What is a Collateralized Debt Obligation?

Collateralized debt obligation (CDO) is a Structured product used by banks to unburden themselves of risk, and this is done by pooling all debt assets (including loans, corporate bonds, and mortgages) to form an investable instrument (slices/trances) which are then sold to investors ready to assume the underlying risk.

The rise and demise Collateralized Debt Obligation assets turned out to be a cyclical process, initially reaching the top because of its inherent benefits, but ultimately collapsing and leading to one of the largest financial crises. CDOs are considered highly astute financial instruments that created cheap credit market infused liquidity, and freed up capital for lenders but ultimately collapsed because of a lack of comprehensive understanding of the systemic risk it may cause.

Key Takeaways

- A Collateralized Debt Obligation (CDO) is a structured financial product that combines various debt instruments, such as bonds, loans, and credit assets.

- CDOs provide investors with a diversified portfolio of debt instruments across different risk levels. Tranches are structured to prioritize repayment, allowing investors to choose risk and return levels that suit their preferences.

- CDOs often employ credit enhancement mechanisms, such as over-collateralization or credit default swaps, to improve the credit quality of lower-rated tranches.

How does Collateralized Debt Obligation (CDO) Work?

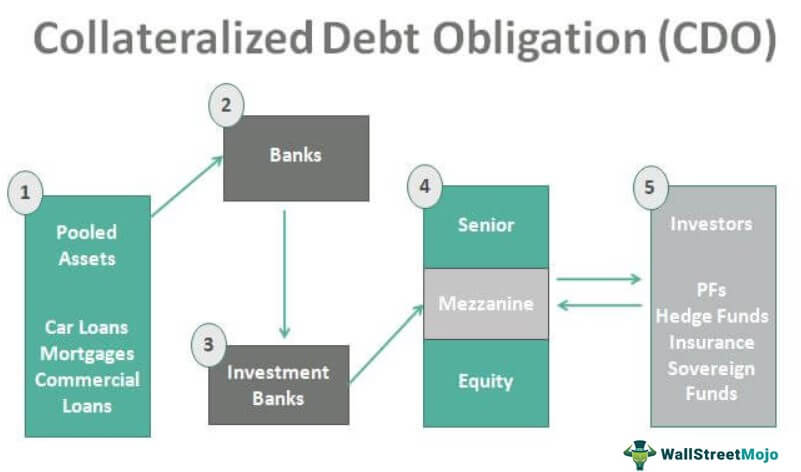

Synthetic Collateralized Debt Obligations or the general CDO creation can be understood as a 5-step process:

Step #1 – Pooled Assets

Banks prepare a list of all the pooled assets (secured and unsecured) like car loans, mortgage loans, commercial loans, etc. that can be included a part of CDOs

Step #2 – Banks form a diversified portfolio

Once the list of pooled assets is prepared, than the Bank started with an aggregation of various debt assets, such as Loans issued corporates and individuals, Corporate bonds invested in, Mortgages, and other debt instruments like credit card receivables.

Step #3 – Investment Banks

A Bank may rope in an investment bank to sell this diversified portfolio

Step #4 – Formation of Tranches

The cash inflows from the portfolio created are sliced into the number of investable tranches. These tranches are characterized by a degree of riskiness. The tranches created are classified as:

- “super senior,” the safest and first one to receive the payouts. But, have the lowest interest rate

- “mezzanine financing,” moderate risk, and a bit higher interest rate

- “equity”/ ”toxic waste,” junior tranche, most risky and offers the highest interest rate. The payouts are made after all payouts are made for super senior and mezzanine tranches.

Step #5 – Selling of Tranches to Investors.

Depending on the risk appetite of various investor groups, these tranches are offered. The most senior tranche is often sold to institutions looking for highly-rated instruments, such as pension funds. The lowest rated tranches are often retained by the CDO (Collateralized Debt Obligations) issuers. This gives the bank an incentive to monitor the loan.

Mezzanine tranches are often bought by other banks and financial institutions.

This entire process of aggregation of assets and slicing them and selling it off to appropriate investors is known as securitization. The bank or the institution assuming the role of CDO issuer is known as Originating Institution. And this entire model is known as the originate-to-distribute model.

Examples

Now that we understand the basics and intricacies of the concept, let us understand the practicality of synthetic collateralized debt obligations and general CDOs through the examples below.

Example #1

Michael, an investor with a high risk appetite. He is eyeing an investment opportunity and comes across a CDO. It is a mixed bag of debt securities like mortgages, bonds, and the likes. Michael perceives potential in the real estate market and decides to invest in a CDO filled with mortgage-backed securities.

By purchasing a tranche of this CDO, Michael essentially owns a slice of the bundled mortgages. The risk and return associated with his investment are based on the performance of these underlying mortgages. If homeowners make timely payments, Michael stands to gain returns. However, if economic winds shift unfavorably, leading to mortgage defaults, Michael could face losses.

Example #2

In 2020, JP Morgan, Nomura, and BNP Paribas were in a race to re-launch the first managed synthetic collateralized debt obligation (CDO) since the 2008 financial crisis. This initiative marked a significant milestone in the rehabilitation of this controversial category of structured credit investment, often linked to the excessive financial engineering that precipitated the 2008 crisis.

The credit default swap (CDS) market, a key component in CDOs, experienced a staggering fourfold expansion in just two years, reaching its peak at US $58 trillion in 2007, as reported by the Bank for International Settlements. However, it subsequently contracted, shrinking to US $8 trillion by mid-2019.

Important Terms and Differentiation from Similar Products

CDOs are part of a large set of financial instruments that sound and operate similarly. However, there are differences in their fundamentals and implications. Let us understand their distinctions in comparison to similar products in the market through the discussion below.

