Debt Meaning

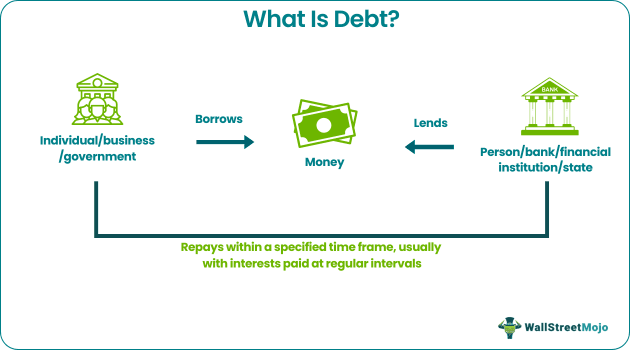

Debt is the practice of borrowing a tangible item, primarily money by an individual, business, or government, from another person, financial institution, or state. The one who accepts the funds is the borrower or debtor, while the one giving it is the lender or creditor. It may be in the form of cash, mortgages, bonds, notes, and personal or commercial or student or credit card loans.

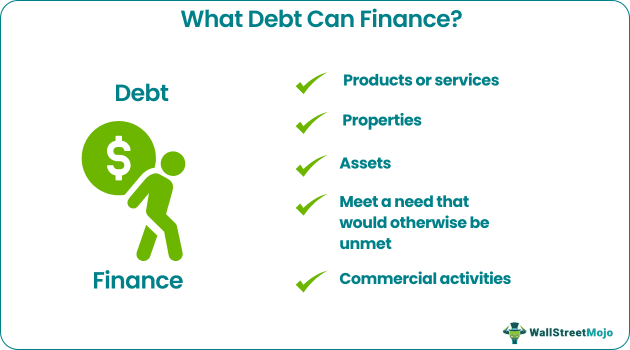

An individual or entity typically requests funds to purchase products, properties, assets, services, or meet a need that would otherwise be unmet. The borrower agrees to return the amount within a specified time frame, usually with interests paid at regular intervals. Based on the collateral backing the loan, it can be secured, unsecured, or guaranteed.

Key Takeaways

- Debt is an arrangement where one party (borrower) borrows money from another (lender) in a mutual agreement to return it with interests within the set period and per the contract terms.

- An individual or company may often request funding to make expenditures, fund commercial activities, or meet an unmet need.

- The main types of debt are secured, unsecured, revolving, non-revolving, corporate, and sneaky. Mortgages, bonds, notes,

- and personal, commercial, student, or credit card loans are all its examples.

- A borrower must weigh the pros and cons of debt financing to pay it off quickly. A secured loan necessitates collateral, which the lender may confiscate if the borrower defaults.

How Does Debt Work?

Debt is the most common form of money borrowing at personal, commercial, and governmental levels. For example, an individual, a business, an employee, or a student can require funds for buying products and services, capital purchases, real estate, or paying tuition fees, respectively.

People and entities usually seek financing when they cannot afford to pay for things under normal circumstances due to income, saving, and expense constraints. So they approach the concerned party or authority, especially banks and financial institutions. Based on the purpose of the loan requested, the borrower can receive it in cash or bank accounts or have it transferred to the provider of products or services, such as the college or university, automobile showroom, hospital, real estate broker, etc.

Companies may also seek loans by issuing bonds to cover operating or capital needs, such as stock buybacks or business acquisitions. Similarly, countries can borrow money from other countries or international organizations to help stabilize their economies or build, support, or improve their infrastructure.

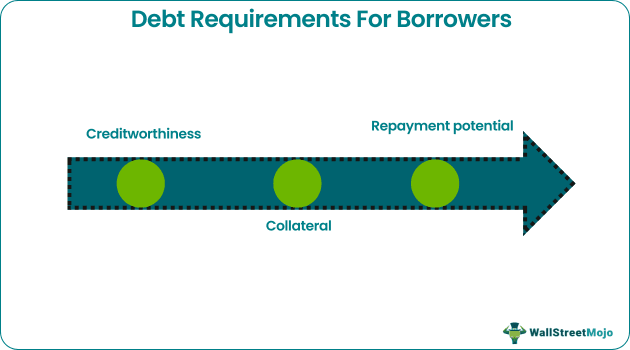

Most banks offer secured loans for a limited time which the borrower backs up with their creditworthiness or collateral that can be an asset. In return, the borrower must pay interest rates and repay the principal amount. If the borrower fails to make the monthly or timely installments accumulated with interest rates, the financial institution can claim or seize the asset in question.

