Part of our Supply and Demand guide

What Are Factors Of Production?

Factors of production define resources used to produce or create finished goods and services, the sale and purchase of which keeps the market economy afloat. Determining these factors ensures efficient production and successful completion of projects and purchase orders.

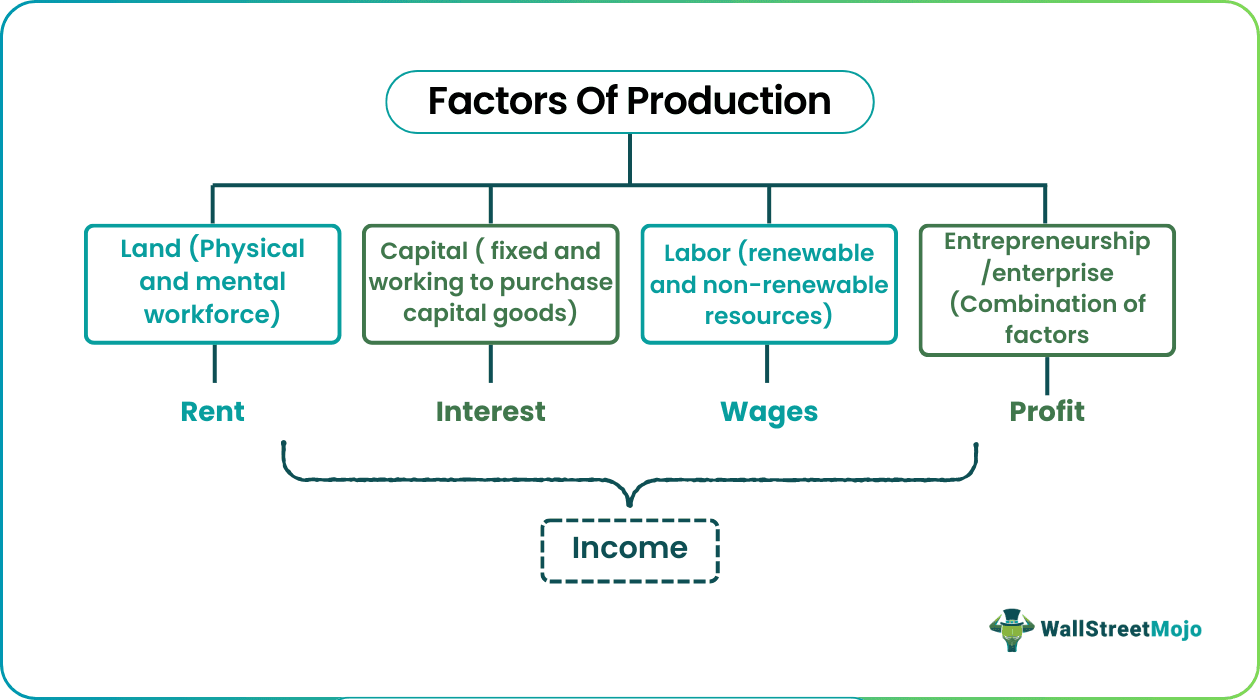

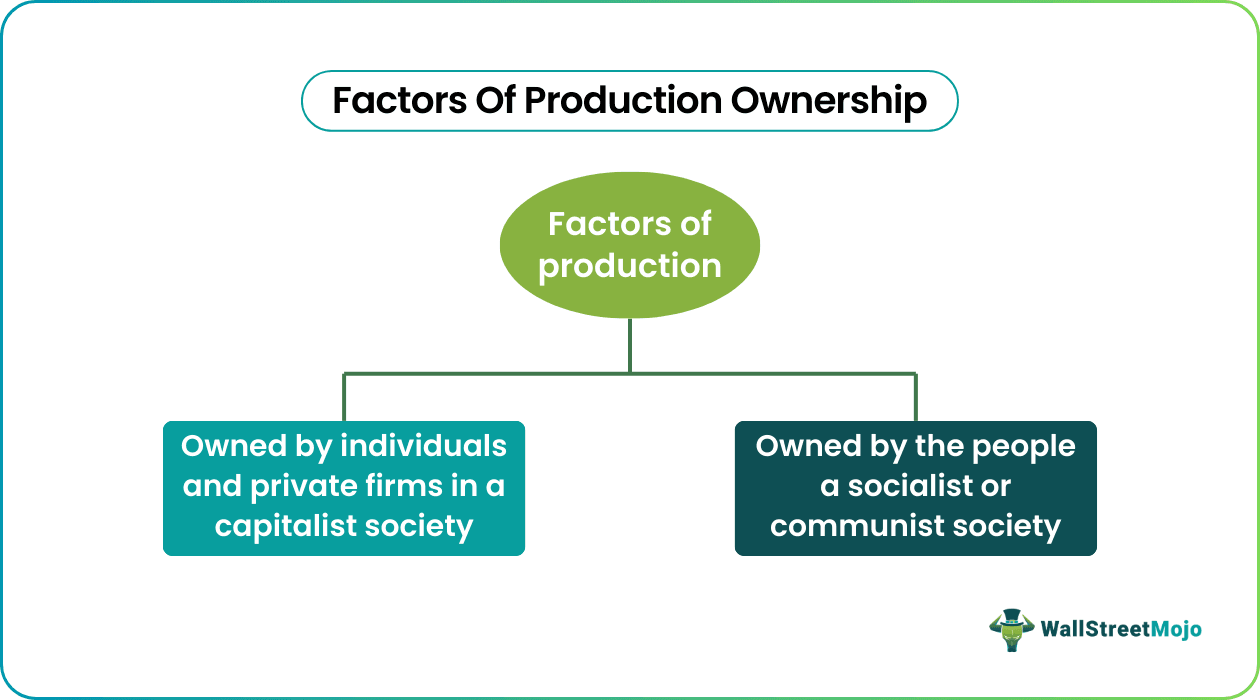

The four factors of production in economics include land, capital, labor, and entrepreneurship or enterprise. Modern economics considers time and information also part of these factors. These factors comprise various resources or inputs needed to generate outputs, measured by the gross domestic product. They are building blocks of an economy, and their ownership varies with the society, industry, and types of economic system (capitalism and socialism).

- Factors of production refers to resources used to produce or create finished products and services to keep the market economy afloat.

- The four common production factors in economics are land, capital, labor, and entrepreneurship/enterprise. Modern economics considers time and information also part of these factors.

- Adam Smith, also known as the Father of Economics, associated the production concept with the creation of material goods only. However, modern economists defined the production process as creating or adding value to the products.

- The ownership of these factors varies with the society, industry, and economic system (capitalism and socialism).

Understanding The 4 Factors Of Production

Factors of production play a crucial role in the production of finished goods and services and economic development. Conventionally, the term production is defined as the process of creating, producing, or manufacturing goods and services using economic resources for financial gains.

