Part of our Structured Finance guide

What Are Collateralized Mortgage Obligations?

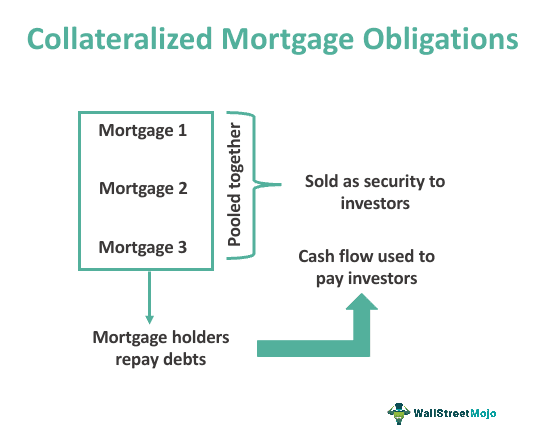

Collateralized Mortgage Obligation (CMO) is a type of mortgage-backed investment wherein a number of mortgages are pooled together and sold as investment securities. Cash inflow occurs when the borrowers repay their loans which are then paid out to the CMO investors.

CMOS are complex financial structures that are governed by the different terms associated with the mortgages in the pool. As such, it isn’t very easy to assess the risks and returns associated. Sometimes investors get so blinded by the income that is supposed to come that they forget to assess the quality of the underlying.

Key Takeaways

- Collateralized Mortgage Obligations (CMOs) are structured mortgage-backed securities created by pooling individual mortgage loans and dividing them into different tranches with varying risk and return profiles.

- CMOs are structured with multiple tranches, each having a specific priority of cash flow distribution and risk exposure. They offer options for risk tolerance and desired return levels to different investors.

- CMOs distribute cash flows to tranches based on pre-defined rules, prioritizing repayment of principal and interest to certain tranches before others. Cash flow allocation can be sequential, pro-rata, or based on other predefined structures.

Collateralized Mortgage Obligations Explained

Collateralized Mortgage Obligation is divided into various risk categories known as tranches. These multiple classes are meant for investors with different risk appetites and return expectations. They have different maturity dates and are ranked according to the priority of payments i.e., and some tranches are paid off before others. As a result, each tranche behaves as separate security with different outstanding principal and coupons.

The riskiest tranche will be the first one to bear the brunt of losses arising from default and, in turn, will be rewarded by the highest coupon rate among all. In the event of prepayments, the least risky class receives its share first and will have the lowest rates of return. Structuring the CMOS like this doesn’t eliminate or lower risk. Instead, the risk gets distributed among investors as per their risk profiles.

However, it is always a great idea to do proper research and analysis before deciding to buy collateralized mortgage obligations and making investments in them, because ignorance can lead to huge losses in this market.

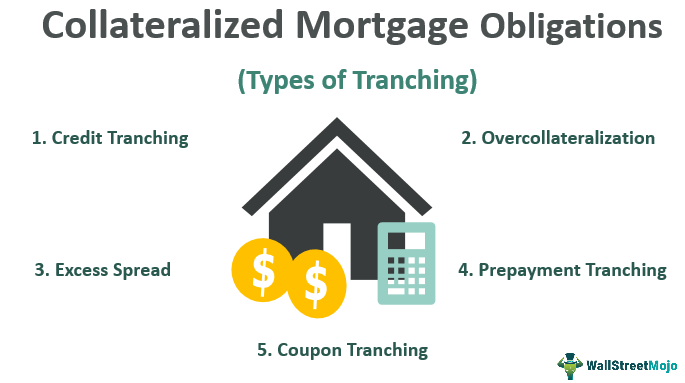

Types Of Tranching

Now let us look at the different types of tranching in CMOs.

#1 – Credit Tranching

This is the most prevalent form of branching, aiming towards credit protection. The structure consists of senior and junior tranches. Junior tranches absorb any losses resulting from the default of borrowers before it can be passed on to the senior tranches. Whatever cash flow is available is first made available to the senior tranches. This kind of structure is also referred to as the “waterfall structure.” Generally, a threshold trigger is also defined where after a certain level of delinquency, the losses start getting transferred to the senior tranches as well.

#2 – Overcollateralization

This refers to a situation of credit enhancement where the principal value of CMOs issued is far less than the total value of underlying mortgages. This renders the CMOS over collateralized where it does not experience losses until the value of mortgages falls below the principal of CMOs, leading to under collateralization. This condition is common in the case of subprime loans.

#3 – Excess spread

The term excess spread refers to the difference between the coupon rate of the issued CMOs and the weighted average interest rate of all the mortgages in the pool. Maintaining excess spread provides a cushion for any losses that might occur in the future. This margin is stored in a spread account and is used to maintain timely payments in case of default and non-payment.

#4 – Prepayment Tranching

Prepayment tranching is a mode of providing a level of protection against prepayment risk. Prepayment of mortgages in the pool shortens the life span of CMOs as the principal is paid before maturity and any future interest payments disappear. Prepayment tranches re-allocates the prepayment risk over a number of tranches. This can be approached in a number of ways:

- Time Tranching – All the principal payments available at one time are used to pay off the first tranche. Any next prepayments go to the next tranche in the sequence. This way, different tranches mature at different times.

- Parallel Tranching – This occurs when the coupon rates of all tranches eventually equal the interest rates of the mortgages in the pool. The tranches may have fixed or floating rates, but it all comes down to match the mortgage rates.

