Part of our Economic Theories guide

What Is Classical Dichotomy?

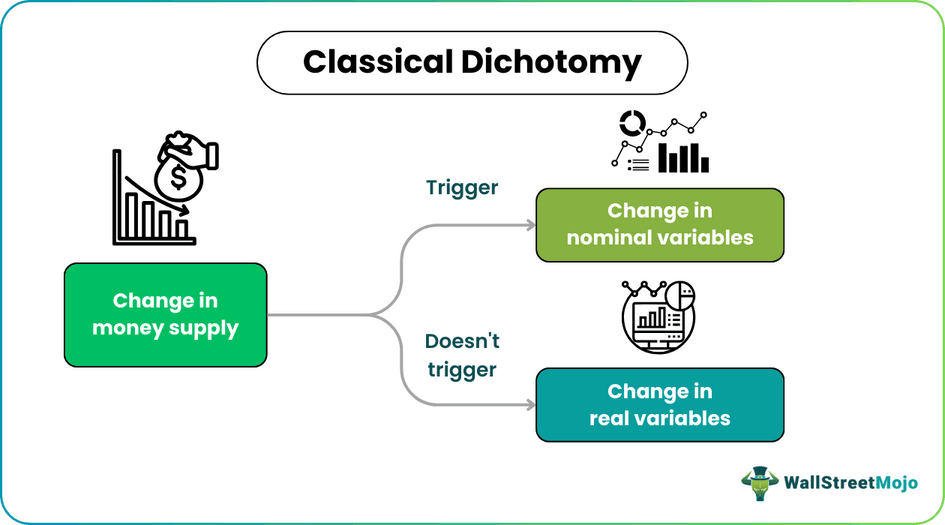

The Classical Dichotomy states that changes in real variables such as interest rates, employment, wage rate, or output (real GDP) are independent of the changes in nominal variables like money demand and supply. It is a pre-Keynesian macroeconomics concept stating that money bisects the economy into real and nominal sectors.

It plays an indispensable role in policymaking and economic analysis. According to the classical dichotomy, long-term changes in the money supply primarily impact nominal variables like prices and nominal income rather than real economic activity. As a result, central banks often prioritize the control of inflation through monetary policy without causing substantial disruptions in actual economic output.

- The classical dichotomy is a fundamental concept in macroeconomics that refers to separating real variables, such as output and employment, from nominal variables, like money and prices, in the long run.

- This theoretical economic concept contributes significantly to government and central banks’ economic analysis and policy formulation.

- However, in the short run, the money supply or price level changes can have real effects due to price stickiness and adjustment delays.

- It differs from the neutrality of money, which signifies that the impact of money supply changes is neutral on the overall economic productivity.

Classical Dichotomy Explained

The classical dichotomy in economics is a concept that distinguishes between real and nominal variables within an economy. Real variables consider adjustments for price changes and reflect the actual physical aspects of the economy, like the volume of goods and services produced or consumed. On the other hand, nominal variables are expressed in current market prices and include factors like nominal income and nominal gross domestic product (GDP).

According to the classical dichotomy, alterations in the money supply or price levels primarily affect nominal variables and have a limited impact on real variables in the long term. This idea is closely associated with classical economics, which posits that the real economy is independent of monetary factors over extended periods. Hence, the variables such as productivity, technology, and resources are the key drivers of sustained economic growth.

The practical implications of the classical dichotomy in economics have significant relevance for policy formulation and economic analysis. However, the real-world economies may deviate from the idealized framework of the classical dichotomy, particularly in the short run. Factors like price stickiness, expectations, and uncertainty can lead to interactions between nominal and real variables. Therefore, policymakers and analysts must consider real and nominal factors in their decision-making and economic analyses.

Examples

In the real world, although the real and nominal economic variables are somewhat interrelated, the classical dichotomy is often applied in the following contexts:

Example #1

Suppose a cement manufacturing company often bases its long-term investment and production decisions on real economic fundamentals rather than short-term price fluctuations or nominal variables.

Suppose Adam invests money in the financial markets. He frequently considers real returns based on economic fundamentals when making long-term investment choices. But, when it comes to short-term investment strategies, he factors in nominal variables like interest rates.

Example #2

Suppose the European economy’s total money supply is fixed at 1,000 euros. The economy operates at full employment, and all markets are in equilibrium.

Suppose the central authority in Europe decides to double the total money supply to 2,000 euros. According to the classical dichotomy in economics, this increase in the money supply should not influence the real variables in the economy because other factors remain unchanged. Here’s what would occur:

- Price Level: Inflation would ensue due to the augmented money supply. Prices of goods and services in Europe would double.

