What Is A Mortgage Points Calculator?

Mortgage Points are mostly calculated based on the total loan amount, and a single point is equivalent to 1% of the loan amount. The mortgage points calculator lets the borrower decide whether he should opt for an upfront payment and reduce its interest rate and hence the monthly installment further; he has to conduct a cost-benefit analysis and make decisions accordingly.

If the borrower can afford to purchase the mortgage points, he needs to figure out if the deal is worth it, or he can take a financial advisor’s help. There is a general rule of thumb: the longer the loan the borrower keeps, the mortgage points will become more attractive. Also, one needs to calculate the payback period of the upfront amount paid while making the decision.

Mortgage Points Calculator Explained

The mortgage points calculator is a method devised for borrowers so that they can clearly take borrowing related decisions related to down payment or monthly installments. Such a calculator provides information based on the data that the user provides to it. Apart from calculation of points or deciding on the amount of down payment, this method also gives suitable guidance regarding mortgage insurance or any other related costs that the borrower has to bear.

The mortgage points can also be referred to as discount points and is actually a kind of interest prepaid. When a borrower buys such mortgage points they can decide whether to reduce their monthly payment on instalments or accept a lower interest rate, using the mortgage points calculator excel.

It should be noted that the value of one mortgage point is the same as 1% or the total amount of the loan. Therefore, this point can be used either to clear off a part of the interest or reduce the instalment. This process is also sometimes called “buying down” of interest.

Certain lenders offer the facility of paying the points along with closing points of buying a property. The closing points can be any expenditure or fee paid by the borrower when they get their property, which may be some standard ones like title fee, appraisal fee, insurance amount for first year, etc. There can also be other elements, depending on the loan type or the requirements of the jurisdiction.

For each point accepted by the borrower, along with the closing cost, the mortgage Annual Percentage Rate (APR) will come down. This will automatically lead to reduction in instalments.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

How To Calculate?

One needs to follow the below steps in order to calculate the Mortgage Points benefits, using the mortgage points calculator excel.

Calculate the amount of upfront payment, which would be the percentage of the loan amount, and multiply the same by the number of points the borrower has chosen to pay upfront.

Now, enter the loan amount first, which is the principal amount:

Multiply the principal by the rate of interest applicable without points.

We need to compound the same by rate until the loan period.

We now need to discount the above result obtained in step 3 by the following:

After entering the above formula in excel, we shall obtain installments periodically.

Repeat steps from 2 to step 5 but this time with the interest rate applicable with points.

- Now, subtract values arrived in step 6 and step 7 that shall give you the monthly savings amount.

Examples

Let us understand the concept with the help of some suitable examples, as given below:

