Part of our Revenue Recognition guide

Trade Receivables Meaning

Trade receivable is the amount the company has billed to its customer for selling its goods or supplying the services for which the amount has not been paid yet by the customers and is shown as an asset on its balance sheet.

Trade receivables is the accounting entry in an entity’s balance sheet, which arises due to the selling of the goods and services on credit. Since an entity has a legal claim over its customer for this amount and the customer is bound to pay the same, it classifies as a current asset in the entity’s balance sheet.

Trade Receivables Explained

Trade receivables, also referred to as accounts receivables, is the amount that a business is due to receive in exchange for the goods and services it has sold to its customers. It is called trade receivables as it results out of the trade dealings between a business and its clients/customers.

These records account for the most significant asset figures for any business. This is because the businesses normally deal in credits with clients who get the products delivered and pay for them in the next cycle.

Trade receivables in balance sheet are reflected under the assets section. This is because as the companies have already sold the items to their customers, they know that they would receive the due payment in a couple of days. Given the confirmation they have, the businesses consider it as an asset. Plus, it is considered mong the businesses’ current asset as the cash conversion cycle for these records is small. The balance sheet of the company also has non-trade receivables included, which is different from the trade receivables. The non-trade receivables are the amount that firms are likely to gain through tax rebates, insurance claims, etc.

Process

Accounts receivables are very critical for the liquidity of companies and, many a time, become the sole reason for Companies becoming bankrupt. An enterprise’s liquidity analysis comprises a company’s short-term financial positions and its ability to pay its short-term liabilities.

One of the most important metrics we look at while analyzing the liquidity positions of Companies is the cash conversion cycle. The Cash conversion cycle is the number of days which an enterprise takes to convert its inventory into cash.

The above picture explains it in more detail. For an enterprise, it starts with the purchase of inventory, which may be on cash or credit purchase. Then, the enterprise converts that inventory into finished goods and makes sales. The sales are made with cash or credit. The sales made on credit are recorded as trade receivables. So the cash conversion cycle is the total number of days it takes for an enterprise to convert its inventory into final sales and cash realization.

The formula to calculate the cash conversion cycle is as below:

The above formula shows that a Company with a significantly higher proportion of trade receivables will have higher days’ receivables and, therefore, a higher cash conversion cycle.

Note: Of course, the cash conversion cycle depends on the other two factors, also which are Days inventory outstanding and Days payables outstanding. However, here to explain the impact of receivables, we have kept the other two parameters indifferent.

A higher cash conversion cycle for an enterprise may lead to a significantly increased working capital loan requirement to meet its short-term demand for day-to-day operations. Once such receivables level reaches an alarming degree, it may create serious trouble for the enterprise creating short-term liquidity issues where the company will not be able to fund its short-term liabilities, which may further lead to suspending the company’s operations.

Trade Receivables Explained in Video

Formula

The mathematical expression that helps obtain the trade receivables figures is mentioned below:

Trade Receivables = Debtors + Bills Receivables

Where,

- Debtors are bills to be received that are still outstanding on the due date.

- Bills receivables are agreement between businesses and customers in which the latter agrees to pay a specific amount without a period to the former in exchange for the goods and services purchased from them.

Additionally, net trade receivables is calculated by summing up the allowances, discounts, returns, and collections and then subtracting the resultant from total credit sales for that particular period.

