continuous dividends. | It considers dividends with varying yields. |

| Interest rates | The interest rates are on a stochastic basis. | The interest rates are risk-free. |

| Detection of Asset prices | It does not consider or study price jumps. | The model helps determine fluctuations in asset prices. |

Frequently Asked Questions (FAQs)

1. What is the difference between Monte Carlo and the Bjerksund-Stensland Model?

The major difference between these is the approach used for option pricing. The Monte Carlo Model uses random sampling to determine the option value. The Bjerksund-Stensland Model follows a closed-form solution for option valuation.

2. What is the difference between the Bjerksund Stensland Model and Black Scholes Model (BSM)?

The primary difference is that the Bjerksund-Stensland Model is used for pricing American options contracts. The Black Scholes Model helps determine the price of European options. The Bjerksund-Stensland Model is believed to be an improvement of the Black-Scholes Model.

3. How accurate is Bjerksund Stensland’s Model?

The model’s accuracy depends on the market volatility, assumptions, and the type of options being priced. In addition, the characteristics of the option also affect the accuracy.

Recommended Articles

This article has been a guide to What Is Bjerksund-Stensland Model. We explain its examples, advantages, and comparison with Merton Jump Diffusion Model. You may also find some useful articles here –