Part of our Financial Planning guide

What Is Medical Debt?

Medical Debt refers to a financial obligation incurred by an individual due to unpaid bills for medical services obtained from a healthcare provider. The debt may be owed directly to a healthcare provider or a third-party agent, such as a collection agency, that bought the debt.

It can be a major part of the total debt for low- and middle-income households. Families with large healthcare bills have a hard time coping with it. Saving money and paying for necessities becomes difficult, making such families more dependent on credit cards and other debt-incurring payment methods. It hurts their credit, puts them off getting the necessary medical care, and may cause personal bankruptcy.

- Medical debt is a significant financial burden many individuals incur due to unexpected health-related expenses. Expenses that become debt are typically given to collection agencies. When bills remain unpaid for over 90 days, these agencies start their collection efforts.

- The payment of such dues is considered a simple or implicit contract. Hence, the statute of limitations, which may vary depending on the state, applies. Creditors trying to collect a past-due debt must file a lawsuit within six years. After this period, creditors and debt collectors do not have the right to file lawsuits in most cases.

- The Medical Debt Relief Act of 2021, also called the Medical Debt Forgiveness Act, was introduced to remove medical debt from credit reports.

Medical Debt Explained

Medical debt is a form of debt that accumulates due to health-related circumstances. It is often unpredictable and unexpected. It can be more harmful than other consumer debt because it is typically brought on by a sickness or accident that makes it difficult for an individual to work and impacts their ability or capacity to earn. Unlike discretionary expenditures on general consumer goods, healthcare is not optional because it is essential for well-being. People only use healthcare systems when necessary, and medical care is often unpredictable. Healthcare costs are generally high, and even those with insurance can face unexpected bills or gaps in coverage, leading to debt.

Medical debt is common when people have long-term or chronic conditions, and routine expenses are anticipated. However, any form of medical care, particularly diagnostic testing, hospital stays, ER visits, and outpatient services, can result in medical debt in the US. It is important to note that all kinds of medical costs are not covered by health insurance. Hence, out-of-pocket expenses like deductibles, coinsurance, and copays are applicable in certain cases.

Patients often lack clear information about the costs involved in seeking medical care, making it challenging to plan for both treatment and expenses. They may even receive one or more confusing and/or inaccurate medical bills from their insurance provider, doctor, or healthcare provider.

Insufficient insurance coverage, the unpredictability of medical emergencies, and high out-of-pocket expenses are three key factors that drive medical debt. Debt and a person’s relationship with it affect their physical and mental health. Studies have found that most people with medical debt put off getting essential care.

Medical debt, like general debt, can have a harmful influence on health. Consumer debtors struggling financially or trying to pay off their obligations are more likely to report reduced life satisfaction and increased worry. Medical debt, like income and wealth, is a social determinant of health, given its effect on access to healthcare and health outcomes.

Another point that needs consideration here is the increase in overall prices. Unpaid bills trigger bad debts, and eventually, these bills raise prices for the patient and the healthcare provider. As unpaid bills result in low revenue and high collection costs for healthcare service providers, their income is affected. To compensate for such risks, healthcare service providers increase their prices. Also, insurance premiums for patients with debt problems are usually high. Due to all this, healthcare costs rise for everyone—patients, healthcare providers, and insurance service providers.

What Happens If Left Unpaid?

The bills owed due to healthcare are often huge, and paying them off may be difficult. One thing every individual can do is to fully understand what they are getting into, including medical procedures, tests, and associated costs. Medical expenses that become debt are typically given to collection agencies. Once the amount is past 90 days, these agencies will attempt to collect it from the individual.

The agency will contact the individuals who owe them the money to confirm the amount, so being aware of the expenses is essential. Mistakes in recording amounts may occur at healthcare institutes; cross-verification can help one save some dollars.

Individuals can ask for repayment options if the balance is correct and payment is due. More often than not, the debt collector has the authority to grant a settlement, which helps individuals repay an amount lower than the amount they owe as full payment. Collection agencies may even offer individuals payment options that involve making nominal monthly payments until the balance is covered.

If the debts remain unpaid and are reported as such on the credit report, an individual’s credit score may be affected. The provider may also pursue legal ways to recover the amount, which includes filing a lawsuit. Per the statute of limitations applicable to medical debt, creditors can take legal action within a specific timeframe. However, since such debts are civil debts, jail time is typically not a consequence under normal circumstances.

Examples

Here are a few examples to take this discussion ahead.

Example #1

Janet visited the hospital due to some uneasiness, and it turns out she had a mild heart attack. Some tests were conducted, where further issues were identified. She underwent treatments, and medicines were prescribed. Due to this, she incurred some expenses not covered by her insurance.

She had no savings and was facing financial constraints. She could not afford this expenditure, leading to the bills not being paid on time. Therefore, the medical care provider decided to seek payment from Janet directly. They would have hired a debt collector, too, had Janet not paid off the debt a few weeks later. Had she not cleared her bills, the debt would have appeared on Janet’s credit history after 180 days.

