Part of our Fiscal Policy guide

What is Fannie Mae?

Fannie Mae (Federal National Mortgage Association) is a securitization agency created by the US Government. Its primary purpose is to provide affordable financing. They serve the people who want to buy a house in America.

During the Great Depression, the US faced a severe housing crisis as banks did not have any capital left to lend. As a result, one out of every four house owners faced foreclosure and lost their dream of owning a house. Consequently, the US Congress formed The Federal National Mortgage Association (FNMA) in 1938. FNMA buys loans from banks and, in return, gives them more capital for lending.

- Fannie Mae (FNMA) purchases and assures the mortgage loans issued by commercial banks and other large lending institutions.

- It works under the Federal Housing Finance Agency’s (FHFA) conservatorship and is a government-sponsored enterprise (GSE).

- In 1938, Congress set up FNMA to handle the housing bust that occurred during the Great Depression. The fundamental motive of the association was to ensure that the banks didn’t run out of capital for financing new mortgages.

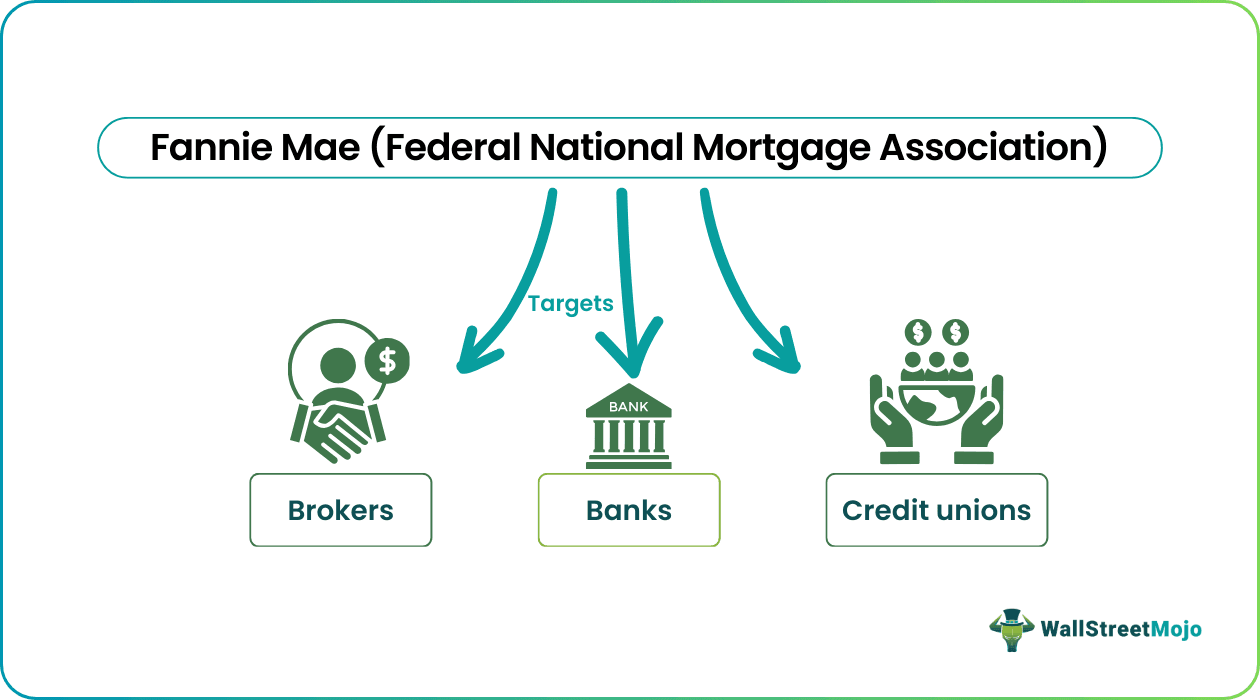

How Does Fannie Mae Work?

Fannie Mae is a support organization for mortgage brokers, banks, and credit unions; it is functional in the secondary mortgage market. The FNMA introduced a new, steady, and reliable type of mortgage, the fixed-rate long-term loan.

FNMA buys loans from banks and, in return, gives them more capital for lending. The FNMA then pools those loans based on their tenures and repackages them as (MBS) Mortgage-Backed Securities. MBS are then sold to large insurance firms, pension funds, and hedge funds after keeping some commission for itself. MBS is a type of mortgage-backed debt security where the value is derived from a pool of residential mortgages.

