Part of our Banking Services and Operations guide

Creditor Meaning

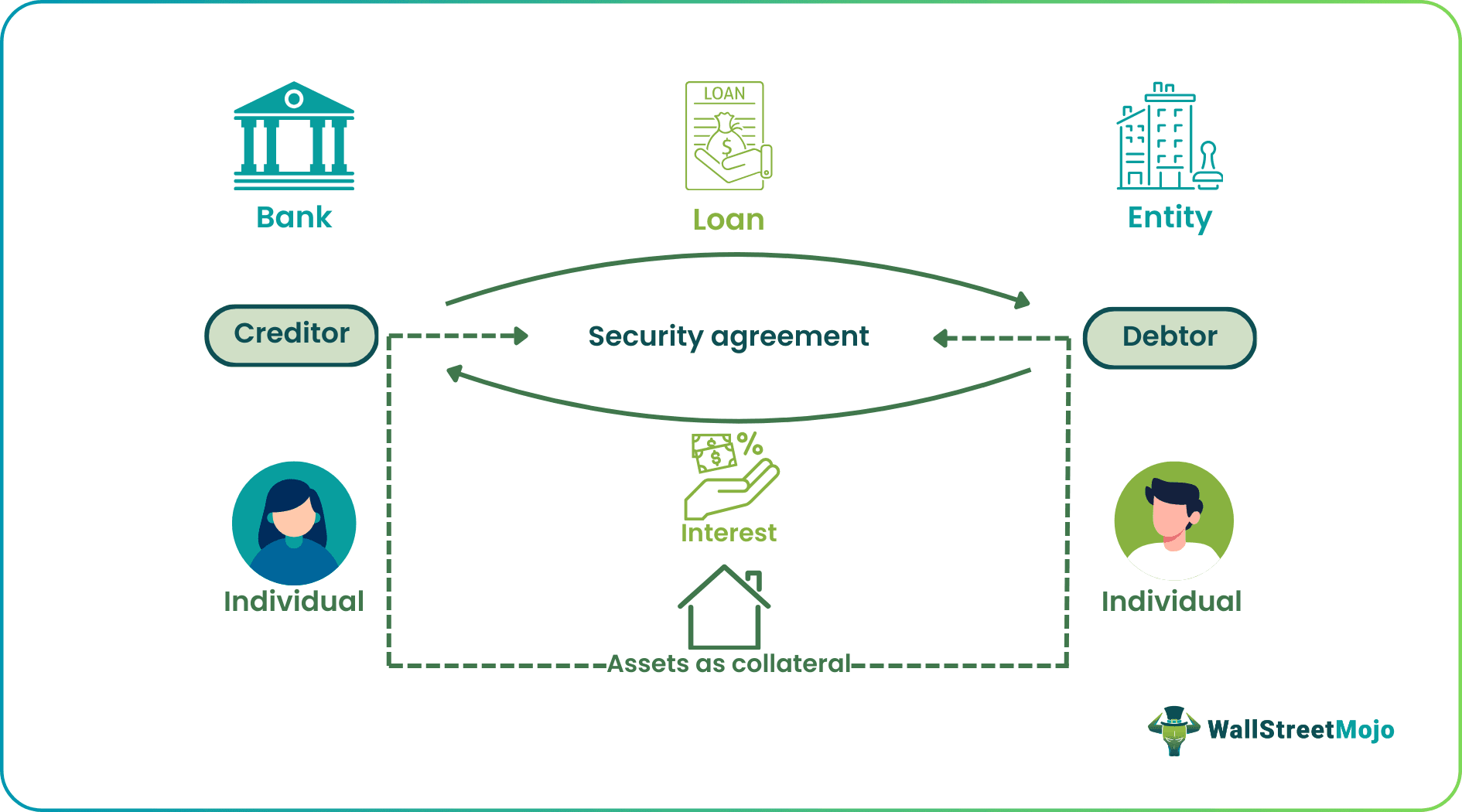

A creditor refers to a party involving an individual, institution, or the government that extends credit or lends goods, property, services, or money to another party known as a debtor. The credit made through a legal contract guarantees repayment within a specified period as mutually agreed upon by both parties.

Debtors running out of funds can receive credit immediately without the obligation of paying it back instantly. The amount lent to the borrower may be subject to an interest rate, depending on its size and the lender. A creditor takes various measures to secure the loan amount if the debtor turns defaulter, like requiring collateral and placing liens on it.

- Creditor definition refers to an individual, entity, or government that lends money or extends credit to people or organizations in need. The loan amount may come with or without an interest rate and with a deadline.

- Creditworthiness and credit scores determine the loan interest rate. Low-risk individuals get loans at cheaper rates, while high-risk seekers are liable to pay higher rates.

- Personal lenders are friends and family members, while the real ones are financial institutions, including banks.

- A secured creditor has the right to claim on the assets or properties of debtors in case they turn defaulters.

Explanation

The history of lenders can be traced back to ages when people used only gold and other metals as the only means of credit. From metals in ancient times to cryptocurrencies today, the form of money has changed.