Adam Smith, also known as the Father of Economics, associated the production concept with the creation of material goods only. However, modern economists believed that any matter is neither created nor destroyed. Thus, the definition of production shifted from only producing products and services to creating or adding value to them.

To understand production factors, let us explore the four of them below:

#1 – Land

It consists of renewable and non-renewable natural resources, including water, minerals, precious metals, vegetation, oil, natural gas, and other raw materials. As these resources are limited in supply, a land rich in these is considered the best for production. The income generated with this factor is considered rent.

Every product bought and sold in the world could easily find a direct or indirect link to the land. For example, the gold extracted through mining is shaped and processed to design expensive jewelry displayed and sold at different jewelry shops. Plus, cooking oils used to prepare delicious meals also get the taste from the oilseeds obtained from the land.

In addition to agriculture, land can get used for commercial and real estate purposes. However, its contribution to the production process depends on its usage.

#2 – Capital

Even though capital refers to money, money cannot act as an input in the production process. Hence, it cannot be considered a factor but a part of the capital, which entrepreneurs use to purchase capital goods to produce products and services. The income generated with this factor is considered interest.

It comprises resources including manufacturing unit/plant, tools, equipment and machinery, raw materials, finished goods, etc. However, bonds, stocks, and other securities cannot be capital as they do not get used in the production process in any manner.