- Real GDP: According to the classical dichotomy, real GDP, which represents the total output of goods and services, would remain unaffected in the short and long term. The production capacity and resource availability in Europe remain constant.

- Employment Rates: Employment rates should likewise remain unaltered, assuming no underlying economic circumstances change. The increased money supply does not create new jobs or decrease employment.

- Real Wages: Real wages, adjusted for inflation, would stay consistent. The surge in the money supply does not impact workers’ productivity or labor demand.

- Real Interest Rates: Real interest rates would remain stable, representing the return on investment (ROI) adjusted for inflation. The increase in the money supply does not modify the essential determinants affecting interest rates.

Importance

The classical dichotomy plays a pivotal role in economic analysis and policy formulation. Its significance lies in the following aspects:

- Facilitates Economic Analysis: The classical dichotomy simplifies economic analysis by allowing economists to separate the actual and monetary dimensions of the economy.

- Monetary Neutrality: This concept focuses on monetary neutrality, implying that central banks’ actions primarily affect prices but not actual economic output.

- Long-Term Policy Implications: It aids the policymakers in recognizing that, over time, real economic growth hinges on factors like productivity and technology rather than fluctuations in the money supply.

- Inflation and Price Stability: The concept exaggerates the link between money and prices, enabling central banks to aim for price stability and curbing inflation.

- Government Fiscal Policy: It even suggests that fiscal policies, i.e., government spending and taxation, have a more direct effect on actual economic variables. For instance, government investments in infrastructure or education can boost long-term economic growth.

- Understanding Economic Shocks: In analyzing economic shocks, economists and policymakers often distinguish between real shocks (e.g., technological advancements or natural disasters) and nominal shocks (e.g., changes in the money supply or inflation).

Difference Between Classical Dichotomy And Neutrality Of Money

The classical dichotomy and the neutrality of money are closely related concepts in macroeconomics, but they address different dimensions of the economy. Here’s a comparative analysis:

| Basis | Classical Dichotomy | Neutrality of Money |

|---|---|---|

| Definition | The classical dichotomy emphasizes the independent behavior of real variables (e.g., output, employment, production of goods and services) and nominal variables (e.g., money, prices, nominal income) in the long-term economic perspective. | The neutrality of money in economics suggests that alterations in the money supply primarily affect nominal variables like prices and wages without causing substantial real economic impacts such as changes in employment, production, or overall economic output. |

| Focus | Believes that variations in the money supply primarily influence nominal variables while exerting minimal long-term impact on real variables | Emphasizes that variations in the money supply do not affect real economic variables in the long run |

| History | Introduced in 1965 by Don Patinkin, an American educator, sociologist, and economist | Discovered in 1931 by Friedrich A. Hayek, an Austrian economist |

| Long-Run Perspective | It offers insights into the long-term view of economic dynamics, suggesting that genuine economic factors, such as technology, productivity, and resources, determine real economic outcomes. | It suggests that the economy eventually adapts to changes in the money supply, leaving real economic variables unaffected in the long run. |

| Policy Implications | It supports the policymakers and the central bank in bringing price stability and controlling inflation by studying the factors that affect real economic outcomes. | It aids central banks in prioritizing inflation reduction and price stability instead of using monetary policy to stimulate real economic growth. |

Frequently Asked Questions (FAQs)

1. What is the formula for a classical dichotomy?

The classical dichotomy equation is MV = PY, where M is the money stock, V denotes money circulation velocity, P indicates the price level, and Y represents the income level.

2. Who invented the classical dichotomy?

The classical dichotomy was introduced in 1965 by the economist, educator, and sociologist Don Patinkin. It was a foundational concept in early economic thought, particularly in the 18th and 19th centuries, and contributed to the development of modern macroeconomics.

Contemporary macroeconomics recognizes the complexity of the relationship between nominal and real variables in the real world, considering factors like inflation expectations and market imperfections.

3. What are the implications of classical dichotomy?

While the classical dichotomy offers valuable insights into the relationship between money and the economy over the long term, it simplifies the complexities of the real world.

In the short run, changes in the money supply and inflation can indeed affect economic activity through channels like uncertainty, sticky prices, and wealth effects. Consequently, contemporary macroeconomic models incorporate short-term and long-term considerations when analyzing economic dynamics.

Recommended Articles

This article has been a guide to what is Classical Dichotomy. Here, we explain its examples, differences with the neutrality of money, and its importance. You may also find some useful articles here –