What Is An Additional Payment Calculator?

Additional Payment Calculator is a tool that helps borrowers check the amount of additional payments made for a loan that could shorten the repayment length, thereby helping them save significantly on interest payments. It can be used for any kind of loan, be it as a mortgage or student loan additional payment calculator.

The Additional Payment Calculator is very useful to borrowers, especially when they plan to increase their installment amount to save on interest payments and pre-pay their loan early. This calculator shall help them identify how much they will save had they not made any additional payment. The borrower shall be able to determine whether his decision to make additional payment is worthwhile.

Additional Payment Calculator Explained

An additional payment calculator is a type of calculator wherein the borrower can determine if they quick up their payments or start paying an additional amount periodically, then how much they would save and how their balance loan tenure shall be impacted.

Calculating the additional payment allows borrowers to find out the savings they can make by repaying the loan earlier, that is, through an additional amount added in every installment. This shall help save the interest and reduce the loan term.

Having an additional amount reserve for mortgage or loan repayments on a recurring basis allows borrowers to pat extra amount to save on interest for an elongated term. However, for the calculator to work efficiently, it is important to enter accurate data or information required for the calculation.

The tool asks for some of the details to ensure the calculation is efficiently done to avoid misleads. The information to be entered for the calculator to work properly and accurately has been mentioned below:

- The first one is the type of loan. User must enter the loan they have obtained. Based on whether it is a purchase loan taken to buy a property or an asset or it is a refinance option for mortgage refinancing, the calculation is done.

- For a purchase loan, users need to enter the amount paid.

- With purchase price, one must put in the down payment amount, which is a certain percentage of the wholesome amount paid to purchase a property.

- Then, users must enter amounts, like current loan balance, monthly principal amount, and monthly interest payment.

- Then, the next on the list of information asked is the term of the loan repayment.

- The users must mention the interest rate.

- The next thing that users need to focus on is the extra payment type, which specifies if they would prefer making monthly additional payments or a lump sum extra amount for the purpose.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Formula

The formula for calculating Additional Payment is not quite simple, and it requires certain steps below:

First, find out the present value of the outstanding balance on the loan

PV = P * [1 – (1+r)-n / r]

Next would be to find out the tenure with the new installment amount

nPVA = Ln [ (1 – PV(r) / P)-1] / Ln (1+r)

then, nPVA x (Installment Amount + Additional Payment per Period)

Wherein,

- FV is a future value of the balloon amount

- PV is the present value of Outstanding Balance

- P is the Payment

- P’ is the new Payment

- r is the rate of interest

- n is the frequency of payments

- nPVA is the number of periodical payments

How to Use?

One needs to follow the below steps to calculate the monthly installment amounts.

Step #1 – First, a borrower needs to determine the current loan outstanding balance, which is nothing but finding out the present value of the mortgage.

Step #2 – Now determine the new installment amount, which is the sum of the existing installment amount and the additional payment that the borrower things to make.

Step #3 – Use the nPVA formula to determine when the remaining loan will be paid off.

Step #4 – Multiply the nPVA calculated in step 3 by the new installment calculated in step 2.

Step #5 – Calculate the total value of the installment already paid by multiplying the existing installment by the number of periods for which the same has been paid.

Step #6 – Take the sum of values arrived in steps four and step 5, which shall be the total outgo if additional payment is made.

Step #7 – Multiply the existing installment with a total number of periods.

Step #8 – Subtract Value arrived in step 7 by step 6, which shall yield the savings done by making additional payment.

