Part of our Accounts Payable & Receivable guide

Debtor Meaning

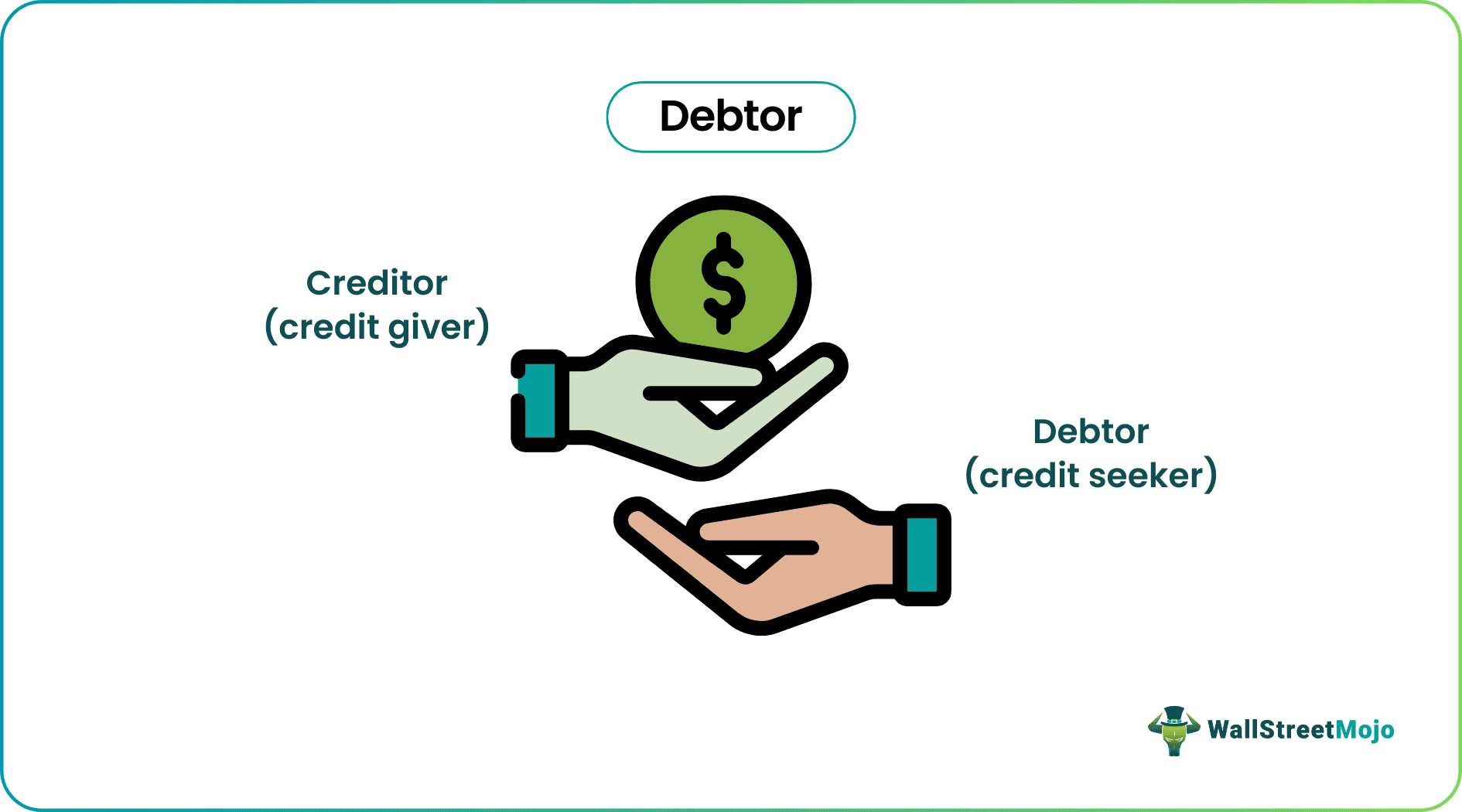

A debtor is a borrower who is liable to pay a certain sum to a credit supplier such as a bank, credit card company or goods supplier. The borrower could be an individual like a home loan seeker or a corporate body borrowing funds for business expansion.

Normally, borrowers must repay their debt along with additional interests to compensate the lender.

Key Takeaways

- A debtor is defined as an individual or firm that owes a particular amount to a lender, payable at a future date or period. A creditor is the supplier of a loan or credit facility and usually makes money out of interest on the debt.

- In accounting, a debtor is listed in the balance sheet under assets as it denotes a due revenue, which is an asset for a business.

- Fair Debt Collection Practices Act (FDCPA) is a law that prevents exploitation of the borrowers. Also, if a borrower becomes bankrupt or fails to repay the borrowed money, the lender can resort to a lawsuit, penalty or other legal action.

Debtor Explained

Debtors are common in business and everyday life. For example, if you have borrowed money from a bank to buy a house or study abroad, you are a debtor. The bank is the creditor as it has loaned the money. Other examples of debtors include businesses and governments that borrow funds to meet their financial requirements. Based on the debt type, lenders usually charge compensation for lending.

For example, if it is a loan, the lender will charge interest on the due amount. Here, the borrower must repay the loan along with interest. In addition, most loan lenders ask for collateral as a backup in case they fail to recover the debt. Conversely, when one buys goods on credit, there are often no interests involved as it is provided on the borrower’s reputation.

In debts, one must exercise caution while acquiring or extending a loan. Granted that borrowing money helps people and entities meet their financial needs. But it is not easy to seek loans as most institutions require a good credit score which is hard to arrange for many low-income groups.

