Part of our Estate Planning guide

What is a Living Trust?

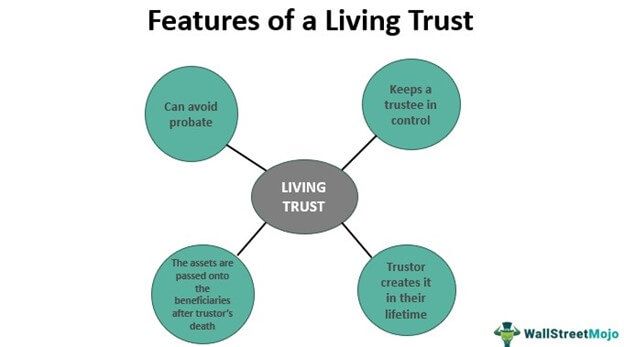

A living trust is a legal document created during a person’s lifetime that adds assets such as cash, real estate, stocks, and bonds into a trust. A trustee is appointed to handle the administration of the trust. Upon the grantor’s death, the assets are dispersed to the beneficiaries.

The trust creator enjoys full ownership and exclusive use of the assets that belong to the trust. The trustee holds the legal possession and manages the trust according to the will and wish of the trust creator. The trust can be both revocable and irrevocable.

- Living trusts are legal documents that allow a person to place their assets in a trust and assign a trustee to distribute them upon their death.

- It can help one avoid probate.

- There are two main types of living trusts: revocable and irrevocable. Revocable trusts can be changed, and irrevocable trusts cannot.

- There are no automatic estate tax savings for a living trust, and one needs to have a will even if they have a trust, especially if there are minor children involved.

Living Trust Explained

Living trusts can be created through estate attorneys or online legal programs such as LegalZoom.

Before meeting with an attorney, a person needs to create a list of their assets and decide who they’d like to leave those assets. They should decide on the trustees who will be in charge of the assets when the person is alive and after the death.

Once this information is decided, a legal document is created, and the trust maker will need to transfer assets to the trust. It means placing property, life insurance benefits, and other assets in the trust’s name.

A trustee must be appointed to handle all of the administration work. The trustee is usually the creator of the trust or “trust maker” if they are still living. A successor trustee should handle the administration after the trust maker’s death.

Assets can be distributed in full upon the trust maker’s death or slowly dispersed over time. Disbursement is dependent upon the wishes of the trust maker.

Types of Living Trust

There are two types of living trusts: Revocable and Irrevocable.

Revocable Trust

A revocable trust can be terminated or changed until the death of its creator. Upon death, it becomes irrevocable. For example, if an individual created a trust for their grandchild and placed $100,000 in it and wanted to take out half the money five years later, they could. However, after their death, nobody could make changes to the trust.

Irrevocable Trust

An irrevocable trust cannot be changed or terminated after the trust maker finalizes it. So, for example, if they’ve created a trust for a child, placed $1,000,000 in it and two years later, decided they wanted to take half the money out – they couldn’t.

There are many types of irrevocable trusts. They are generally used to avoid taxes or protect assets such as property.

Here are a few of the most common types of irrevocable trusts:

- Life Insurance Trusts -These trusts can be made three years before the grantor’s death and are intended to help avoid higher estate taxes by placing life insurance proceeds in a trust.

- Special Needs Trusts – The special needs trust allows grantors to create a trust for a person with special needs without the trust affecting the beneficiary’s ability to receive government benefits.

- Generation-Skipping Trusts – Wealthy families use these trusts to help reduce estate taxes.

- QTIP Trust – QTIP stands for Qualified Terminable Interest Property. Married couples commonly use this trust to provide one spouse income if the other dies. If both spouses die, the trust can be passed on to the next beneficiary.

Benefits

One of the most significant benefits of having a living trust is ensuring that the assets of a person go where they’d like after their death. It eliminates the family from fighting over property and gives the creator peace of mind knowing that their wishes are being met.

Another benefit of these trusts is that it doesn’t have to go through probate court like a will. With a living trust, the trust beneficiaries will quickly have access to the assets left to them.

Living trusts also afford a person privacy. For example, if they create a living will, the courts will publish it upon their death. On the other hand, a living trust is not made publicly available.

And if someone has children who aren’t at the age to manage large amounts of money responsibly, a living trust will provide them peace. It will allow them to stagger payments or withhold payments until the children are of certain ages. For instance, the person could give your children money three times, at ages 25, 30, and 40. Another option would be to stipulate that the children have to be at least 30 to be administered their inheritance.

Limitations

A living trust can be an efficient way to manage assets and delegate where they go after a person’s death. However, there are a few limitations to it:

- Even though using a living trust is a great way to disperse the assets upon one’s death, that doesn’t mean you don’t also need to create a will. This is especially true if they have minor children and need to name a guardian for them in the event of the parent’s death.

- Creditors can sue the trust for debts owed.

- No automatic estate tax savings.

- Another disadvantage is the sheer amount of paperwork that can come with it. A person will need to retitle the assets into the trust’s names. If they have several investments, this can be a lot of work.

Frequently Asked Questions (FAQs)

What is the difference between a living trust and will?

Wills are used to ensuring the flow of assets to beneficiaries after the grantor’s death, while trusts can be created and used when the grantor is alive. In addition, people often use living trusts to avoid the complex legal process of probate associated with a will.

What is the downside of a living trust?

The downsides of a living trust include loss of control over the assets, transfer taxes, and record maintenance. Similarly, there are no automatic estate tax savings in such a trust, and creditors can sue a person if debts are owed.

Do living trusts avoid probate?

Unlike wills, living trusts are beneficial to avoid probates, which is a complicated and expensive process with a long list of legal requirements. In addition, since the trust can be created when the grantor is alive, the assets are automatically passed on to the beneficiaries after the trustor’s death without any court requirements.

Recommended Articles

This has been a guide to what is Living Trust and its definition. We explain types of living trusts – Revocable/Irrevocable, their benefits, & limitations. You may also have a look at the following articles to learn more –