Examples

Let us consider the following instances to understand how this calculator work be it for mortgage or for student loan additional payments:

Example 1

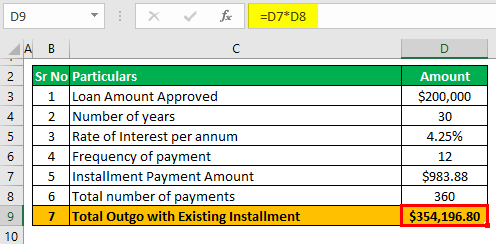

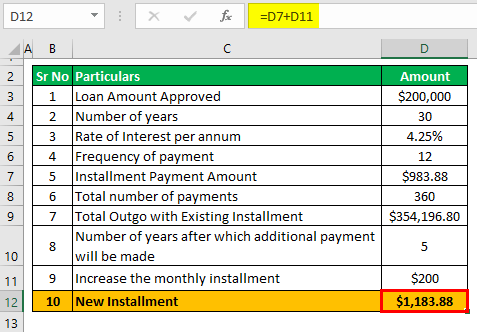

Mrs. Yen Wen has taken a mortgage loan for $200,000 for 30 years, and the rate of interest, which applies to the same, is 5%. Since she is an employee of the bank, she is eligible for a rebate on interest to the tune of 0.75%. Her monthly installment is $983.88 based on a current fixed rate. She would be eligible for promotion next year and expects a decent hike. She feels that she would be able to increase the monthly installment by $200, and she feels that she would be able to save a substantial amount of interest, and she would be able to close the loan earlier than the current. It has been four years since she has been paying the same monthly installment, and she has not defaulted on any of the installments.

Based on the given information, you are required to calculate the savings she would make on her mortgage loan and by what span she can expect to close the loan based on a new installment amount.

Note: You can ignore the time value of money since her additional payment starts from the end of year 5.

Solution:

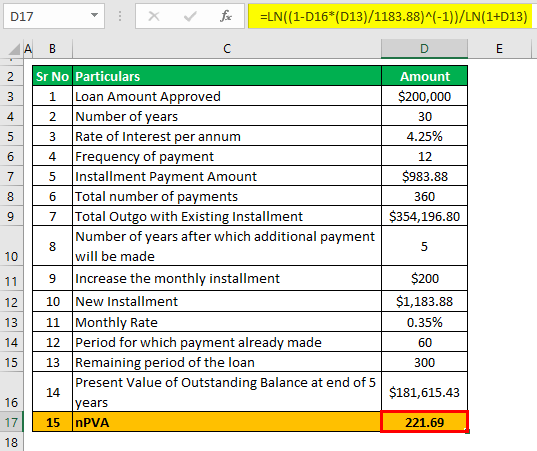

We are given here; that the existing monthly installment she is paying is $983.88, which must be paid until 30 years. Hence, her total outgo would, if she continues to make the existing installment, will be $983.88 x 30 x 12, which is $354,196.72

Now, after five years, she wants to increase the monthly installment amount, which is $983.88 + $ 200, which equals $1,183.88.

We will now calculate what savings she shall make if this additional payment is made.

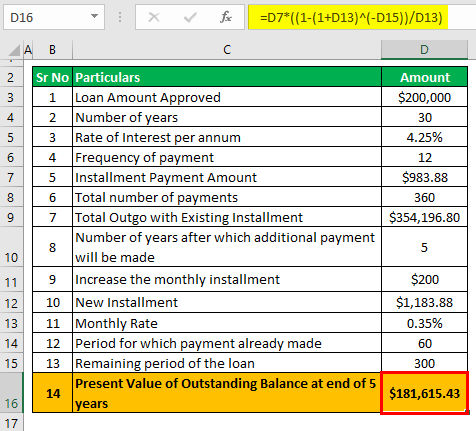

Rate of interest applicable on monthly basis = (5.00% – 0.75%) / 12 = 0.35%

The remaining period will be (30 * 12) – (5 * 12), which is 360 – 60, 300.

