What Is Asset-Backed Commercial Paper (ABCP)?

Asset-backed commercial papers, or ABCP, are short-term financial securities backed by assets, issued for 90 to 270 days. Hence, if the underlying assets fail to generate sufficient cash flow, there is a risk of default on the ABCP. The primary purpose of ABCP is to fulfill the company’s capital requirement (or other borrowers).

These ABCPs intend to fill the debt gap of short-term money rules. Usually, the cycle for these money market vehicles remains between three to 9 months. Likewise, the payback period also stands at less than 30 days. However, asset-backed commercial paper issuers might not adhere to the standards leading to higher risk.

Key Takeaways

- Asset-backed commercial papers (or ABCPs) are commercial papers issued by large corporations for 90 to 270 days. These are short-term securities for collateralized assets.

- The concept’s origin dates back to the 1970s when GNMA ensured timely and guaranteed interest and principal payments to the respective investors.

- The structure of ABCP involves a single and multi-seller program. The large corporations then store assets in the conduit or special purpose vehicles (SPV) for security.

- The only difference between ABCP and commercial paper is that assets back the former, and the latter involve none.

Asset-Backed Commercial Paper Explained

Asset-backed commercial papers are money market securities issued by large companies for less than a year. The maturity date for the ABCP is 270 days at maximum. Plus, its issuance is either on an interest or discount basis. In addition, they are set up by sponsoring financial institutions.

Therefore, the process of ABCP is similar to the commercial paper. However, it involves some extra elements and procedures. Let us look at them:

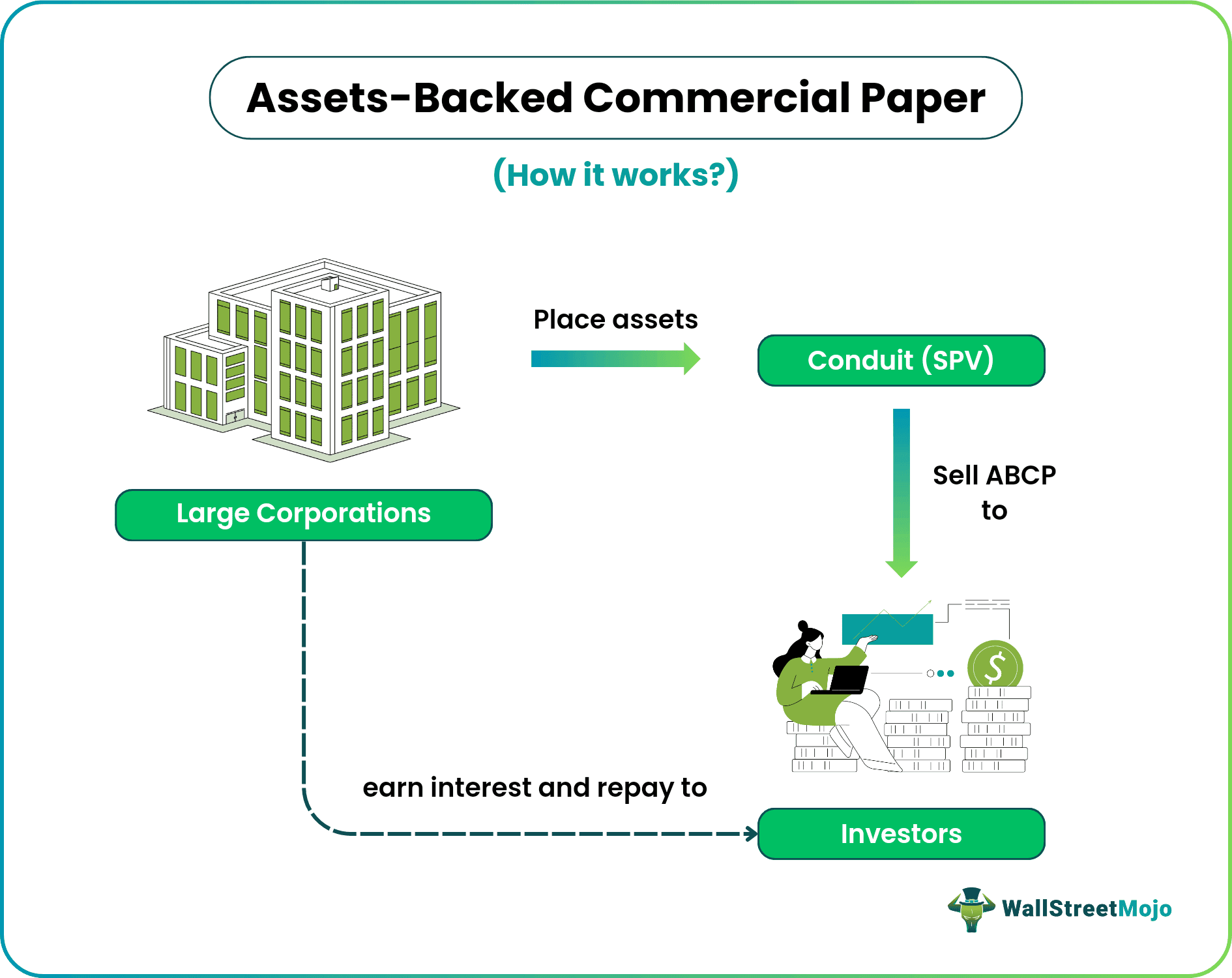

- Large corporations requiring debt will set up an SPV (Special Purpose Vehicle) and pool all their assets.