#3 – Labor

Labor includes both physical laborers and the workforce putting mental efforts as essential resources in facilitating the production of goods and services. The labor force required to achieve better outputs depends on the size and quality of these resources and the production volume. The income generated with this factor is considered wages.

The value of human capital depends on how skilled, trained, educated, and productive it is. When a manufacturing unit has expert and efficient labor, it leads to efficient production and increased sales. After the capital, it is the second factor critical to the production processes.

#4 – Entrepreneurship/Enterprise

Of course, land, capital, and labor are crucial factors, but these necessitate someone or something to oversee and supervise the production process. It is where the fourth variable, entrepreneurship/enterprise, comes into play. This factor combines the other three inputs and activates the most efficient production system to produce the best output.

The person or organization involved is responsible for coming up with new ideas and spotting prospective commercial prospects. They also assume business risks in addition to planning and executing production. The income generated with this factor is considered profits.

Factors of Production Examples

The below-mentioned factors of production examples explain the concept even better. So, let us have a look at them:

Example #1

Ryan has an ancestral farm where his forefathers used to grow oranges. His father suggested Ryan starting orange juice production on the land on a small scale and see how it goes. Ryan, as the fourth factor of production, got involved from the start of the business plan.

He borrowed some money from his father and arranged the second factor of production – capital. He set up a plant in a family-owned building and bought the required machinery to produce a small unit of product at first. The next step was to have the third factor ready, i.e., labor. Ryan hired individuals to process the juice and pack it into bottles. The efforts of the small team led to the efficient production of tasty and healthy juice.

Example #2

In modern economics, time and information have emerged as two new production factors. Also, they play a crucial role in accelerating the pace of production in the competitive market. Since wasting time would only mean a loss, businesses need to develop technological infrastructure to speed up the production process.

Toyota’s Prius, a hybrid electric vehicle, is said to have taken only 15 months to create. The accelerated product development was made possible by integrating advanced techniques and technologies. The company developed and used complex software to equip manufacturing engineers with data and information. It resulted in faster design, development, and deployment processes.

In short, offering sufficient information in a short time could act as the best among the known factors. Above all, they do not require businesses to wait any longer for their research and development activities. All this helped Toyota stay ahead of its competitors and satisfy customers.

Characteristics

When discussing characteristics and the importance of factors of production, it is crucial to pay attention to the ownership aspect of each one. However, ownership varies based on a country’s social, industrial, and economic framework.

In a capitalist society, private enterprises or people own these factors, while in a socialist or communist society, the community or society is the owner of these factors.

Land

The land factor of production can have renewable and non-renewable resources. The former can be used year after year without getting exhausted. These include air, water, etc. The latter can last for a short time before being depleted due to a gradual increase in demand and consumption.

Capital

The capital can be fixed and working. Fixed capital is used continuously in the production processes as a manufacturing unit or plant, tools, machinery, etc., may undergo repairs and replacements whenever required. On the other hand, working capital is only arranged or gathered in cash and accounts receivable once the product gets sold.

Labor

Every business divides its workforce into several categories based on the many parts of the production process. As a result, personnel from diverse departments gain knowledge in specific fields, resulting in outputs that meet the required quality standards.

Entrepreneurship/Enterprise

An entrepreneur allocates capital and segments labor based on their skills and expertise. Entrepreneurship combines the rest of the factors, explores new business opportunities, and takes responsibility for managing risks and uncertainties related to production.

Frequently Asked Questions (FAQs)

What are the factors of production in economics?

Production factors are productive resources used to produce or create finished goods and services to keep the market economy afloat. These resources or inputs are essential for efficient production and the successful completion of projects and purchase orders.

What are the 4 factors of production?

The four production factors are land, capital, labor, and entrepreneurship/enterprise. Of these, labor and capital factors are considered the most critical to the production processes. Time and information have also emerged as two new factors in modern economics.

Who owns factors of production?

The society, industry and economic system (capitalism and socialism) determine who owns these factors. In capitalism, private firms and individuals own these. In socialism and communism, the community or the society is the owner.

Recommended Articles

This has been a guide to Factors of Production in Economics and its definition. Here we discuss 4 production factors with their characteristics and examples. You can learn more from the following articles –