Examples

Let us consider the following examples to see what is trade receivables and how it is recorded:

Example #1

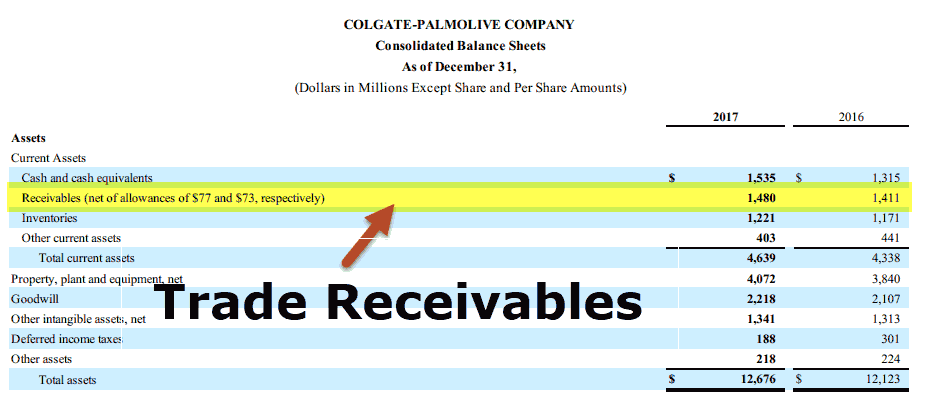

Below is the standard format of the balance sheet of an enterprise.

source: Colgate SEC Filings

It is generally classified under the Current Assets in a Balance sheet.

Example #2

ABC Corporation is an electrical equipment manufacturing company. It recorded sales of USD 100 billion in FY18, with 30% sales on credit to its Corporate Customers. Accordingly, the trade receivables accounting entry for the transaction in its balance sheet will be as below:

Accounts Receivables in the above example are calculated below:

| Particulars | Billion USD |

|---|---|

| Total Sales in FY18 | 100 |

| Credit Sales | 30% |

| Account Receivables / Trade Receivables | Total Sales *% of Sale on Credit |

| Account Receivables / Trade Receivables | 100*30% |

| Account Receivables / Trade Receivables | USD 30 Billion |

In this example, accounts receivables will be recorded as USD 30 billion in the current asset head in the Balance Sheet.

Reconciliation

Reconciliation of trade receivables is an important aspect whereby the outstanding bills are matches with the records in the general ledger. The source of information that helps tally the figures to prove its justified, are general ledger and receivables details.

Reconciliation may bring to notice the difference or discrepancy between the two, which could arise due to various reasons, which may include:

- Missing information in the general ledger

- Misplacement of receivables details to some other account

- Date issues or discrepancy

Reconciliation is carried out at the end of the months before the financial statements are issued to avoid further errors. The rectifications are done as soon as the reconciliation identifies discrepancies. Once the financial data is rectified, financial statements can be accordingly prepared and issued.

Analysis and Interpretation

The liquidity analysis and interpretation for the level of trade receivables should always be looked into in the specific industry context. Certain industries operate in an environment with a high level of receivables. A typical example is electricity generation companies operating in India, where receivables are very high and days receivable for generation companies vary between as low as one month to as high as nine (9) months.

On the other side, some companies operate with virtually very few or no trade receivables. For example, companies operating and toll road project developers and operators have fewer accounts receivables as their revenue is toll collection from commuters on the road. They collect the toll from commuters as and when they pass by toll plaza.

So for a meaningful analysis, one should look at the receivables levels of the top 4-5 companies in the respective industry. For example, suppose your target company has higher receivables in comparison. In that case, it is doing something wrong either in the business model or client/customer targeting or incentives in terms of credit sales to promote sales.

To conclude, one can safely assume that the lower the receivables level and days receivables, the better the liquidity position for the company.

Difference Between Trade Receivables and Trade Payables

When it comes to trade deals between businesses and clients, there are two terms that are widely used – trade receivables and trade payables. These are used interchangeably for accounts receivables and accounts payables, respectively.

Let us have a quick look at the difference between the two:

- Trade payables is the amount that firms owe to suppliers in exchange for the goods and services taken up from them, while payables is the amount that customers owe to the firms in exchange for the goods and products that the former buys on credit.

- While trade receivables is a current asset, trade payables is recorded as a current liability in the balance sheet.

Recommended Articles

This has been a guide to Trade Receivables and its Meaning. Here, we explain it along with its reconciliation, examples, formula, vs trade payables. You can learn more about accounting from the following articles –