- Z Bonds/ Accrual Bonds – This refers to a CMO which has a “Z” tranche. This tranche is often the last tranche and does not receive any interest payments at first. All the interest accruing for this tranche goes to pay off the principal of other tranches. After other tranches are paid off, this tranche starts receiving its due payments.

- Schedule Bonds and Companion Bonds – Schedule bonds receive prepayments as per a pre-defined schedule, and any excess is absorbed by the support bonds, also known as companion bonds.

#5 – Coupon Tranching

This type of traching is approached by re-allocating the coupons of the mortgages and is mostly done after prepayment teaching is achieved. Coupon tranching produces two main types of tranches:

- Interest-only tranche (IO) – This tranche only receives the interest calculated over a notional principal. No principal payments are made. Hence, it does not face any prepayment risk.

- Principal only tranche (PO) – This tranche is only set to receive the principal payment and no interest, and hence it becomes more vulnerable to prepayments.

Financial Crisis Of 2008

The Subprime Mortgage Crisis was a result of lack of knowledge about the risk and return capacity of the mortgage loans that backed it.

It was a financial event that had far reaching effects on the global financial market. In mid-2000, there was a boom in the US housing market, due to very low interest rate and relaxed rules of lending. Thus, borrowers with very low credit rating began to take loans to buy houses. They were identified as subprime loans.

But mortgage lenders pooled those loans and sold them as securities to investors globally. But as the subprime borrowers began to default because of declining housing market, the institution who issued the loans faced losses. The crisis escalated and affected the global market, leading to job loss, fall in GDP and consumer spending, etc.

This led to increased monitoring by the regulatory bodies. CMOs are good investment options, but like everything else, they need to be assessed for any possible risks and losses before investment decisions are taken. The above is a perfect collateralized mortgage obligations example to explain the risk associated with them.

Example

Let us assume that a financial institution has created a CMO backed by residential mortgage loans with an amount of $100 million. It is divided into different tranches. Class A consists of least risky loans with a balance of $60 million, at interest of 3%. Class B is a mezzanine tranch with moderate risk, with balance $30 million, interest 5% and Class C is the subordinate tranch with highest risk, balance $10 million, interest 6%.

From the above example, the structure of the CMOs is clarified.

Advantages

Some of the advantages of CMOs are detailed below. Let us try to understand them before we buy collateralized mortgage obligations.

- Tranching allows investors to earn profits more suited to their risk profiles and investment return expectations.

- CMOs benefit the financial institutions by allowing them to issue securities that are structured in a way where they do not have to worry about making payments to all investors at once. Some receive payments before the others and those who don’t have signed up for it.

- Investors have access to a varied set of mortgage loans under one roof.

Disadvantages

Some of the disadvantages of this concept are as follows:

- Prepayment risk- Investors have access to a varied set of mortgage loans under one roof.

- Interest rate risk- Prepayments are most common when market interest rates fall since the homeowners look for refinancing options to reduce their borrowing costs.

- Market risk- Overall economic condition also impacts the functioning of a CMO.

- Liquidity risk- Mortgage loans aren’t liquid. If an investor looks to get out of one position, it isn’t very easy.

- The performance of a CMO is largely dependent on the quality of underlying loans. If the underlying mortgages are subprime, the probability of default is much greater.

Collateralized Mortgage Obligations Vs Mortgage Backed Securities

Both the above are two types of structured securities that are backed by loans. But the basic differences between them are as follows:

- The CMOs are a type of mortgage backed securities which are divided into classes as per the risk but the latter is an ownership interest in the pool of mortgage loans.

- The former is divided into various tranches or classes that vary according to the risk and return profiles, but the latter are loans bundled into pools which are issued as securities.

- In case of the former, the cash flow from the loans are allocated among the tranches but in case of the latter pro-rata shares are allocated to the investors.

- For the former, the risk and return vary as per the tranches but for the latter, the risk directly depends on the payment of loan by the borrowers.

- The CMOs employ different credit enhancement facilities, suh as reserve funds or overcollateralization, but for the mortgage backed securities, there is the risk of default form the borrowers. The creditworthiness in this case is very important.

The CMOs are not actively traded in the market but the latter is done so.

Frequently Asked Questions (FAQs)

How do Collateralized Mortgage Obligations (CMOs) differ from other mortgage-backed securities?

Collateralized Mortgage Obligations (CMOs)differentiate themselves from other mortgage-backed securities through their tranche structure. Unlike pass-through securities and similar alternatives, CMOs divide cash flows and risks into multiple tranches. This hierarchical structure allows investors to select the risk and return profile that aligns with their investment objectives.

What are the risks associated with investing in CMOs?

Investing in CMOs entails several risks, including prepayment, interest rate, credit, and liquidity risks. Prepayment risk arises when mortgage borrowers repay their loans early, impacting the cash flow distribution among CMO tranches.

Who typically invests in CMOs?

CMOs are primarily acquired by institutional investors, such as pension funds, insurance companies, hedge funds, and other large investment firms. Nevertheless, individual investors can also access CMOs through mutual funds or exchange-traded funds (ETFs) that invest in mortgage-backed securities.

Recommended Articles

This has been a guide to Collateralized Mortgage Obligations. Here we discuss types of training in Collateralized Mortgage Obligations along with advantages and disadvantages. You can learn more about financing from the following articles –