#1 – CDOs and CMOs

Collateralized Mortgage Obligation, as the name suggests, is a structured product that pools in mortgage loans and slice them into tranches of different risk profiles, as explained in the previous section. CDOs, on the other hand, can have loans (home/student/auto, etc.), corporate bonds, mortgages, and credit card receivables, thereby expanding the choice of instruments for forming the portfolio.

- CMOs are issued by REMICs (Real Estate Mortgage Investment Conduit). CDOs are issued by SPEs (Special purpose entities) created by banks which are separately capitalized to assume a high Credit rating for issuing CDOs.

- CMOs may have different classes of securities depending on the quantum of risk associated with the mortgages and are created by breaking down coupons and principal payment. CDOs, on the other hand, have tranches created by slicing down the groups of cash flows from various instruments. And there have to be at least three classifications.

#2 – CDOs and MBS

MBS or the Mortgage-backed securities are the earliest form of structured products, formally introduced in the early 80s. Structurally MBS and CDOs are similar to CDO being more complex. MBS have repackaging of mortgages into investable instruments. Based on the type of mortgage repackaged, MBS are of majorly two types: RMBS (Residential MBS) and CMBS (Commercial MBS)

#3 – CDOs and ABS

ABS or the Asset-backed Security, is similar to MBS, with the only difference that the pool of assets comprises of all debt assets other than Mortgages. CDO is a type of ABS which includes mortgages as well in the pool of assets.

#4 – CLOs and CBOs

CLOs and CBOs are subclassifications of CDO. CLOs are collateralized loan obligations that are made using bank loans. CBOs are a collateral bond obligation which is made using corporate bonds.

There are lesser-known CDO classifications as well, Structured finance back CDOs having ABS/RMBS/CMBS as underlying and Cash CDOs with cash market debt instruments.

CDOs and Subprime Mortgage Crisis 2008

The financial crisis of 2007 and 2008, often called the subprime crisis, had several factors, ultimately leading to a collateral failure of financial systems. Among various causes, CDOs played an important role. The crisis started with a housing bubble1, which majorly proliferated because of the availability of cheap credit and widespread use of the Originate-to-distribute model, burst around 2006 and 2007, and led to a liquidity squeeze.

The originate-to-distribute model and securitization, i.e., use of CDOs/ CMOs, etc. became popular for the following reasons:

- A low-interest rate on mortgages: Originating institutions were in a position to issue mortgages at a low-interest rate by slicing it off and spreading the risk among willing investors

- A high rating of CDOs helped banks to meet lower capital charge requirements of Basel I and II without affecting the risk profile.

Commercial papers were issued, and short term repurchase agreements (both of which are ideally short-term instruments) were done to fund the investments in structured products. The months of July and August 2007 were specifically important as most of the commercial papers were maturing in this period. Banks tried Repos and issuance of Commercial papers to meet the liquidity requirements at redemptions, but the impact was so widespread as all major banks were facing the same problem, that the dollar lending rates rose as high as 6/7 %.

Faced with huge losses, banks and financial institutions with heavy investments in structured products were forced to liquidate their assets at very low prices. This further led to bankruptcies filed by prominent banks like Lehman Brothers and American Home Mortgage Investment Corp. etc., and leading to intervention and financial restructuring by the International Monetary Fund in October 2009.

Collateralized Debt Obligations Vs Mortgage-Backed Securities

We saw the differences between collateralized debt obligation assets and mortgage-backed securities in one of the sections above. However, let us understand the differences between the two concepts in detail through the comparison below.

CDOs

- CDOs are complex financial instruments that bundle various debt securities, such as mortgages, bonds, and loans, into a single package.

- They comprise diverse assets and are typically divided into tranches with varying risk and return profiles.

- Investors in CDOs are exposed to the performance of the underlying assets, and returns are contingent on the success or failure of the bundled securities.

- CDOs include various debt instruments like loans, corporate bonds, and mortgages.

- They expose investors to a broader spectrum of risks, given their diverse asset pool.

Mortgage-Backed Securities

- MBS are financial products backed by a pool of mortgages, where the cash flow from the underlying mortgages is used to pay investors.

- MBS are specifically tied to mortgages, representing an ownership interest in a pool of loans.

- Investors in MBS bear the risk associated with mortgage payments, prepayments, and potential defaults within the underlying mortgage pool.

- They are solely tied to mortgages.

- MBS focuses on the risks inherent in the mortgage repayment scheme of things.

Frequently Asked Questions (FAQs)

Who invented CDOs?

CDOs were developed in the 1980s by several financial institutions, including Drexel Burnham Lambert and Salomon Brothers. While there were multiple contributors to the creation and evolution of CDOs, they are often associated with the pioneering work of Michael Milken and Lewis Ranieri, who played significant roles in their development and popularization.

What is the difference between CDS and CDO?

Their purpose indicates the main difference between a CDS (Credit Default Swap) and a CDO (Collateralized Debt Obligation). A CDS is a derivative that provides insurance against default on a specific debt instrument. At the same time, a CDO is a structured product that combines multiple debt instruments to create new securities with varying levels of risk and return.

What is a CDO called today?

A CDO is commonly referred to today as a Collateralized Debt Obligation. The term “CDO” has remained consistent over time and continues to be used to describe this structured financial product that pools various debt instruments.

Recommended Articles

This has been a Guide to what is a Collateralized Debt Obligations. Here, we explain its examples and how CDOs led to the Subprime Mortgage Crisis in 2008. You can learn more about financing from the following articles –