The answer to what is a creditor – is that it is an entity that lends money or extends credit to the debtor for buying goods, properties, and services without having to pay for them immediately. Instead, the customers can have their monthly payments done at once as per the amount they owe. Lenders can be:

- Personal – Someone from the family or friends from whom one borrows money.

- Real – An individual or institution that lends money under strict repayment conditions and repossesses collateral if the loan remains paid. Because of the risks associated with lending, it can be secured and unsecured.

How Do Creditors Make Money?

There are a few things that secured lenders are very particular about, such as interest rate. They levy it on borrowers and keep making money from it till the loan repayment However, it can vary depending on the amount lent and the lender.

Multiple factors determine the credit interest rate, such as:

- Creditworthiness: Lenders offer debtors a loan only if they find them worthy enough to repay it. Before deciding the interest rate, they assess their creditworthiness based on their income and other financial liabilities.

- Credit Scores: Financial institutions use credit scores to know if a particular loan seeker is a low-risk debtor or high-risk debtor. For the loan applicants who appear high-risk to lenders, the interest rate charged is considerably more than their low-risk counterparts.

Creditors Examples

Credit can be offered for several purposes, given different types of lenders. A debtor can seek loans for mortgage, education, automobile, purchasing goods and services, etc. Here are a few examples to better understand the process:

- A software engineer named Alice (borrower) decides to buy a car and approaches the Alpha Bank (secured lender). The bank is happy to help her, but it does a few checks on her credit score and ability to repay the loan before agreeing to her request. Upon finding that she meets all the requirements, the bank asks her to attach any asset worth the loan amount as collateral. It then offers her a loan of $30,000 with a 3% interest rate and 4 years period to pay back. Even though Alice has to pay an additional amount over the principal amount, she will get enough time to repay the loan. On her failure to do so, the bank can seize the collateral to cover the loan amount.

- In another example, a plumbing machinery retailer (borrower) takes a loan of $15,000 from a contractor (unsecured lender) with a credit term of 2 months. But before paying the loan amount back, the retailer files for bankruptcy. Since the contractor is an unsecured lender and could not ask for any collateral, it can only claim a small portion of the retailer’s assets, resulting in a loss of loan amount.

- Due to the repercussions of the COVID-19 pandemic, many people have lost their jobs, and businesses have faced restricted customer activities. Unfortunately, the situation continued to be the same with the second wave of COVID-19. Therefore, many lenders have introduced multiple schemes with lenient terms and conditions for the people and institutions in need.

What Happens When Creditors Don’t Repay?

While personal lenders do not impose any strict repayment terms on debtors, real ones do. The latter can be categorized in to secured and unsecured. The repayment terms for debtors are always applicable, regardless of the type of lender.

- Secured Creditor always makes sure they get their borrowed amount, such as a mortgage, back at the specified time. They secure the amount against an asset termed collateral, which they seize to cover the losses from the unpaid loan.

- Unsecured Creditors trust the borrowers based on the signed contracts, the terms of which are mutually agreed on by the parties involved. With that said, they can claim a part of the assets in case the debtors go bankrupt.

Personal lenders might use the non-repaid amount as a short-term capital gains loss for income tax benefit. However, to make sure they convert their loss into a tax gain, they need to reclaim the debts as proof of non-repayment despite multiple reminders.

If the debt remains unpaid and lenders move to the court of law, the legal authority can take relevant actions to make sure they get their lent amount back. Typically, the process goes through four stages, including the complaint filed by the lender, review of the debt by the borrower, hearing in the civil court, and the court verdict.

The US Treasury can garnish lenders’ social security benefits in the event of defaults. Whether it is retirement, disability, or any other kind of benefits, debtors are likely to lose out on the same if their debt remains unpaid.

Creditors In Accounting

In accounting, creditors are people or organizations like banks and credit unions that offer products and services to the other party without asking them to pay back for it instantly. The term is also found synonymous with the word “supplier” or “vendor”.

For example – when a wholesaler sells the products to a retailer on credit, it becomes the lender, whereas the latter acts as a debtor. Here, the payment does not intend to be made immediately after the purchase. Instead, the debtor can pay for the goods and services at once as a whole.

Similarly, when the same retailer sells those goods and services directly to a consumer on credit, it becomes a lender, and the consumer acts as a debtor. In both cases, the debtor can have their sheet maintained on a quarterly or monthly basis, according to which they can pay at the end of the specified period.

Frequently Asked Questions (FAQs)

Frequently Asked Questions

Who is the creditor?

<p>A creditor is an individual, institution, or government that extends credit or lends money to another party, given an agreed-upon on-time repayment assurance.</p>

What is the difference between creditors and debtors?

<p>Creditors lend money to people or organizations immediately with the guarantee of getting it back at a specified time. Debtors receive the money instantly with the obligation of paying it back in the given time frame.</p>

Are creditors an asset or liability?

<p>In accounting, under the <a href=”/balance-sheet/”>balance sheet</a>, creditors are considered liabilities while debtors are assets. It happens because debtors signify the amount receivable by a party, and lenders represent <a href=”/accounts-payable/”>accounts payable</a>.</p>

Recommended Articles

This has been a guide to What is a Creditor & its Meaning. Here we discuss types of creditors and how does it work along with examples. You may also have a look at the following articles to learn more –