Example #1

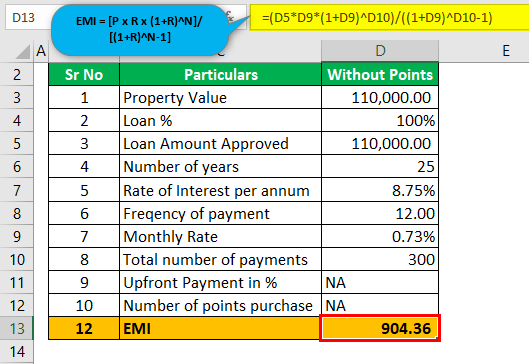

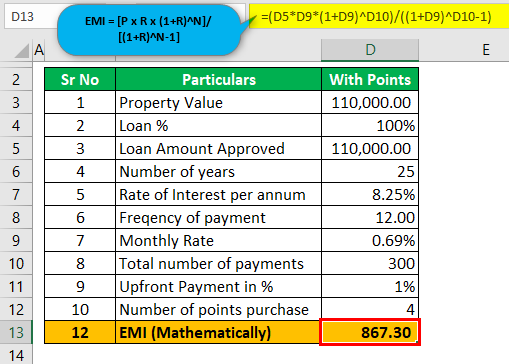

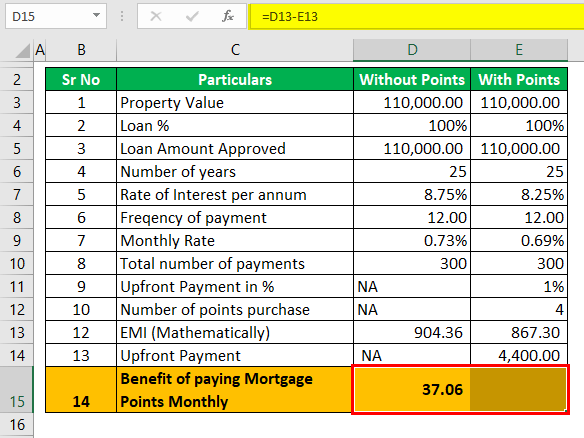

Karry had purchased the house with a Mortgage loan. The loan amount was $110,000 and was taken for 25 years. Further, the rate applicable was 8.75%. Karry complained about the higher rate being charged; the bank was currently offering new home loans at 8.50%.

The bank manager told her that she could even be shifted to a rate of 8.25% if she opts for Mortgage points. On inquiry, she came to the conclusion that purchasing one mortgage point will equal 1% of the loan amount, and she has to purchase four mortgage points.

You are required to calculate Mortgage points to benefit from this.

Solution:

- We need to calculate the EMI amount with points and without points interest rate.

- The number of installments is 25 years, but since it is monthly outgo, the number of payments required to be paid is 12*25, which is 300 equal installments.

- And lastly, the interest rate is 8.75% fixed, which shall be calculated monthly, which is 8.75%/1 two, 0.73%, and 8.25%/1,2, which is 0.69%.

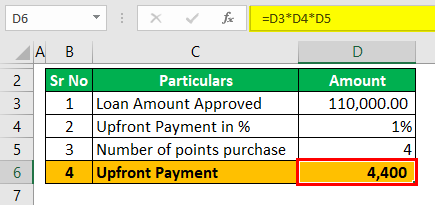

Upfront Payment Calculation:

Loan Amount x Upfront percentage x Number of points

$110,000 x 1% x 4 = $4,400

Now we shall use the below formula to calculate the EMI amount.

Without Points:

EMI = [P*R*(1+R)^N]/[(1+R)^N-1]

= [110,000*0.73%*(1+0.73%)^300]/[(1+0.73%)^300–1]

= 904.36

With Points:

EMI = [P x R x (1+R)^N]/[(1+R)^N-1]

= [110,000*0.69%*(1+0.69%)^300]/[(1+0.69%)^300–1]

= 867.30

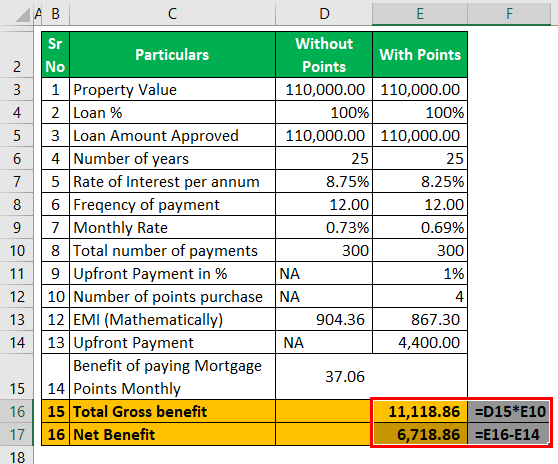

Benefits per month: EMI without points – EMI with points

= 904.36 – 867.30

= 37.06

Therefore, 34.81 * 300 which shall equal to $8,354.29 less $4,400 which is net benefit of $3,954.29

Example #2

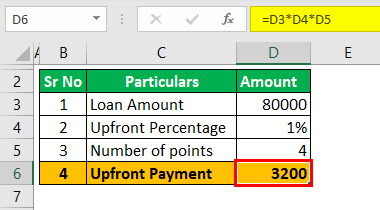

Mr. KJ has a current loan outstanding for $80,000, which he initially financed at 7.89%, and ten years are yet left for the loan to be fully paid. Now the Bank has recently launched for their existing borrowers to purchase mortgage points and reduced their interest rate and, subsequently, monthly installment. The scheme detail is below:

| Cost of Per Mortgage Points | 1% | 1% | 1% |

| Points Purchased | 1 | 4 | 8 |

| Rate | 7.75% | 7.26% | 6.80% |

Mr. KJ decides to purchase four mortgage points. Based on the given information, you are required to determine whether it was worth the deal.