- These conduits will act as separate entities that handle these assets, protecting them from bankruptcy.

- The ABCP is then sold at face value to the investors in the secondary market. Placement agents provide SPV access to the investors. There are at least two such agents, mostly from investment banks.

- As the assets within the SPV gather cash flows, it is used to repay the investors. These cash flows occur in the form of interest and principal payments.

- However, if there is an insufficient amount to repay the investors, the SPV can sell the assets.

Usually, asset-backed commercial paper issuers give debt with lower credit risk. Hence, this risk is backed by collateral that includes the corporation’s assets. The firm needing the money will issue an ABCP and sell it in the secondary market. However, they must first set up an SPV. The issuers who provide this facility are conduit or special purpose vehicles (SPV). Thus, the primary purpose of SPV is to own the sellers’ assets. These assets could be notes like trade receivables with a short-term recovery period.

History

Let us look at the history from the rise to the asset-backed commercial paper in detail:

- The 1970s – Origin in 1970 when the Government National Mortgage Association (GNMA) ensured the investors regarding interest and principal payments by the federal government.

- The 1980s – The asset-backed commercial paper market rose from $50 billion to $70 billion.

- 1983 – The Standard & Poor’s Corporation first rated pooled receivables.

- 1985 – The Federal Home Loan Mortgage Corporation (FHLMC) and the Federal National Mortgage Association (FNMA) started issuing mortgages backed by assets.

- 2008 – The Great Recession and the stock market crash of 2007-2008 brought a downfall and caused the asset-backed commercial paper financial crisis.

Structure

The structure of asset-backed commercial paper issuers involves two sellers, namely a single seller and a multi-seller program. Let us look at them:

#1 – Single Seller Program

As per this structure, there is a single seller who then buys assets from just one person. Plus, there is only one collateral kept within the SPV. Thus, there is no diversification, plus it involves higher risk.

#2 – Multi-seller Program

Here, there are more sellers involved. Thus, there are various assets placed within the conduit. As a result, there is lower credit risk and higher liquidity.

Examples

Let us look at the examples of asset-backed commercial paper to comprehend the concept better:

Example #1

Suppose Killis Ltd. is a credit financing company that provides loans to businesses. They have, in total, $100 million worth of collateral from home loans. However, the firm wishes to earn interest on these assets. Therefore, they intend to place these assets in an SPV. Killis Ltd then issues ABCP to the respective investors.

The collateralized assets of home loans backed this short-term security. Throughout the period, they earn interest and principal payments on it. Later, the firm went into bankruptcy. Still, the firm was able to repay the investors.

In this case, the SPV acted as a separate entity. Thus, there was no default repayment available.

Example #2

For 2023, market analysts for the asset-backed commercial paper sector in the United States have a neutral outlook.

According to a recent update from Fitch Ratings, the ABCP sector would experience declining asset performance in 2023 due to its significant exposure to vehicle loans and leases, corporate and commercial loans, and trade receivables. However, due to the continuous credit quality, assigned scores on ABCP investments have endured.

According to Federal Reserve figures published on Monday, there was $1.1 trillion in outstanding asset-backed commercial paper. Due to a boom in issuance that started in August, unsettled commercial paper was up 9% for the year back in September.

Fitch analysts stated in the outlook that “volumes in ABCP were mostly unchanged in 2022, a pattern that we expect to continue in the near term.”

Hence, in 2023, ABCP is anticipated to benefit from transaction-savvy administrators and liquidity support, particularly given the expected softening of underlying assets.

Besides, Fitch anticipates choppy inflows during the first three months of the year, but that institution-quality money-market mutual funds may still see a 0.08% gain in total assets.

Advantages And Disadvantages

Advantages

- ABCPs provide extra liquidity and flexibility to the sellers.

- There is low credit risk involved in the market.

- The type of structure of ABCPs creates greater security for the participants involved.

- There is a diversification of assets under the program.

Disadvantages

- Nature, quality, and type of assets can influence the ABC

- The 2008 asset-backed commercial paper financial crisis brought a collapse.

- Assessing various assets can bring complexity to the SPV.

- Likewise, the risk from the cash flows may flow to the investors.

Asset-Backed Commercial Paper vs Commercial Paper

Although ABCP and commercial papers share much in common, they have distinct features. So, let us look at the differences between them:

Frequently Asked Questions (FAQs)

What is the difference between asset-backed commercial paper and unsecured commercial paper?

The only difference between ABCP and unsecured commercial paper is that the former involves collateralized assets. But, in the latter, there is no collateral or security provided.

What is the role of asset-backed commercial paper in the financial crisis?

The ABCP plays a significant role in the financial crisis. The SPV will protect the investors during bankruptcy if the proper structure is involved. Here’s an overview of its position and the impact it had during that period:

– Exposure to subprime mortgages

– Deterioration of Mortgage

– Liquidity Crunch

– Losses and write-downs

– Funding squeeze and Market freeze

– Contagion effect

How does ABCP conduit work?

The purpose of ABCP is to act like a sponsor. It intends to collect financial assets from various sellers and keep them with itself until maturity. Hence, these commercial paper conduits provide financial institutions with a mechanism to efficiently fund a portfolio of assets by converting them into short-term debt instruments.

Recommended Articles

This article has been a guide to what is Asset-Backed Commercial Paper. We explain it with its examples, comparison with commercial paper, structure, and advantages. You may also find some useful articles here –