What Is General Equilibrium?

In economics, general equilibrium exists when demand and supply are in perfect balance or harmony. The primary objective of this theory is to identify the exact circumstances under which demand and supply become equal to each other and prices become stable.

General equilibrium analysis involves an in-depth study of multiple economic variables and their interrelations to understand how various markets of an economy work as a whole. Thus, it differs from the partial equilibrium theory, which analyzes single markets. For an economy to be in general equilibrium, its factor services, For example, firms, and consumers, must be in equilibrium simultaneously.

- General equilibrium definition refers to a theory explaining how the forces of demand and supply dynamically interact in markets, ultimately resulting in a price equilibrium.

- Various assumptions of general equilibrium are unrealistic. For instance, the tastes and preferences of individuals do not remain the same; they keep changing over time.

- Unlike partial equilibrium, this theory analyzes an economy as a whole, considering the interrelations of several variables.

- A French Economist named Leon Walrus developed this theory in the 19th century to address a much-debated economic problem.

General Equilibrium Theory Explained

General equilibrium definition refers to a theory explaining how demand and supply become equal in an economy with various markets working simultaneously. It tries to explain how price, demand, and supply work in an economy, not in a particular or single market.

Leon Walrus, a French economist, developed this concept in the 19th century. Hence, individuals also refer to it as the Walrasian general equilibrium. This concept is the same as economic equilibrium. Both these theories utilize the equilibrium price model to analyze economies.

The concept links cause and effect sequences of the alterations in prices and quantities of products and services concerning the entire economy. The theory holds only if all prices are in equilibrium. In other words, every consumer must spend their income in a way that yields maximum satisfaction. The demand and supply of factors of production must balance each other at equilibrium prices. Moreover, all firms in every industry must be in equilibrium at all output levels and prices.

Assumptions

The assumptions of general equilibrium are as follows:

- Consumers’ habits and tastes remain constant.

- There is no change in production techniques.

- All firms carry out business-related operations under exactly the same conditions.

- The returns to scale remain constant.exists full employment of resources, including labor.

- Consumers’ income remains constant.

- Factors of production (land, labor, capital, and entrepreneurship) remain perfectly mobile between various places and occupations.

- Every unit of a product service is the same.

- Perfect competition exists in services, goods, and factor markets.

Diagram

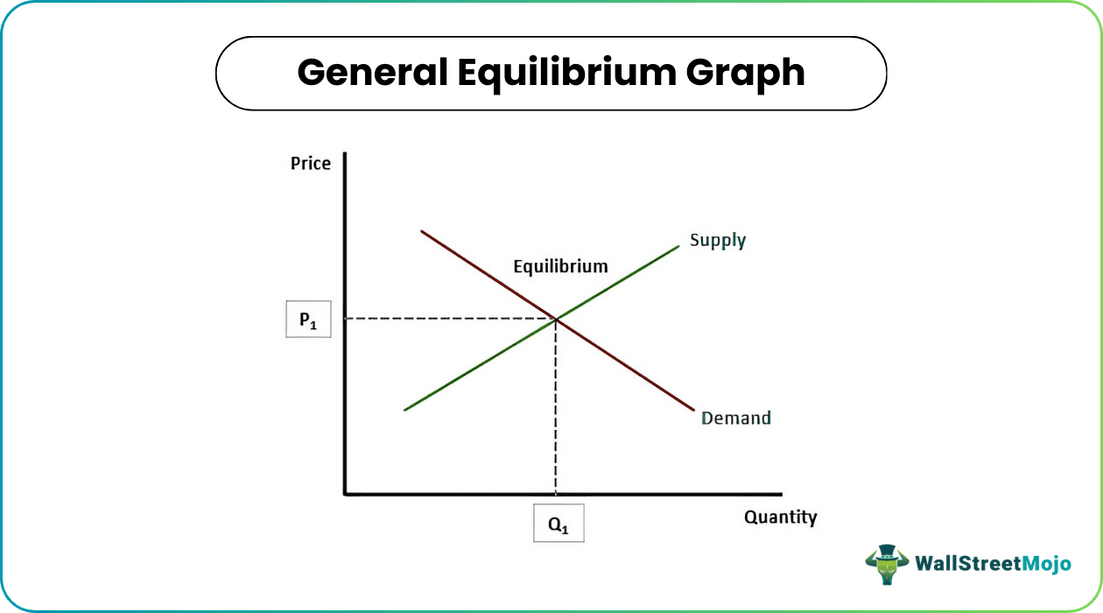

Let us look at a diagrammatic representation of general equilibrium.

