Static Scoring Definition

Static Scoring or Conventional Scoring refers to a government revenue estimation method based on the assumption that taxpayer behavior does not change with changes in taxation or other policies. It further states that these changes have no impact on macroeconomic parameters like Gross Domestic Product (GDP), inflation, and interest rates, among other things.

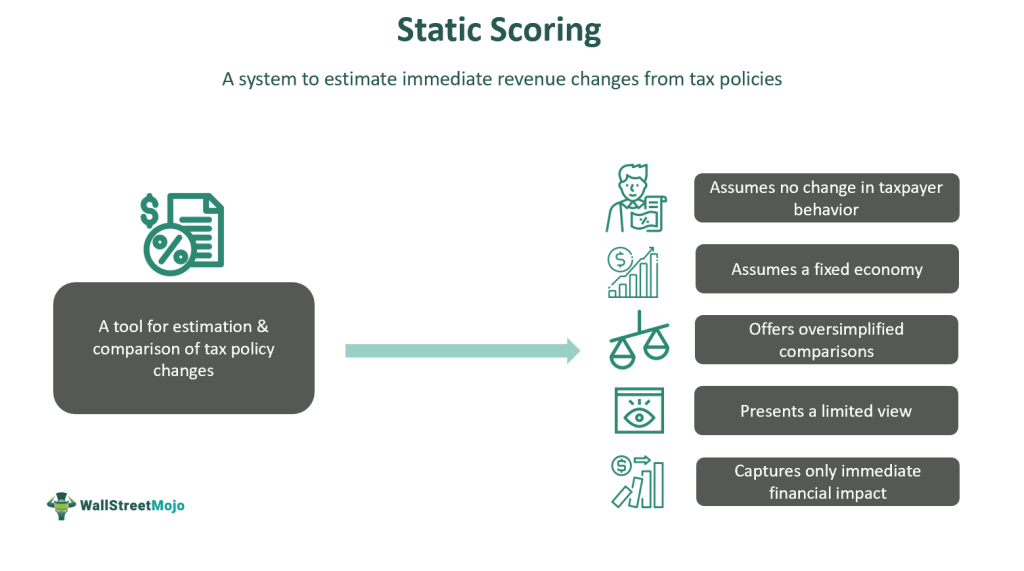

It considers the direct results of policy changes without taking consumer behavior or other effects on the economy into account. It offers a single-dimensional perspective on tax changes and measures revenue changes, presuming constant Gross Domestic Product (GDP). It assumes that the behavior of firms and individuals remains unaffected by policy changes.

- Static Scoring is a revenue estimation method that works on the primary assumption that taxation/policy changes do not bring about any behavioral or macroeconomic changes in an economy.

- It calculates revenue changes assuming that the country’s Gross Domestic Product (GDP) is stable, not reflecting upon the influence of taxes on consumer behavior.

- While it assumes policy and tax changes do not influence taxpayer behavior and other macroeconomic factors, dynamic scoring considers these elements when evaluating the impact of policy changes.

- The static model offers a consistent and reliable method for determining the direct fiscal impact of policy change on the economy.

Static Scoring Explained

Static scoring does not offer the full picture of how tax policies affect an economy. It often leads legislators to assess trade-offs between various economic policies, where only immediate monetary repercussions are considered.

It determines the variations in revenue while assuming that consumer behavior related to savings and consumption has no effect on it and GDP remains constant. It offers a one-dimensional view of the impact of tax changes without considering the possible impact of new laws on the overall economy. Since it is an estimation method for quick initial comparisons, it does not consider consumer behavior, savings, consumption, public expenditure, people’s disposable income levels, or other changes seen in an economy due to policy revision. Due to this, its scope is limited in terms of offering input for long-term decision-making.

It ignores economic growth effects since it assumes that people’s spending, investing, and occupation/working habits will remain unchanged. Hence, any government revenue losses that might be offset by these factors remain unaccounted for when this method is applied.

Despite its narrow view, this model is used widely to estimate the direct fiscal effect related to a policy change like a tax cut or expenditure increase. It is seen as a direct and straightforward method to provide a quick and simple forecast of the direct fiscal effect of policy changes. Due to its limitations, its use and applicability are frequently debated. Hence, many experts and critics believe that dynamic scoring, though complex, will be more suitable for economic analysis than this method.

