What Is A Refinance Calculator?

A Refinance Calculator is used to find the new installment amount when the borrower refinances his loan with a new interest rate. This can calculate any loan issued on a reducing interest basis. The same can be used to calculate the interest savings amount as well. In addition, this calculator also helps individuals know if they should even go for a particular refinance option or wait.

Borrowers opt for refinancing a loan only when they think they would be able to save something by switching to another loan option. Using the refinance calculator allows borrowers to compare two refinancing options available and make a choice based on what offers more monetary benefits.

How Does A Refinance Calculator Work?

Refinance calculator is a mathematical tool that helps borrowers calculate the payments they would have to make if they refinance a mortgage or auto loan. A borrower’s motive behind refinancing a loan is to save money. This is because when refinanced, the loan interest rate gets reduced to a significant extent, thereby making borrowers pay less than what they have been paying. In addition to this, the refinance option offers borrowers to shift to a fixed interest rate from any variable interest rate loan scheme.

Refinancing comes with two options. One if where borrowers can make less monthly payment over a longer period and second is paying less interest over time. This means, in both instances, borrowers will end up either paying less amount every month with more interest applicable or pay more amount every month with reduced interest rates.

When they use these calculators, they can easily calculate what option would work better for them. Therefore, decision-making becomes easier for borrowers. As this calculator involves a comparison between two loans, it is divided into two sections – one section makes calculations related to original loan and the other makes calculations related to the new loan option under consideration. The figures required are obtained and compared to ensure the borrowers make wiser decisions.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Elements

A refinance calculator works the best when the data entered within the calculator are accurate. Incorrect inputs lead to incorrect results. Hence, one must ensure putting in information correctly to get the accurate results. The elements that are commonly included in this calculated are:

- Outstanding loan balance, which refers to the amount that is due for payment in the original loan scheme. This is the amount that borrowers opt to refinance.

- New rate of interest: This is the new annual rate of interest applicable to the amount to be borrowed.

- Time period to which the original loan would continue.

- Frequency of payments, which marks the intervals at which the repayments would be scheduled. This could be annually, semi-annually, and monthly, etc.

Formula

The formula on which the refinance calculator work is mentioned below:

Wherein,

- P is the outstanding loan balance.

- R is the new rate of interest.

- N is the number of periods for which the existing loan will continue.

- F is the frequency with which the loan shall be repaid, i.e. annually, semi-annually, monthly, etc.

There could be scenarios wherein the borrower has taken the loan during the business cycle when there is a high-interest rate prevailing in the market. Due to requirements at that moment, the borrower could not wait further to delay the processing of a loan. Now, assume that the interest rate has come down and the borrower wishes to refinance the loan at a lower rate of interest, and when he does the same, he would be saving the interest outflow, which will reduce the cost of the purpose for which he had borrowed the loan. When the borrower refinances at a lower interest rate, the advantages would be a reduced interest rate and an installment amount. Also, in certain cases, the borrower can repay it sooner if that option is available. Hence, this calculator can calculate the refinanced installment amount and the savings amount.

How To Calculate?

For a mortgage or auto loan refinance calculator to work efficiently, it is important that users use it properly. Listed below are some of the standard steps to be followed to use this tool for effective results. Let us have a look at them:

- First, one needs to determine the existing installment, an initial loan taken, the number of years for which the loan was taken, and the interest rate.

- The borrower should have an option to refinance the loan. Then we should calculate the loan’s outstanding balance if any repayment was made in between. The same can be calculated using the table method, as provided in the example below.

- Now, from the above step2, determine the outstanding principal balance amount and the remaining term of the loan (here, we assume that the loan period will remain the same).

- Multiplying the principal amount by a new interest rate using the above formula.

- Continuing step 4, compound the same by a new rate of interest.

- As a final step, discount the result obtained in step 5 per the formula discussed above, which shall be a new installment amount.

To determine the savings, one needs to calculate the difference between the existing and new installments calculated in step 6 and multiply the same with the remaining loan period.

Example

Let us consider the following instance to understand how it works:

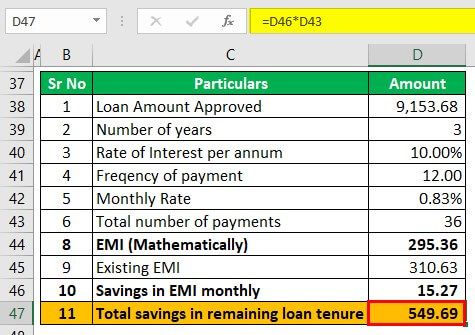

Mr. Kedia had purchased a laptop for $13,500, fully financed by Bank of Asia. The Bank has provided him with a five-year loan with a reducing rate method. The rate of interest that the bank will charge is 13.50%, which was charged high because Mr. Kedia’s credit score was below par. However, after paying the installment for two years without any default, the credit score of Mr. Kedia improved, and the bank offered to refinance his outstanding balance at 10.00%, to which Mr. Kedia agreed. The existing installment amount is $310.63, payable in 60 installments.

Based on the given information, you are required to calculate the new periodical installment for the remaining tenure and the savings he would make.

Solution:

We will now summarize the information that we are given.

To calculate the new installment amount, we are first required to calculate the outstanding balance of the loan borrowed, and for the same calculation is below:

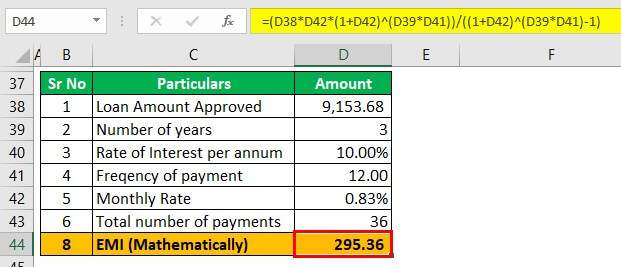

The monthly interest rate now will be 10.50% / 12, which is 0.83%, and the outstanding balance of the loan as calculated above at the end of 2 years is 9,153.68 with a loan period of 3 years remaining, which would be 36 months.

At the end of 2 years

- = [9,153.68 x 0.83% x (1 + 0.83%)^3×12 ] / [ (1 + 0.83%)^3×12 – 1 ]

- = 295.36

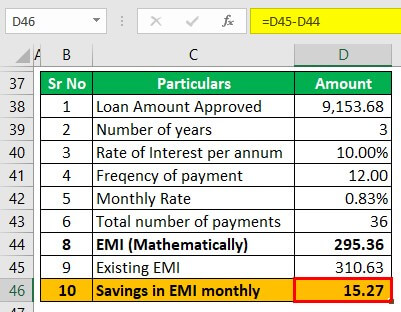

- = 310.63 – 295.36

- = 15.27 per month

- = 36 * 15.27

- = 549.69

Benefits

There are certain benefits of using the refinance calculator. Let us have a look at them in brief below:

- It helps compare two refinancing options to help borrowers make wise decisions for better benefits.

- The calculator asks preferences of borrowers. This means, they can decide if they would like the calculations to be made for more monthly payment with less interest payment or less monthly payment with more interest payment.

- It makes available all elements for which the data is required. The users only need to put in figures for calculation. No manual calculation is required. Everything is conducted automatically.

- One can try calculating figures selecting different options to ultimately find out what suits them the best. For example, they can change the length of loan to check the repayment figures, or they might lower the monthly payment to check how much interest they would have to pay altogether. Checking different options allow them make better choice.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Recommended Articles

This has been a guide to what is Refinance Calculator. Here, we explain the tool along with its formula, how to calculate it, examples, and benefits. You may also take a look at the following useful articles –