As one can observe from the above figure, at price and output levels P1 and Q1, demand and supply balance each other, and general equilibrium exists.

Example

Let us look at a general equilibrium example to understand the concept better.

Suppose there are two sectors only in A’s economy — business and household. The nation’s economic activity involves products, services, and money flowing between these two sectors. Consumers buy products and services in the goods market, and producers receive money from them in the factor market.

In other words, consumers pay producers for purchasing their offerings. In return, producers pay consumers for the services provided to the business, the wages paid for labor, etc. Hence, there is a circular flow of payments between consumers and producers. That said, products and services flow in the opposite direction. Products flow to the household sector from the business sector, and services flow to the business sector from the household sector. Factor and product prices link these two flows.

An economy is in general equilibrium when the volume of income flow from the producers to consumers balances the volume of expenditures from the consumers to producers at certain prices.

Importance

French economist Leon Walrus developed the theory of general equilibrium to address a much-debated economic issue. Before he developed this theory, economic analysis explained the function of supply, demand, and price in single or specific markets. It could not show the existence of equilibrium for every market simultaneously in aggregate.

This theory aimed to demonstrate why and how every free market tends to move towards equilibrium. That said, one must note that the markets do not reach equilibrium. They only tend to move towards it. Hence, economists believe that concept is not realistic.

The theory builds on a free market price system’s coordinating processes. This system shows how traders get involved in a bidding process with other traders and create a transaction via the purchase and sale of goods. The transaction prices signal other consumers and producers to realign their activities and resources along more profit-making business lines. Nevertheless, this assumption has been subject to criticism.

Limitations

The limitations of the theory are as follows:

- Leon Walrus developed this theory based on multiple unrealistic assumptions. For example, perfect competition is a theoretical construct and does not exist in reality.

- General theory analysis is static. The theory assumes that all producers and consumers manufacture and consume identical products regularly without delay and that their economic decisions are in complete harmony. Moreover, consumers’ tastes and preferences remain the same. However, such things do not happen in reality. Consumers and producers do not think and act in the same way. Moreover, consumers’ tastes and habits are constantly changing.

- According to George Joseph Stigler, the theory is a mistake as economic analyses have never been general. He believed that the more general the economic analysis, the less specific its content was.

General Equilibrium vs Partial Equilibrium

There are two approaches to the study of equilibrium — partial and general. Both concepts have crucial contributions to economic analysis. Hence, individuals must have a clear idea of the differences between them. Let us look at them.

| General Equilibrium | Partial Equilibrium |

| Analyzes the economy as a whole. | Analyzes single markets. |

| The impact of several variables is taken into account simultaneously to derive it. | Its derivation involves considering the impact of two variables; all other variables remain constant. |

| Considers interdependence and the interrelations of many variables. | Ignores interdependence between variables. |

| Forms the basis of macroeconomic analysis. | Forms the basis of microeconomic analysis. |

Frequently Asked Questions (FAQs)

1.Does general equilibrium exist?

It only exists when the demand for every product equals the supply. However, many economists believe that the theory has unrealistic assumptions. For example, perfect competition does not exist in reality, and consumers’ tastes and habits do not remain constant. Hence, they think the dynamic interaction of supply and demand forces cannot lead to price equilibrium.

2.Is general equilibrium theory macroeconomics?

It is a macroeconomic theory that analyzes the economy as a whole. The theory extensively studies several economic variables and their correlations to understand how the entire economic system functions. It does not analyze individual markets contrary to partial equilibrium.

3.Why is general equilibrium situation of Walras static?

The theory of general equilibrium is static because of the following reasons:

· All producers and consumers regularly produce and consume identical goods without any time lag.

· Consumers’ goals, tastes, and habits remain constant, and their economic decisions are in complete harmony with that of producers.

Recommended Articles

This article has been a guide to What is General Equilibrium. We explain its assumptions, importance, examples, diagram, and comparisons with partial equilibrium. You can learn more about it from the following articles –