Part of our Financial Calculators guide

Total Loan Cost Calculator

Total Loan Cost Calculator can be used to calculate the cost of the loan after repaying the same until the end of the period. It meticulously computes the entire cost of a loan, including the interest rates and fees. This enables borrowers to make mindful decisions, fostering financial prudence and empowering them with an understanding of their financial commitments.

This is a superset calculator for all kinds of loans wherein a fixed rate of interest is applied, and that includes Home loans, student loans, car loans, education loans, etc. This calculator will calculate the installment amount as well as the total loan cost by multiplying the installment amount with the number of years and frequency for which that shall be paid.

Total Loan Cost Calculator Explained

The Total Loan Cost Calculator serves as an invaluable tool for both borrowers and lenders. For borrowers, this calculator offers a comprehensive view of the entire cost associated with a loan, going beyond just the principal amount. It factors in interest rates, fees, and other charges, enabling borrowers to make informed decisions regarding their financial commitments.

Lenders also benefit from the Total Loan Cost Calculator as it fosters transparency and trust with borrowers. By providing a clear breakdown of all costs, lenders establish a more open and honest relationship with borrowers, which is crucial for the long-term success of the lending process.

Let us understand how the calculator helps both borrowers and lenders through a detailed individual discussion.

The calculator empowers borrowers to:

- Understand the full financial implications of a loan.

- Easily compare different loan offers to choose the most cost-effective one.

- Plan and budget for the total cost of the loan.

The calculator aids lenders in:

- Enhance transparency by clearly communicating all costs associated with the loan.

- Stand out by offering borrowers a tool to make well-informed choices.

It is important to consider the full picture beyond the principal amount to assess the actual cost of the loan. Therefore, the impetus placed on the terms and conditions must be high to ensure no additional charges or hidden fees are charged.

It is always wise to consider a few options from different banks or lenders before making the final choice based on the most favorable terms, which also include a more convenient repayment schedule and good after-sale services such as assistance with extension or pre-closure of the loan, etc.

Formula

The formula for calculating Total Loan Cost is as below:

(L * R * (1+R)n*F) / ((1+R)n*F-1)

Wherein,

- L is the loan amount

- R is the rate of interest per annum

- n is the number of periods for which the loan is required to be paid

- F is the frequency for which interest is going to be paid out

People dream of buying houses, luxury cars, etc. Butnot everyone is fortunate enough to have funds to buy them, and thus, they opt for a loan wherein the cost is involved. The cost comes in the form of interest, which again varies from financial institution to financial institution. The loan could be used for a house, vehicle, education, etc. This calculator can be used to calculate the total cost of the loan, which is the amount paid in total versus what the amount was borrowed, and the difference would be the interest payment.

How to Calculate?

One needs to follow the below steps in order to calculate the total cost of the loan.

Step #1 – First of all, determine the loan amount that has to be borrowed. A financial institution generally lends more loan amounts to those who have a better credit score and lends lower amounts to those who don’t have a good credit score. Enter the loan amount as required.

Step #2 – Determine the rate of interest which shall be applicable and also the frequency and accordingly find out the rate to calculate the cost of interest. For example, if the rate of interest is 12% per annum, and if the compound frequency is monthly, then the rate of interest would be 12% / 12, which is 1%.

Step #3 – Multiply the loan amount by the equivalent rate of interest that was determined in step 2.

Step #4 – Now, we need to compound the same by the rate that was determined in step 2 until the end of the loan period.

Step #5 – We now need to discount the above result obtained in step 4 as given in the formula.

Step #6 – After entering the formula, which was discussed above, we shall obtain installments periodically.

Step #7 – Now multiply the installments by a number of periods and frequency to determine the total cost of the loan.

Examples

Now that we understand the basics and intricate details of the concept, let us apply the theoretical knowledge to practical application through the examples below.

Example #1

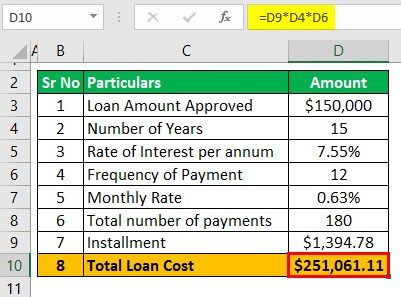

Mr. N wants to set up a business wherein the biggest expenditure is the cost of machinery and for which he doesn’t have funds. Hence, he approached the bank for a term loan for $150,000 and provides machinery as collateral. The bank agrees to provide term loans for 15 years, and the rate of interest will be 7.55% which will be compounded on a monthly basis. However, due to the festive offer, the bank will not charge any processing fees for the loan.

Based on the given information, you are required to calculate what shall be the cost of the loan to Mr. N for purchasing machinery on the term loan.