Solution:

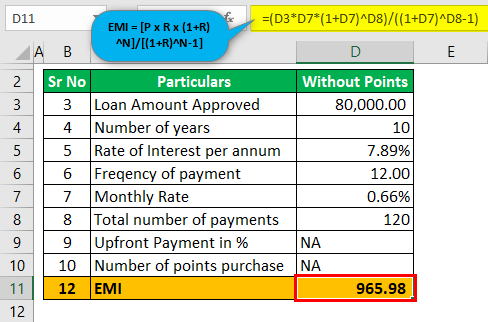

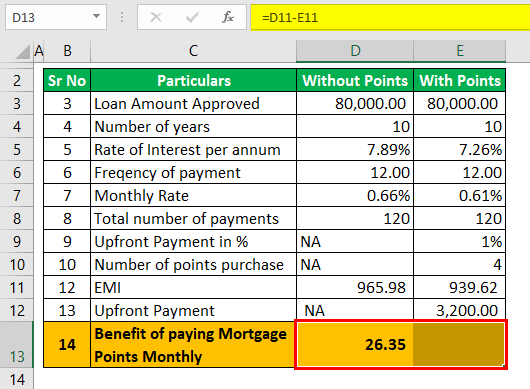

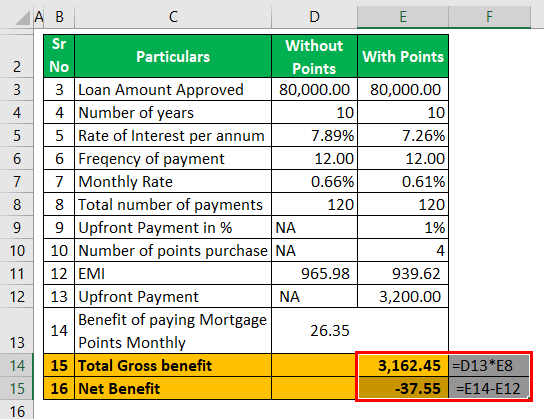

We need to calculate the EMI amount with points and without points interest rate. The number of remaining installments is ten years, but since it is monthly outgo hence the number of payments required to be paid is 12*10, which is 120 equally installments, and lastly, the rate of interest is 7.89% fixed, which shall be calculated monthly which is 7.89%/12 which is 0.66% and 7.26%/12 which is 0.61%.

Upfront Payment Calculation

Loan Amount x Upfront percentage x Number of points

$80,000 x 1% x 4 = $3,200

Now we shall use the below formula to calculate the EMI amount.

Without Points:

EMI = [P x R x (1+R)^N]/[(1+R)^N-1]

= [80,000*0.66%*(1+0.66%)^120 ]/[(1+0.66%)^120–1]

= 965.98

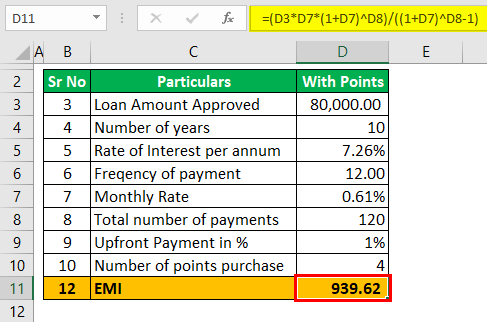

With Points:

EMI = [P x R x (1+R)^N]/[(1+R)^N-1]

= [800,000*0.61%*(1+0.61%)^120]/[(1+0.61%)^120–1]

= 939.62

Benefits per month: EMI without points – EMI with points

= 965.98 – 939.62

= 26.35

Therefore, 26.35 x 120 which shall equal $3,162.45 less $3,200 which is a net loss of $37.55.

Hence, it doesn’t affect if he buys four mortgage points; in effect, he suffers a loss, so he should avoid buying four.

In this concept, it is important to evaluate the situation based on the calculated numbers. Since, by utilising the points, the borrower is paying more amount of down payment, this will lead to reduction in the interest rates of the loan and this is highly beneficial for long term.

If the homeowner plans to keep the home for many years, then its value will appreciate over the years, helping the borrower reach the break-even point, in which the interest that the borrower is able to save will cover the initial extra payment that they made using the points. A short-term plan to keep the home may not provide this benefit.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Recommended Articles

This has been a guide to what is Mortgage Points Calculator. We explain how to calculate it along with some suitable examples. You may also have a look at the following useful articles –