Examples

Let us study a few examples to understand the topic.

Example #1

Suppose the government is introducing a tax cut that would reduce personal or individual income tax rates by 5%. It is estimated that such a tax cut would reduce government tax revenue by $100 billion in the first year based on the current estimates of income tax receipts.

Ava, an officer in the department, has been asked to write a report about it. She applies the static scoring model, which estimates that the tax cut would reduce revenues by $100 billion per year. This method does not take into account that this reduction will likely be reversed in the coming years. She assumes this to be correct because she does not expect or consider any changes in the economy.

Now, due to the tax cut, people may spend more since their disposable income will increase. Hence, consumer spending, which is an economic change, will result in additional tax revenue for the government. Similarly, companies may hire more people than normal since they will have higher retained earnings. This will also boost tax revenue. Several other changes likely will be seen in the economy, which will affect macroeconomic aspects like interest rates, inflation, etc. Such changes can potentially offset all initial loss-driven projections. Ava, being an advocate of static scoring analysis, ignores all these changes.

Since Ava decided to follow the static scoring model, she assumes there will be no economic changes. Based on this, she states in her report that $100 billion will be the annual revenue loss in all subsequent years.

This illustrates the limited nature of conventional scoring models.

Example #2

A 2015 article discussed the use of static scoring in the US. It said that the method assumes the macroeconomic effect of economic policy remains unaffected or zero. However, this was not true. Hence, a mandate was issued to replace the Congressional Budget Office’s (CBO) static scoring method with dynamic scoring.

This decision was made to accommodate the wider economic implications of policy changes, which are crucial for analysis and decision-making. It was concluded that only dynamic scoring models offer a comprehensive picture of policy changes.

Importance

Despite its limitations, it is a key tool in the hands of policymakers to assess the fiscal impact of policy changes. Let us see why.

- It presents a consistent and simple process of estimating the fiscal impact of policy changes. It is a simple yet reliable budgetary estimation tool.

- It helps policymakers anticipate the direct effects of policy changes on government expenditure and revenue, giving an initial glimpse of how things will pan out.

- It is less complex than dynamic scoring, so it is easier to understand and execute.

- It offers reasonable accuracy in terms of quantifying the impact of policy changes on government expenditure and revenue.

Static Scoring vs Dynamic Scoring

The differences between static and dynamic scoring are listed below.

| Parameter | Static Scoring | Dynamic Scoring |

|---|---|---|

| Scope | It assumes policy and tax changes have no impact on taxpayer behavior and other macroeconomic factors. | It considers behavioral and macroeconomic changes on account of policy revision. |

| Visibility | It offers a simple and direct visibility into revenue without further analysis or elaboration. | It offers a detailed view of several economic aspects or factors affected by policy changes. |

| Impact | The economic impact covered for analysis is limited. | The economic impact covered for analysis is comprehensive. |

| Ease of use | It is a simple tool to estimate revenue changes. It is less resource-intensive. | It is a complex methodology that covers various aspects of the economy to arrive at changes triggered by policy revision. It is more resource-intensive. |

Frequently Asked Questions (FAQs)

1. Will it be wise to replace static scoring with dynamic scoring?

Dynamic scoring is complex and takes several uncertainties related to the economy into account. For initial or baseline projects, a static model could work. For a more in-depth look, dynamic models can be employed. A combination of these scoring models might be more beneficial to an economy.

2. Why do policymakers value static scoring?

Since it outlines the direct fiscal effects (spending and revenue) of policy changes, policymakers rely on it for quick assessments within a limited timeframe. Using the figures as benchmarks for swift evaluation and easy comparison also motivates many government departments and analysts to employ this method.

3. Can static scoring be biased or misleading?

By not studying macroeconomic factors and economic growth aspects, this tool might give biased or misleading results. It focuses far too much on the revenue impact, operating in a silo, which is neither suitable for nor relevant to economic development.

Recommended Articles

This article has been a guide to Static Scoring and its definition. We compare it with dynamic scoring, and explain its examples and importance. You may also find some useful articles here –