We need to calculate the present value of the current outstanding balance, which can be calculated per below formula:

PV = P * (1 – (1+r)-n / r)

- = $983.88 * [1 – (1+0.35%)-300 / 0.35%]

- = $181,615.43

Now since we have the Present Value of the outstanding loan balance at the end of 5 years, we need to Calculate the period within which the loan can be closed with the new installment amount.

nPVA = Ln [ (1 – PV(r) / P’)-1] / Ln (1+r)

- = Ln [ {(1- 181,615.43 x (0.35%) / 1,183.88}-1] / Ln (1+0.35%)

- = 221.69

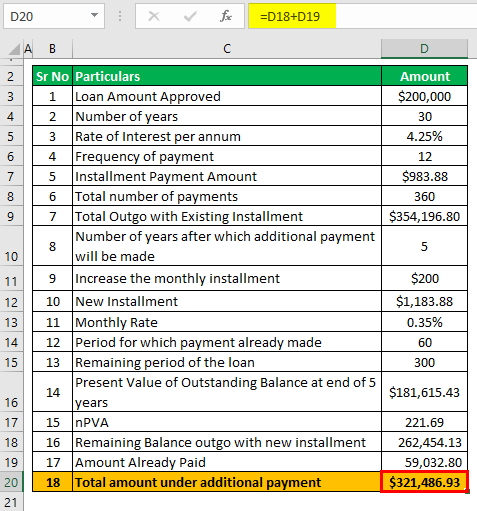

Now we shall calculate the total outgo with the new installment, which is

New installment * nPVA i.e. 1,183.88 * 221.69 which equals to $262,454.13 and amount that is already paid which is $983.88 x 60 which is $59,032.80, and therefore the total amount paid under additional payment installment shall be $262,454.13 + $59,032.80 which is equal to $321,486.93

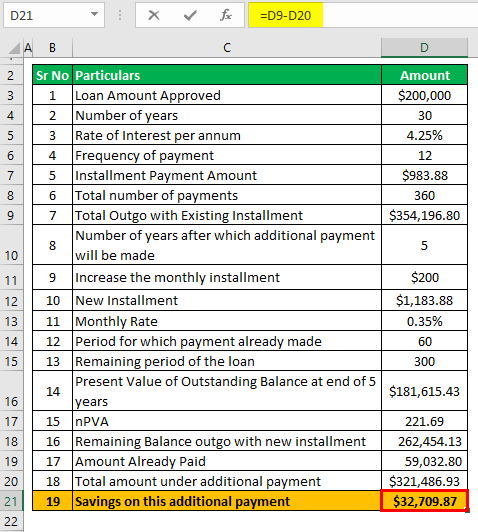

Therefore, savings on this additional payment will be $354,196.72 less $321,486.93 which is $32,709.87.

The number of loan payment periods shall be reduced by 300 – 221.69, equal to 78.31 months, and in years it is six years and six months.

Example 2

Stella, who borrowed applied and received a mortgage loan, decides to shorten her loan period and save herself from paying more interest. Her friend, George, tells her about the biweekly mortgage payment options. Under this, she would not require making full monthly payment. Instead, she would be allowed to pay half of the monthly payment every two weeks.

While she pays in full for few months, there are extra payments in the longer months in equal halves. This counts to additional payments, thereby reducing the length of the loan term and helping her save on interests payments.

Her loan amount was $250,000 with loan term of 30 years at an annual interest rate of 7% and she decides to pay $1,000 extra. When she uses the additional payment calculator, she figures out the amount she could save by making this extra payment would come to $207,206.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Importance

By using additional payment calculator, users can explore their benefits both in terms of saving money as well as saving on the term of loan repayment. Borrowers can save on the interest payment if they could clear their outstanding principal and interest payments before the expiration of the loan term. This saved money, in return, could be used by individuals in serving other purposes requiring monetary funds.

In addition, the term of loan comes to an end earlier than fixed or expected. As a result, individuals get more span of time living a life free from financial burdens. The best part is that these financing options come in different alternatives, which borrowers can choose from to ensure convenient repayment. These options include weekly, biweekly, semi-monthly, monthly, bi-monthly, quarterly or annually.

Recommended Articles

This has been a guide to what is Additional Payment Calculator. Here, we explain the concept along with its formula, how to use it, examples, and importance. You may also take a look at the following useful articles –