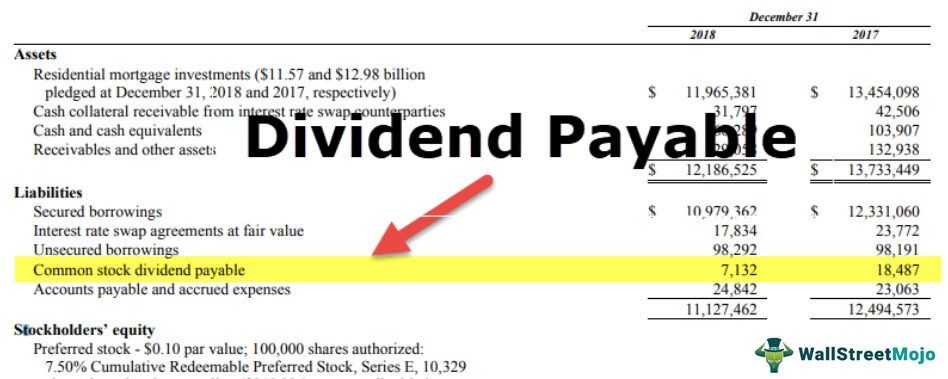

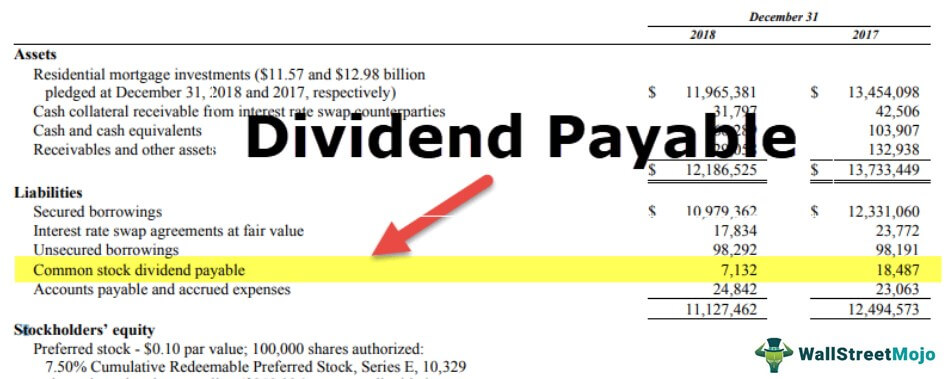

Dividend Payable Definition

Dividend payable is that portion of accumulated profits declared to be paid as dividends by the company’s board of directors. Until such a dividend is declared and paid to the concerned shareholder, the amount is recorded as a dividend payable in the current liability on the company’s balance sheet. After such declaration, it is due to be paid to its shareholders.

Simply put, a dividend payable is the dividend approved by the shareholders in the annual general meeting. The company needs to pay it within the specified statutory due days. The calculation methods are different for different shares and based on their preferences.

- Dividend payable is the portion of the accumulated profits declared as the company’s dividends to be paid by the company’s board of directors.

- Until the dividend is declared and paid to the shareholder, the amount is noted as a dividend payable in the current liability on the company’s balance sheet. After the announcement, it becomes due that must be paid to its shareholders.

- It must be paid within the specified statutory due days.

- It must be paid under the set guidelines by the concerned nation’s chief organization considering the stock market. Once declared, the dividend disclosure may occur under the current liability until it is paid.

Dividend Payable Examples

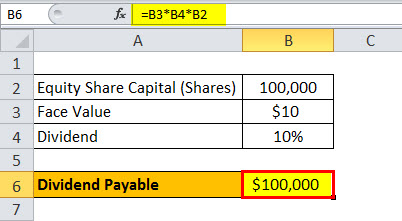

Example #1

ABC Ltd. has an equity share capital of $1 million, consisting of 1 lakh shares with a face value of $10 each.

The company proposed a 10% dividend at the end of the year. Calculate the dividend payable.

Solution:

= $10 * 10% * 100,000 shares

= $100,000

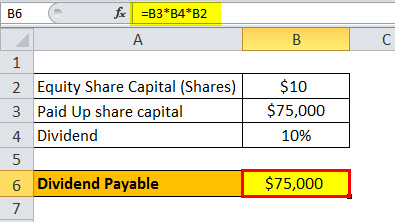

Example #2

Equity share capital = $1000,000 , consisting 1 lakh shares of $10 each.

Paid Up share capital = $750,000, consisting 75000 shares of $10 each.

Dividend Declared = 10%. Calculate dividend payable by the company.

Solution:

= 75000 shares * 10 % * $10 = $75,000.

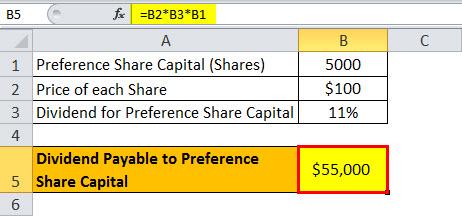

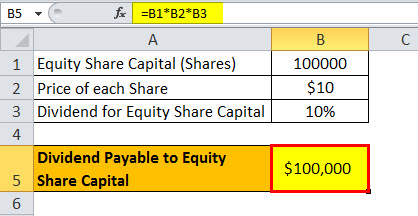

Example #3

For ABC Limited, below are the particulars:

Equity Share capital = $1000,000 consisting of 100,000 shares of $10 each.

11% preference share capital of $500,000, consisting of 5000 shares of $100 each.

The company declared a 10% dividend for the equity shares.

Please calculate dividend payables.

