Offset Mortgage Meaning

Offset mortgage can be defined as the type of the mortgage where the saving account of the person is linked with its mortgage thereby offsetting the balance between the accounts and this arrangement helps the person in reducing the interest payment because the rate of interest to be paid on the mortgage is substantially higher when compared to a rate of interest which is to be received on the savings account, thus providing a net benefit to the borrower.

Explanation

- If any person takes the mortgage from a financial institution and they have a savings account in the same financial institution then both can be linked. This type of mortgage is allowed in many of the nations depending on the tax laws of the respective country.

- This arrangement helps the borrower in saving its interest on the amount up to the extent available in his savings account. One of the key benefits is that the person still has access to savings, out of which he can spend the money whenever required.

Features Of Offset Mortgage

The features are as follows:

- This concept is different from the normal mortgage, as in the case of the offset mortgage, the savings account or current account is linked with the mortgage, and the savings balance maintained may offset balance.

- With this arrangement, the mortgage principal amount on which interest charge is payable by the borrower is reduced by balance available in the linked bank account.

- This concept is great for people having a moderate or large amount of deposits as it helps in saving their interest charge.

How Does it Work?

- Let the person link his mortgage to his savings. The financial institution offering such a mortgage offset the number of total balances that are available in the linked saving or current accounts of the person against the amount which it owes on the mortgage every month.

- After this offsetting, the interest is calculated on the lowered balance. This helps in reducing the net interest amount payable as the interest amount payable on the mortgage is substantially higher when compared rate of interest amount receivable on a savings account. Thus, till the time the accounts are linked, a person will not earn an interest in the savings or current account.

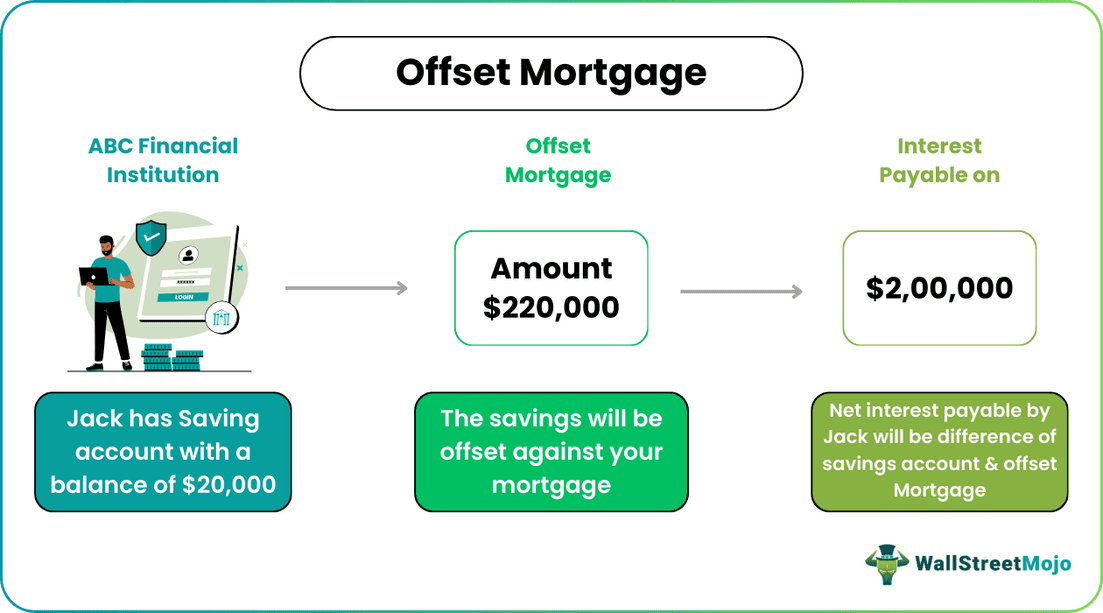

Examples of Offset Mortgage

For example, Jack has a saving account with the ABC financial institution with a balance of $20,000, out of which now withdrawals were made during the last month. The rate of interest on the savings account is 2% per annum. Also, Jack has an offset mortgage with a principal amount of $220,000 and an interest rate of 5% per annum.

In this case, the net interest payable by Jack will be calculated on the amount derived by deducting the saving balance from the mortgage balance.

- Interest payable = ($220,000 – $20,000) * 5%

- Interest payable = $200,000 * 5%

- Interest payable = $2,19,000

Rates

These interest rates are generally higher than of the traditional mortgage interest rates. Like in the case of the standard mortgage, in case of the offset mortgage as well both fixed and the standard variable rates are available where in case of the former rate of interest is fixed while in case of the later rate of interest changes.

Offset Mortgages Are Tax-Efficient?

Savings account interest is taxable if the interest earned is more than a certain amount, but in case of an offset mortgage, the money which is offset with a mortgage loan is not taxed, so it is more tax-efficient than a normal savings account. It is most beneficial for higher taxpayers as their savings account will attract no interest, and they do not have to declare the interest income as taxable income. In offset mortgage, one can link saving accounts of their family also so tax benefit will arise to the person(s) whose account(s) are linked.

Importance and Uses

- Saving of Interest on Mortgage: This type of mortgage is used to set off the liability of loan with the amount in a savings bank account and that savings bank accounts amount would be first set off against the principal of the loan, and interest will be calculated on balance amount hence it gives the benefit of tax saving of interest on saving account and benefit of interest on the mortgage loan.

- Allow to Withdraw and Deposit Money from Saving Account: Here, the saving account balance is used to offset the loan, and at important benefit is saving account is not blocked for deposits and withdrawals so the borrower can withdraw or deposit the amount to the savings bank account.

- Aids in faster repayment of the mortgage loan.

- It can be used for repayment of any type of loan.

- These accounts can be suitable for every type of taxpayers.

- With offset accounts, loan balance reduces more rapidly.

Advantages

- Saving in Tax: With offset mortgage accounts, tax expense can be reduced as there is no interest on saving account and ultimately, a tax on interest on saving account can be saved.

- Quick Repayment of Loan: As the mortgage account links the savings account with a loan account, it offset the balance in the saving account with the loan account and that amount in the savings account first to be used for setoff principal; hence loan can be repaid quickly.

- Benefited for Large Taxpayers: This account is very useful for large taxpayers as it gives the tax benefit of interest on saving bank account.

- No Restrictions on Saving Bank Account: They do not block the savings account. It allows the borrowers to deposit or withdraw from savings account along with using for offsetting the loan.

Disadvantages

- Higher Cost: in offset accounts rate of interest and charges of a bank are higher as compared to normal loan accounts.

- Loss of Interest Income: as the offset account is used to set off the amount in saving account with the mortgage account, resulting in no interest to be earned on excess money; hence there is a loss of income in the short run.

- Monthly repayments and interest rates can be increased if withdrawn from an offset savings account.

- Not all lenders provide benefits from such an account; hence the choice is limited, and this gives more benefit to the lenders who offer the benefit of offset, and they can set the terms and conditions favorable to them.

Conclusion

An offset mortgage is used for offsetting the balance in the loan account with the amount in saving bank; hence loan can be repaid quickly, but at the same time lenders charges higher interest rates as not all lenders provide the benefit of offset. It is useful for large taxpayers, and it gives tax benefit of tax on interest on saving accounts.

Recommended Articles

This has been a guide to offset mortgage and its meaning. Here we discuss features, examples, and how does offset mortgage works along with advantages and disadvantages. You may learn more about financing from the following articles –