The FNMA got privatized in 1968. From 1970 onwards, it got permission to purchase conventional loans as well. The different credit products offered by FNMA are the HomeReady and the RefiNow. The FNMA stock trades over the OTC markets of the US. The association owns the underlying securities even after selling the mortgage-backed securities to the investors. The share of the monthly mortgage payment is also shared with the investors on a pro-rata basis.

History

Fannie Mae entirely reformed the US housing scenario from the early 1900s. Back then, owning a house seemed a big deal for Americans. However, during the Great Depression, the banks were out of money and could not provide loans. Also, many Americans with mortgage home loans were unable to pay off their monthly mortgage payments and became homeless due to regressive recovery by the banks.

In 1938, US Congress came up with the Federal National Mortgage Association. The FNMA was Franklin D. Roosevelt’s “New Deal” to rescue the nation. The idea was to aid banks in bouncing back by creating a suitable mortgage loan product. The fixed-rate long-term mortgage loan was its highlight. It was affordable, flexible, reliable, and stable. In contrast, pre-FNMA loans required borrowers to pay hefty down payments. Also, those loans were for a short period.

How Does Fannie Mae Make Money?

The Federal National Mortgage Association primarily maintains the stability and liquidity of the US housing market. The enterprise makes home loans accessible to low- and middle-income Americans. But making money is equally essential. Although they are not the direct lenders to the homeowners, they set the eligibility criteria for sanctioned mortgage loans. FNMA only buys loans from banks and other lending institutions if they fulfill those criteria.

The association converts its single-family and multi-family loan purchases into different mortgage-backed securities (investment products). Moreover, the organization assures impressive interests and the principal sum to the investors. FNMA receives guaranteed fees against its risky foundation—the mortgage loans. Between the investors and purchased loans, the FNMA keeps some commission for itself—its source of income.

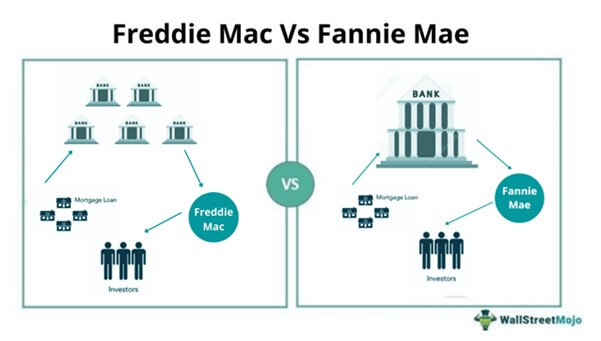

Difference Between Fannie Mae and Freddie Mac

Both the organizations are engaged in procuring mortgage loans. However, the significant difference between them is their target markets. Fannie Mae targets large commercial banks, whereas Freddie Mac targets smaller banks.

Both are aimed at low-income applicants and help reduce initial down-payment. FNMA provided HomeReady programs, whereas Freddie Mac provided HomePossible loans. HomePossible loans offered by Freddie Mac require a slightly higher credit score in comparison to Fannie Mae.

Effective July 28, 2019, qualifying income for Freddie Mac’s HomePossible loan is limited to 80% of Area Median Income. For Fannie Mae’s HomeReady qualifying income is up to 100% of Area Median Income. Area Median Income is the average income for a geographical area. Additionally, Freddie Mac can create 30-year mortgages, but FNMA cannot.

Frequently Asked Questions (FAQs)

What does Fannie Mae do?

The FNMA operates in the secondary mortgage market and buys loans provided by commercial or large banks. Thus, it enhances the banks’ cash flows by purchasing pre-existing mortgages. The banks then use the proceeds to loan them to other borrowers.

Does Fannie Mae own my loan?

Fannie Mae or Freddie Mac may own a mortgage loan taken by an individual. Customers can call or mail their respective service provider, i.e., the lending institution, to confirm whether the loan is bought by FNMA or Freddie Mac. Alternatively, customers can use Fannie Mae’s “Look-Up Tool” to verify it online.

Should I buy Fannie Mae stock?

Despite the positive movement, the FNMA stocks are not highly recommended. The housing market is expected to slow down in 2022 due to inflated mortgage rates and decreased supply.

Recommended Articles

This article has been a Guide to what is Fannie Mae and its Definition. Here we discuss Fannie Mae loans, mortgages, how it works, and how it differs from Freddie Mac. You may learn more about financing from the following articles –