Moreover, accumulating interests make repayments difficult for borrowers, putting financial constraints on them. Many times, people lose their collateral as well upon failing to repay the debt. Consequently, if a borrower fails to repay, the lender may lose the loaned amount, especially if the borrow files for bankruptcy. As such, one must deal in debts after thorough contemplations regarding their alternatives.

Debtor Examples

- Consumer loans – Borrowing money from banks or financial institutions to purchase a house, finance education, or for a trip abroad, etc.

- Business loans – Businesses borrow long and short term debts to meet operational requirements. Common long-term borrowing examples include bank loans, securities such as debentures and bonds, etc. In bonds, the issuer is the borrower. Short-term needs are fulfilled using facilities like bills of exchange, letters of credit, payday loans, etc.

- Entities – Likewise, entities like non-profit organizations, communities, etc., borrow money for different requirements.

- Government and nations – The government issue bonds such as a T-bond to raise funds from the public and finance its development activities. An important source of external borrowing for a nation is International Monetary Fund (IMF). Many nations borrow funds from the IMF and other countries to keep its economy running.

- Credit facility – Businesses acquire goods on credit from a supplier based on their reputation of making timely payments. Other credit facilities include credit cards, prepaid services such as prepaid electricity meters, prepaid taxis, etc.

Accounting of Debtor Account

Businesses often supply goods or services to a client in advance before receiving their payment. Therefore, in accounting, the client who owes money to a business for purchasing its goods or services on credit is recorded as a debtor account.

A debtor account is an asset as it denotes a pending revenue from a credit sale. Therefore, it is put under the debit side of accounting books, such as the balance sheet.

Debtor days is the number of days a company takes to recover cash from its credit sales. Too many account receivables and longer debtor days will affect a company’s availability of cash. In such cases, it won’t be easy to manage the company’s working capital requirements.

Types of Debt Interests with Calculations

We have discussed below the types of interests a debtor must pay along with the owed amount.

1. Repayment of debt without interest

Here, only the borrowed sum needs to be repaid as it does not accrue any interests. Examples include bills receivable by a company.

Calculation – George took a loan of $500 from his friend and promised to return the amount in a week. His friend did not charge any interest, and so George only repaid $500 after 6 days.

2. Repayment of debt with simple interest

When the borrower takes a loan at an interest chargeable with the simple interest method, the outstanding loan amount is evaluated as:

Due amount = Simple Interest (SI) + Principal

SI = (P×R×T)/100

Where A is the outstanding amount;

- P is the principal amount;

- R is the annual rate of interest; and

- T is the time converted in years.

Calculation – S borrowed $6000 from a bank at the rate of 10% per annum. The time period to repay the loan is 5 years; calculate the due amount using simple interest.

- SI = (6000 x 10 x 5) / 100 = $3000

- Due amount = $6000 + $3000 = $9000

3. Repayment of debt with compound interest

If the creditor allows credit to be repayable with a compound interest, the total amount due is computed as:

A = P (1 + r/100)^(t)

Where A is the outstanding amount;

- P is the principal amount;

- R is the annual rate of interest; and

- T is the time converted in years.

Calculation – T deposited a sum of $5000 in ABC bank. The bank promised to repay the sum after five years with a compound interest of 8% per annum.

What is the total outstanding amount payable by the bank after five years?

- A = [5000 (1 + 8/100) ^ 5]

- A = $7346.64

Thus, the total outstanding sum payable by the bank is $7346.64.

Debtor Prison and Legal Protection

Earlier, the US and UK had debtor prisons that imprisoned those who couldn’t repay their debts or were behind schedule. They were put behind bars even for the smallest amounts of debts. In the 19th Century, the prisons were banned and branded unconstitutional in the US. Yet, as per a 2020 study, over 3000 borrowers were issued an arrest warrant over payday loans, vehicle title, and other expensive lendings.

Debtor protection laws such as the Fair Debt Collection Practices Act (FDCPA) have been around for a while. Whenever unlawful imprisonment of debt holders surface, authorities take stricter actions to prevent such practices. The FDCPA also informs borrowers of their rights, what collectors can do and what they are prohibited against.

It also helps address the grievances of borrowers. Moreover, facilities like a debtor in possession financing allow borrowers to undertake business operations in a mortgaged building despite declaring bankruptcy. The idea is to continue functioning to pay off the debt eventually.

However, there are laws to safeguard creditors, too, especially with absconding borrowers or criminal offenders. An example is Nirav Modi’s alleged involvement in the $2.2 billion defrauding of a reputed Indian bank. The accused used illegal guarantees by rogue bank staff to raise credits from other banks and fled from the country.

Frequently Asked Questions (FAQs)

Who is a debtor and a creditor?

A debtor is a borrower of funds or a credit facility, and a creditor is the lender of funds who extends a credit facility.

Are debtors a current asset?

A debtor is a current asset recognized as accounts receivable for a company since the due amount will be received at a specific date in future using cash, kind or cheque.

What are sundry debtors?

They are the clients or customers who have taken the company’s delivery of goods or services but haven’t made an immediate payment. Instead, they promise to pay the due amount at a future date or period.

Is a customer a creditor or debtor?

The customers who make a credit purchase of products or services and don’t pay immediately for the same are considered the company’s borrowers, such as credit cardholders.

Recommended Articles

This has been a guide to Debtor and its definition. Here we discuss the meaning of debtors along with examples, advantages, disadvantages, and limitations. You can learn more about finance from the following articles –