The interest is typically a fixed percentage of the loan that gives a sense of security to the creditor and urgency among borrowers. It can be tax-deductible for mortgages or nondeductible for consumer loans. The interest paid on loans incurred by a company is tax-deductible. A loan with stricter terms can put financial burdens on the borrower.

Types Of Debt

There are several types of debt financing that the borrower must be aware of for better debt management and debt relief:

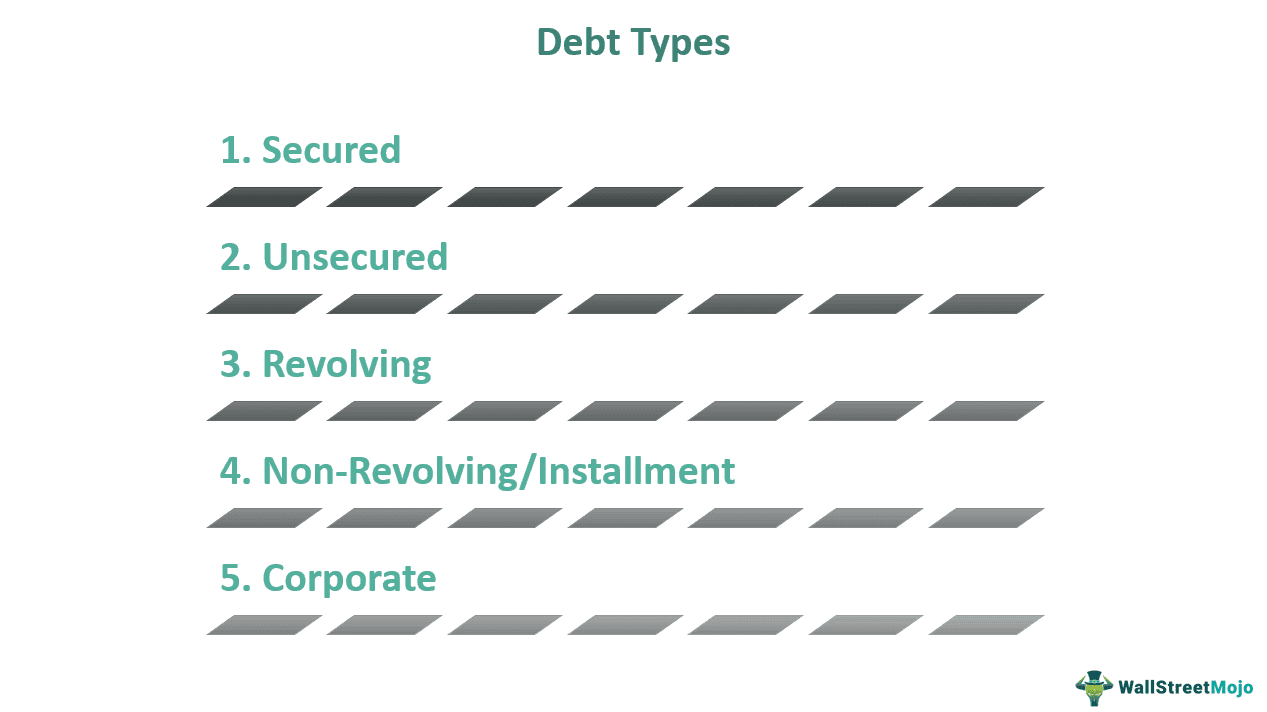

#1 – Secured Debt

It requires the borrower to put up collateral, such as a tangible asset or property, to secure the loan. In addition, the lender must refund the borrowed funds on a mutually agreed-upon date. The bank analyzes the borrower’s creditworthiness and ability to pay before granting the loan.

If the borrower fails to make monthly payments, the creditor has the power to take possession of or sell the asset or property in question for debt recovery. Common examples include automobile, mortgage, and credit card loans.

#2 – Unsecured Debt

It does not require the borrower to secure the loan with the collateral. Hence, the lender may face difficulty retrieving the money if the borrower defaults. That is why the lender considers the creditworthiness and repayment potential of the borrower when issuing the loan.

Furthermore, in unsecured loans, the interest rates are usually higher than any other loan form. If the borrower fails to repay the loan, the lender may file a lawsuit against them to cover the losses. Common examples include credit card bills, medical costs, student loans, payday loans, etc.