Solution:

We need to calculate the installment amount; for that, we shall first calculate the loan amount, which is $150,000. The number of periods required to be paid is 15 years, but since Mr. N is going to pay on a monthly basis the number of payments that he shall be required to pay is 15*12, which is 180 equally installments and lastly, the rate of interest is 7.55% fixed which shall be calculated monthly which is 7.55%/12 which is 0.63%.

| Sr No | Particulars | Amount |

|---|---|---|

| 1 | Loan Amount Approved | $150,000 |

| 2 | Number of Years | 15 |

| 3 | Rate of Interest per annum | 7.55% |

| 4 | Frequency of Payment | 12 |

| 5 | Monthly Rate | 0.63% |

| 6 | Total number of payments | 180 |

Now we shall use the below formula to calculate the installment amount.

- = (150,000 * 0.63% * (1 + 0.63%)15*12 ) / ( (1 + 0.63%)15*12 – 1 )

- = 1,394.78

Therefore, the Installment amount for Mr. N for 15 years on the loan amount 150,000 shall be 1,394.78

The calculation of the total loan amount for Mr. N is as follows:

- = 1,394.78 * 15 * 12

- = $251,061.11

Example #2

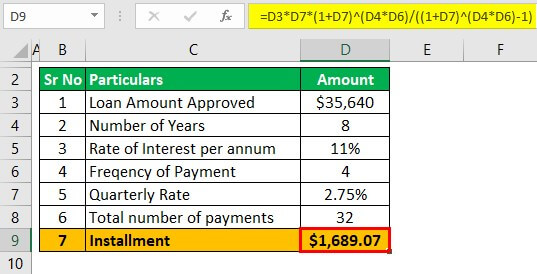

Mr. Gomzi wants to pursue higher education in a renowned university wherein the total estimated cost will be $35,640. However, since he lacks funds, he approaches a bank to borrow a loan. The bank charges 11% interest per annum, which shall be compounded quarterly, and the loan period will be for 8 years. The bank has no charges system for an education loan, but however, it charges 3% pre-penalty charges.

Based on the given information, you are required to calculate the total cost of the loan, and what amount would Mr. Gomzi be paying only in the form of interest?

Solution:

We need to calculate the Installment amount; for that first, we shall calculate the loan amount, which is $35,640. The number of periods it is required to be paid in 8 years, but since here Mr. Gomzi is going to pay on a quarterly basis hence the number of payments that he shall be required to be paid 8*4, which is 32 equally installments and lastly, the rate of interest is 11.00% fixed which shall be calculated quarterly which is 11.00%/4 which is 2.75%.

| Sr No | Particulars | Amount |

|---|---|---|

| 1 | Loan Amount Approved | $35,640 |

| 2 | Number of Years | 8 |

| 3 | Rate of Interest per annum | 11% |

| 4 | Frequency of Payment | 4 |

| 5 | Quarterly Rate | 2.75% |

| 6 | Total number of Payments | 32 |

Now we shall use the below formula to calculate the installment amount.

- = (35,640 *2.75% * (1 + 2.75%)8*4)/ ((1 + 2.75%)8*4 – 1 )

- = 1,689.07

Therefore, the Installment amount for Mr. Gomzi for 8 years on the loan amount 35,640 shall be 1,689.07

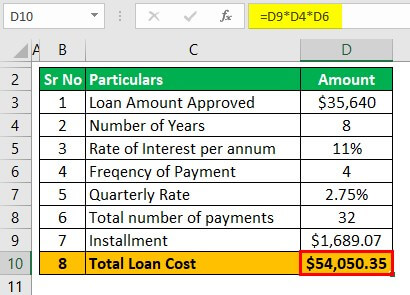

The calculation of the total loan amount for Mr. Gomzi is as follows:

- = 1,689.07 * 8 * 4

- = $54,050.3

Total interest outgo equals to $54,050.35 – $35,640 which is $18,410.35

How To Reduce?

Even though each individual might have different strategies to reduce the overall cost, by incorporating these strategies, borrowers can actively work to minimize the total loan cost, saving money and fostering financial well-being in the long run.

- A higher credit score often leads to lower interest rates, reducing the overall cost of the loan.

- Compare interest rates from various lenders to secure the most favorable terms.

- Engage in discussions with lenders to negotiate or waive certain fees associated with the loan.

- Shorter loan durations may have higher monthly payments but can significantly reduce the overall interest paid.

- A substantial down payment can lower the principal amount, reducing both interest and overall cost.

- If interest rates drop or your credit improves, consider refinancing to secure a lower rate and decrease the total loan cost.

- Select a loan type that aligns with your financial goals, whether it’s a fixed-rate or adjustable-rate mortgage.

- Set up automatic payments to avoid late fees and potentially secure interest rate discounts.

- Apply unexpected financial gains, like tax refunds or bonuses, to the loan principal to expedite repayment and reduce interest charges.

Recommended Articles

This has been a guide to Total Loan Cost Calculator. Here we explain the formula, how to compute and reduce the total cost of a loan in detail. You may also take a look at the following useful articles –