Part of our Costing Methods guide

What is Job Costing?

Job costing is a process of determining the cost associated with a job or work, which helps analyze the applicable per unit cost of each job in the entire production. The job costing sheet can be understood as a specific work, contract, or batch done or completed to achieve any goal.

When the specific order costing is applicable, that time for some products, the experts try to find out job costing or contract costing of the product to get the exact costing of the particular work. It is prevalent in those industries where the production is done in batches.

Job Costing Explained

The job costing mechanism in accounting is technically a very efficient way of determining the cost of each job in a production unit. The management can easily understand which item is profit-generating and which is loss-making. The organization can avoid such future items and think of adding another substitute for the same. All in all, the cost allocation is done through this process very smoothly. All the expenses are evenly distributed.

However, it is a known fact that whenever any organization thinks of having an efficient mechanism, they have to bear the cost for the same. Only big organizations can afford this. The experts are hired to control the costing mechanism, which is costly.

Whenever the organization is ascertaining the normal loss during the finalization of the cost sheet, the loss is evenly adjusted to the total output. Whenever there is an abnormal loss, the loss is adjusted under the profit and loss account statement. Also, if the mistake in the cost sheet is due to the incorrect entries in the inventory books, rectification is done by charging the cost to its inspection department, not the manufacturing department.

Each job or work for the production is considered a separate item. The profits can be easily identified by adjusting the losses. Still, due to its cumbersome detailing, the cost sheet loses its importance, and most organizations fail to include all the material, labor, and overhead details in their cost sheet. If this loophole can be fixed, then the job costing system will become very efficient for all organizations.

Objectives

Let us understand the objectives of incorporating a job costing system through the points below.

- Job costing aims to provide accurate and precise cost information associated with specific projects or jobs within a company.

- It facilitates effective budgetary control by tracking and comparing actual costs against budgeted costs for each job, ensuring financial accountability.

- Enables a detailed analysis of the profitability of individual projects by assessing revenue generated against the direct and indirect costs incurred.

- Helps in allocating resources efficiently by identifying the labor, materials, and overhead costs associated with each job.

- Job costing allows for the evaluation of the performance of different departments or teams by analyzing their ability to manage costs within the specified budget for a particular job.

- Assists in setting competitive and profitable pricing for future projects based on historical cost data, ensuring accurate and competitive quotes.

- Provides valuable data for decision-making by offering insights into the financial performance of individual projects, aiding in strategic business decisions.

Features

A job costing sheet comprises different factors within the business and the culmination of all these factors gives the management clarity on things like budgeting, raw material, etc. Let us discuss its features through the points below.

- Direct Material

- Direct Labor

- Direct Expenses

- Prime Cost

- Cost of Production

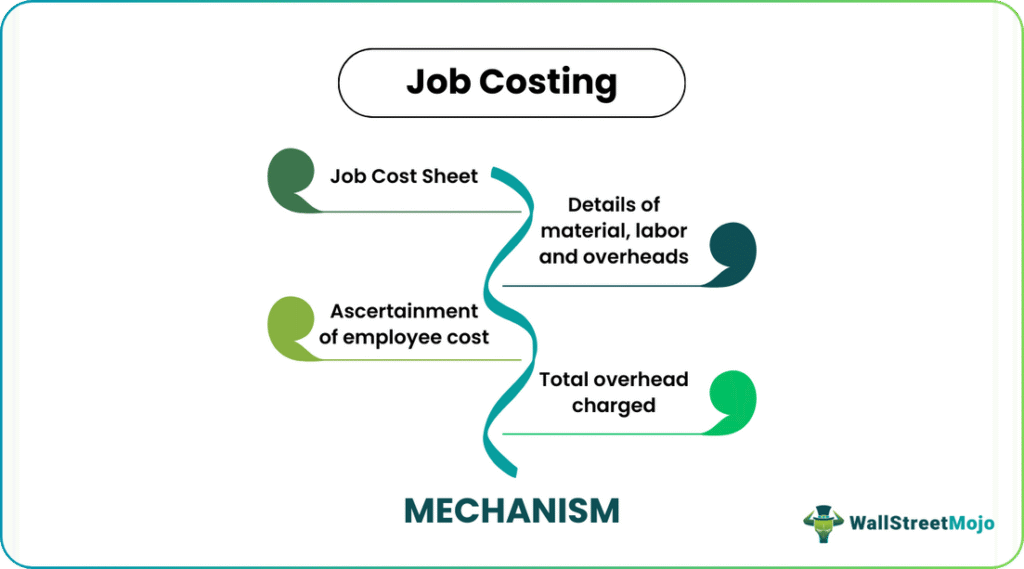

Mechanism

Let us understand the mechanism of a job costing system through the points below.

- Each year a Job cost sheet is prepared by an accounting expert.

- Details of material, labor, and overheads are given.

- Ascertainment of employee cost to each job separately;

- On completion of the job, the total overhead is charged on the jobs separately.