Example #2

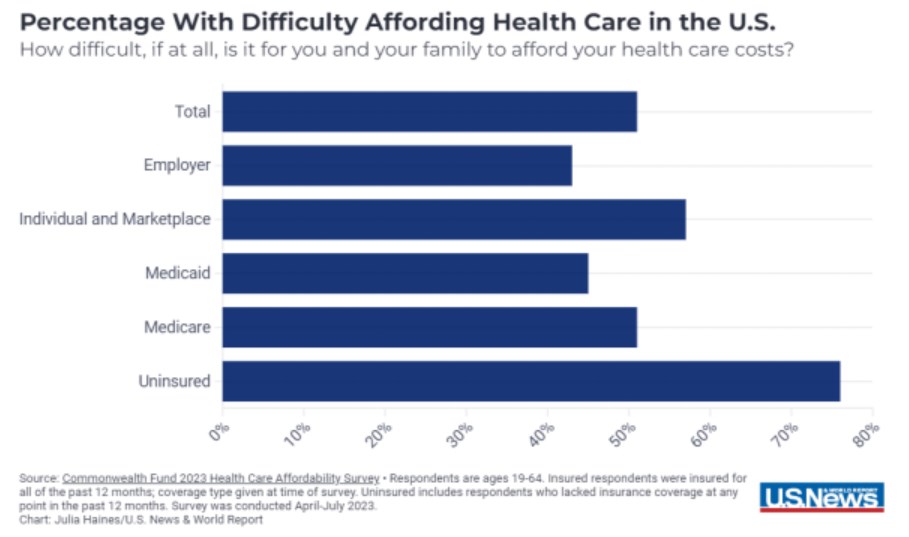

An October 2023 report states that 1 in 3 people in the US are currently shouldering hefty debts related to healthcare services, according to a survey. The news piece highlighted certain worrying figures related to the working population in the US, where half of them is dealing with a lack of adequate funds to meet medical expenses. It means more than half the population in the working age group is unable to allocate funds specifically for healthcare.

The survey titled the Health Care Affordability Survey by the Commonwealth Fund reflected the challenges that nearly 51% of the survey participants between the ages of 19 and 64 faced in terms of handling their health-related expenses.

Another prominent figure that came to light through this survey was the number of people who have Medicaid but still cannot afford medical care—around 45% of the participants. The following chart shows the many parameters against which financial well-being linked to medical expenses was measured.

Medical Debt Forgiveness

The Medical Debt Relief Act of 2021, termed the Medical Debt Forgiveness Act, aims to remove medical debt from credit reports. It helps individuals struggling with debt regain their financial balance. To facilitate this, the following provisions have been made available.

- When debt is incurred due to medical reasons, a consumer reporting agency is prohibited from including such debt as credit information in a consumer credit report if certain conditions are met. These are:

- The debt is fully repaid or

- It is less than a year old.

- Another key stipulation is that a debt collector must inform the consumer before reporting the medical debt to a consumer reporting agency.

How To Get Rid Of Medical Debt?

Financial assistance programs, also called Charity Care, give people who need assistance paying their medical expenses access to free or subsidized healthcare. Patients who do not have insurance and those who have insurance coverage but are underinsured may benefit from these services.

Medical providers, state governments, patient advocate groups, non-profit organizations, and disease-specific charities typically offer these programs to help people navigate these debts. The US government has come up with various solutions that can help individuals in distress; being aware of them and using them is important.

Apart from these solutions, individuals can take certain measures from their side to ease the situation, such as:

- Understanding the health insurance policy: It is important for individuals to understand the costs their insurance covers. They must also understand which costs are not covered and whether any waiting periods are applicable before they can benefit from insurance coverage. This can help people make sound decisions while seeking medical care.

- Setting up a payment plan: Medical bills can be sent to collections even if individuals make payments. The remaining bills may be forwarded to collection agencies if partial or regular payments are made after the due date. If an individual believes they cannot make payments regularly due to financial constraints, it is better to let the provider know. Service providers may be willing to help them find an alternative payment plan.

- Negotiating a discounted price: Some providers offer considerable discounts if individuals can pay and settle their accounts immediately, subject to the type and duration of payments.

- Other helpful options include:

- Avoiding credit cards that charge a high rate of interest while paying medical bills may reduce the debt burden.

- Consulting non-profit agencies such as the National Foundation for Credit Counseling to help with the bill is a worthwhile solution.

It is important to note that the medical debt statute of limitations generally places a six-year limit beyond which the matter cannot be taken to court. This period may vary from one state to another. In this context, the statute of limitations is the period within which creditors and debt collection entities can take legal action to settle pending bills. Once this period lapses, no legal action is possible.

Frequently Asked Questions (FAQs)

1.Do medical debts affect credit scores?

Usually, healthcare providers do not report to credit bureaus. However, they might give collection agencies control over unpaid bills, which could harm an individual’s credit score. If the debt is still listed as a negative item on the credit report, it will be deleted once the medical bills are paid in full.

2.How long can medical debt be collected?

Medical bills typically are considered simple or implicit contracts, so the six-year limit applies. Creditors trying to collect a past-due debt must file a lawsuit (known as an “action for account”) within six years of when the right of action accrues, failing which the claim is legally barred. The statute of limitations may vary from state to state, and specific laws may apply to specific cases.

3.Does medical debt have interest?

Interest is rarely charged on these debts, and medical credit cards often offer a temporary interest-free period of six to twelve months. However, a deferred interest rate may be charged, which might make credit cards expensive.

Recommended Articles

This article has been a guide to what is Medical Debt. Here, we explain it with its forgiveness, how to get rid of it, and examples. You may also take a look at the useful articles below –