Solution :

Calculation of Dividend Payable to Preference share capital

= 5000 shares * $100 * 11%

=$55000

Calculation of Dividend Payable to Equity Share Capital

= 100000 shares * $10 * 10%

= $100,000

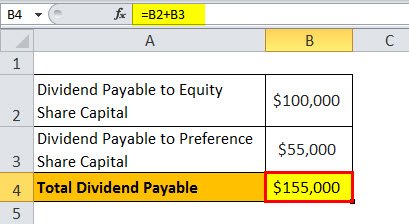

Thus total dividend payable by the company = $55,000 + $100,000 = $155,00

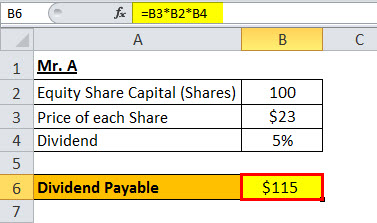

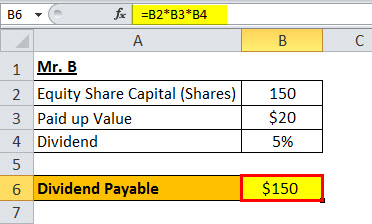

Example #4

Mr. A and Mr. B are subscribers to the equity share capital of Facebook, Inc. Mr. A has subscribed to 100 shares for $50 each and paid $23 for each share. Mr. B has subscribed for 150 shares of $50 each, paid $20, and called not paid $3 each. At the end of the year, the company declared a dividend of 5%. Please calculate the dividend payable to Mr. A and Mr. B.

Solution:

The calculation for Mr. A

Thus, dividend payable on the 100 shares = $23 * 100 shares * 5%

= $ 115

Mr. B has subscribed for 150 shares and paid the same value of $23, but he has paid only $23. Therefore, he will not pay the dividend on the calls not paid by the shareholders.

The calculation for Mr. B

= 150 shares * $20 * 5%

= $150

Thus dividend payable= $115 + $150 = $265

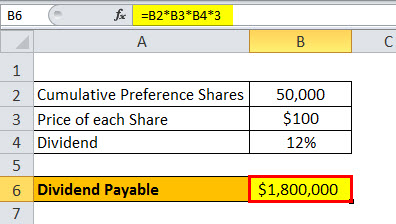

Example #5

ABC Limited has 12% cumulative preference shares of $5 million, consisting of 50,000 shares of $100 each. The company had not declared a dividend for the last two years. However, the company had declared a 12% dividend for the equity shares this year. Please calculate the dividend payable to the preferred shareholders this year.

Solution:

Cumulative preference shareholders can accumulate the dividend yearly, even though the company has not declared the dividend. As a result, they will receive a dividend for the past years for which the dividend was undeclared in the year of declaration.

Thus, in the given question, the company had not declared a dividend for the last two years and declared dividends this year. Therefore, preference shareholders will receive a dividend of 3 years.

Calculation of Dividend Payable

= 50000 shares * $100 * 12% * 3 years = $18,00,000

Thus, ABC Limited will have to pay the dividend of $18,00,000 this year, including an accumulated dividend of the last two years.

Example #6

Mr. A and Mr. B are subscribers to the equity share capital of HSBC Bank. Mr. A has subscribed to 250 shares of $20 each and paid $13 for each share consisting of $3 calls in advance. Mr. B has subscribed for 500 shares of $20 each, paid $8, and called not paid $2 each. At the end of the year, the company declared a dividend of 5%. Calculate the dividend payable to Mr. A and Mr. B.

Solution:

The calculation for Mr. A

Mr. A has subscribed to 250 shares by paying $13 for each share. However, Mr. A paid $3 in advance.

Dividend always gets paid on the Paid-up capital as and when called by the company. It cannot get paid on any advance calls received by the company.

Thus, Mr. A will not be eligible for the call in the advance dividend received by him, dividend payable to Mr. A = 250 shares * $10 * 5% = $125

The calculation for Mr. B

Mr has subscribed for 500 shares by paying $8 per share. However, Mr. B has not paid $2 on the paid-up value of $10. he will not pay the dividend on the calls in arrears. Hence, Mr. B will not receive a dividend on call in arrears of $2.

Dividend payable to Mr B = 500 shares * $8 * 5%

= $200

Thus total Dividend payable = $125 + $200 = $325

Conclusion

Dividend payable must pay obligation on the company, within the specified period and through the authorized banking partners. Moreover, it must be paid under the guidelines the concerned nation’s chief organization sets, keeping watch on the stock market. Once declared, disclosure of the dividend will take place under the current liability until paid.

Frequently Asked Questions (FAQs)

Is dividend payable a current liability?

Yes, the dividend payable is a current liability. It is recorded as a current liability on the balance sheet because it shows declared payments to shareholders typically met in a year.

Is dividend payable an expense?

Dividends payable to shareholders are not considered an expense on a company’s income statement. It is because cash dividends do not affect a company’s net income or profit. Instead, dividends affect the shareholders’ balance sheet equity section.

Is dividends payable a debit or credit?

When a dividend to shareholders is officially declared, the company’s retained earnings account gets debited for the dividend amount. The dividends payable account gets credited by a similar payable amount.

What account is dividend payable?

Dividend payable is a current liability account on the balance sheet. It is displayed as declared payments to shareholders that have been announced by the Board of Directors but are yet to be distributed to the concerned stockholders.

Recommended Articles

This article has been a Guide to Dividend Payable and its definition. Here, we discussed calculating dividends payable and practical examples and explanations. You may learn more about accounting from the following articles –