Types

Each type of job costing is tailored to the specific characteristics and requirements of the industry or business, providing a flexible framework for cost tracking and analysis.

- Job Order Costing: Used in industries where products or services are customized to meet specific customer requirements. Each job is treated as a separate entity, and costs are tracked individually.

- Batch Costing: Suitable for industries producing similar but not identical products in batches. Costs are averaged over the entire batch, providing a cost per unit for that batch.

- Contract Costing: Applied to large-scale projects or contracts, such as construction or consulting. Costs are accumulated and assigned to a specific contract, treating it as a distinct unit.

- Service Costing: Primarily for service-oriented industries. It focuses on tracking costs related to providing a specific service, often on a per-job basis.

- Unit Costing: Applicable in industries with standardized, mass-produced items. Here, costs are attributed to each unit produced, allowing for precise cost determination per unit.

Examples

Now that we understand the basics and intricacies of a job costing sheet, let us also understand the practical applicability through the examples below.

Example #1

In a paper mill, the manufacturing cost of the entire production is $1,000, and 5% of the production is generally rejected or not used. The realizable value of the rejected products is $20. The typical loss, as per company norms, is estimated at 2%. How do you find the job cost of different products?

Solution:

- Loss due to rejection is 5%, i.e. 5% of $1000 = $50.

- Normal Loss is 2%, i.e. 2% of $1000 = $20.

- Therefore, the abnormal loss = $50 – $20 = $30.

Therefore, the normal and abnormal loss ratio comes out to be $20:$30 = 2:3.

If the rejection is inherent, the same cost is incorporated into the manufacturing cost. But suppose it is not identified with the jobs. In that case, the cost due to rejection is settled with factory overheads.

The manufacturing cost will be written off in the profit and loss statement.

The distribution of the cost as per its job will be done as follows:

- Work in progress = $50.

- Material Cost = $20.

Abnormal loss of $30 will be allocated in the ratio 2:3:

- Therefore, Overhead = $30*2/(2+3) = $12

- Manufacturing cost written off to Profit and Loss = $30*3/(2+3) = $18

Example #2

Jobber, the leading operations management software, came up with a new job costing feature that could allow painters, construction companies, contractors, landscapers, tree care providers, HVACs, and others to efficiently take note of the costs involved in a project and their profit margins.

With the costs of materials and labor going up towards record highs, this feature, launched in July 2023, shall be helpful to determine the profitability of a project.

Advantages

Some of the advantages of a job costing sheet are as follows:

- Provides Details: The complete details of the material, overheads, and labor can be ascertained because the cost is segregated job-wise.

- Profits Assessment: The profits from each job can also be ascertained separately.

- Production Planning: It helps the organization plan, and the storekeeper can easily manage his inventory.

- Budget: They can also help the organization in making their budgets. The estimation can be drawn easily by following the job costing method.

- Abnormal Loss: They can also help the organization in making their budgets. The estimation can be drawn easily by following the job costing method.

Disadvantages

Despite the various advantages, there are a few factors from the other end of the spectrum as well that prove to be a hassle. Let us understand the disadvantages of a job costing system through the points below.

- Expensive: This technique is beneficial. It requires an expert to do the same. For any big organization, when there are a lot of transactions, it is difficult for them to ascertain the cost. Therefore, they are required to hire an expert, and the expert charges professional fees.

- Cumbersome: In the case of a big organization, where there is lots of material, labor, and overheads used, the detailing of each item to prepare the cost sheet becomes cumbersome.

- Fails to Consider Inflation: It fails to consider the inflation effects. When the cost sheet is prepared, all the details are recorded, but the process of the job costing cost sheet is such that the effect of inflation cannot be incorporated due to its limitations. Therefore, it gives a wrong calculation of profits, especially if the cost sheet is prepared in the middle of the month.

- Market Condition: The market condition for preparing a job cost sheet is critical. Sometimes uninvited factors like labor strikes, nonavailability of products, etc., make the calculation inaccurate.

Job Costing Vs Process Costing

Let us understand the distinctions between job costing anf process costing through the comparison below.

Job Costing

- Ideal for industries with custom or unique products or services where each job is distinct.

- Tracks costs associated with each specific job individually, allowing for precise cost allocation.

- Highly flexible, accommodating variations in production methods and materials for different jobs.

- Custom furniture manufacturing, construction projects, and advertising campaigns are some of its examples.

Process Costing

- Suited for industries with continuous and standardized production processes, producing homogeneous products.

- Accumulates costs over a specific production period and averages them over the total units produced.

- Maintains consistency in cost allocation, making it practical for large-scale, repetitive production.

- Examples include oil refining, chemical processing, and food manufacturing.

Recommended Articles

This article has been a guide to what is Job Costing. Here we explain its features, examples, advantages, and disadvantages, and compare it with process costing. You can learn more about accounting from the following articles –