#3 – Revolving Debt

It is a cycle of loan where the borrower can borrow up to a specific credit limit as long as they keep making small amounts of payments to the creditor. Moreover, it gives the borrower the flexibility to borrow the money and repay the balance per their need and convenience. Also, the amount lent changes with time. Examples include credit cards, store cards, or credit accounts at local grocery stores.

#4 – Non-Revolving/Installment Debt

It is a one-time credit option, where the borrower borrows a particular amount of money for a specific time and pays monthly installments. Thus, it takes an ample amount of time to clear off completely. Like all loans, it carries high-interest rates. As a result, the borrower pays a significant amount compared to what they have borrowed. Examples include student and home loans.

#5 – Corporate Debt

Apart from individuals, corporations may also seek funds to further their business-related activities. These types of loans are known as corporate loans. Businesses raise capital by issuing these loans to investors in the form of bonds or notes with the promise of repayment. However, firms need to refund the amount to bondholders at a predetermined (maturity) date along with regular fixed interests or coupons.

#6 – Sneaky Debt

It is the most typical type of loan taken by middle-class families to furnish their homes with necessities. The infamous 0% interest rate may help finance nearly everything, including furniture, home appliances, and cell phones. While it appears to be an attractive offer, people should avoid it at all costs.

Examples of Debt

Let us consider the following two practical cases to get a better understanding of the concept:

Example #1

Alex has a small company that manufactures automobile batteries. One day he receives a fresh order for 10,000 batteries from a client. Alex promises to deliver the order by the end of the month. But when the production starts, Alex realizes that he will run short on working capital, raw materials, inventories, and other indirect expenses. Since the order is extensive, Alex cannot lose it. So he calls his friend Patricia and asks her to lend some money with the promise to return it on a particular date.

Patricia sees no harm in it and agrees without hesitation. They construct a legal contract in which Alex is the borrower, and Patricia is the lender. Alex receives the required funds from Patricia and fulfills the order. Upon receiving the final payment from his client, he returns the money borrowed to Patricia.

Example #2

In September 2021, the Institute of International Finance revealed that the COVID-19 pandemic pushed the global debt to a new high of $296 trillion in the second quarter. The organization looked at the household, business, bank, and government loans statistics from 61 countries. It also reported that emerging markets and developed economies, such as China, the United States, and European nations, witnessed significant growth in loan levels.

Advantages & Disadvantages

There are numerous benefits and drawbacks to debt that are as follows:

Advantages

- Many people start their businesses or take out personal loans to meet their necessities. If they are confident in their ability to repay the loan on time, they can maintain smooth ownership and control of their business or asset.

- Debt management of mortgages and student loans can help the borrower in paying their installments on time. Moreover, it will elevate their credit scores, increase their earning potential, help build their wealth, and provide them financial security.

- It gives the business the required money to close deals, fund projects, or start new ventures.

- It also lowers tax responsibilities for both individuals and companies.

Disadvantages

- Once a borrower has taken on a loan, they are obligated to repay it at some point. If they fail to repay, they may face legal action or lose the tangible property used as collateral.

- The interest rates on various loans are higher than typical, putting a burden on the borrower after a given period.

- Global events like natural disasters or financial crisis may make it hard for someone uncomfortable with money to repay the amount borrowed. As a result, it is preferable to avoid getting a loan until there is no other option.

- Failure of a business to repay interest owing to a drop in revenues may result in bankruptcy. Similarly, avoiding loans can cause it to miss out on potential business opportunities.

- The borrower may lose the collateral in case of defaulting on the loan.

- Having too many loans can make it difficult to obtain loans in the future.

- Personal, credit card and payday loans can be problematic owing to depreciation, reduced returns on investment, or higher interest rates.

Frequently Asked Questions (FAQs)

What are the four types of debt financing?

The four common types of debt are – secured, unsecured, revolving, and non-revolving. Credit card loans, school loans, personal loans, commercial loans, and mortgages fall under these categories. It is worth noting that unfavorable terms can turn a good loan into a bad one.

What is the most common source of debt?

Banks and financial institutions are the most popular source of getting loans. They offer a variety of options to anyone looking to finance their business, education, or personal requirements.

How many types of debt repayment methods are there?

There are three sorts of loan repayment methods: short-term, intermediate-term, and long-term. They differ in terms of the repayment period and the interest rates charged. Student and mortgage loans are examples of long-term loans.

Recommended Articles

This has been a guide to what is debt and its meaning. Here we discuss how debt in finance works along with the types and examples. You can learn more from the following articles –