What Is Payback Period?

Payback period can be defined as period of time required to recover its initial cost and expenses and cost of investment done for project to reach at time where there is no loss no profit i.e. breakeven point.

This is a method to check the viability of projects or investments. Here, if the payback period is longer, then the project does not have so much benefit. However, a shorter period will be more acceptable since the cost of the investment can be recovered within a short time. It is considered to be more economically efficient and its sustainability is considered to be more.

Payback Period Explained

The payback period is a metric in the field of finance that helps in assessing the time requirement for recovering the initial investment made in a project. It has a wide usage in the investment field to evaluate the viability of putting money in an opportunity after assessing the payback time horizon.

Every investor, be it individual or corporate will want to assess how long it will take for them to get back the initial capital. The shorter the period, the more favorable it is. This is because it is always worthwhile to invest in an opportunity in which there is enough net revenue to cover the initial cost.

Since the concept helps compute payback period with the breakeven point, the investor can easily plan their financial strategies further and make more decisions regarding the next step. It is calculated by dividing the investment made by the cash flow received every year. This is a valuable metric for fund managers and analysts who use it to determine the feasibility of an investment. However, it is to be noted that the method does not take into account time value of money.

source: Lifehacker.com.au

The above article notes that Tesla’s Powerwall is not economically viable for most people. As per the assumptions used in this article, Powerwall’s payback ranged from 17 years to 26 years. Considering Tesla’s warranty is only limited to 10 years, the payback period higher than 10 years is not idea.

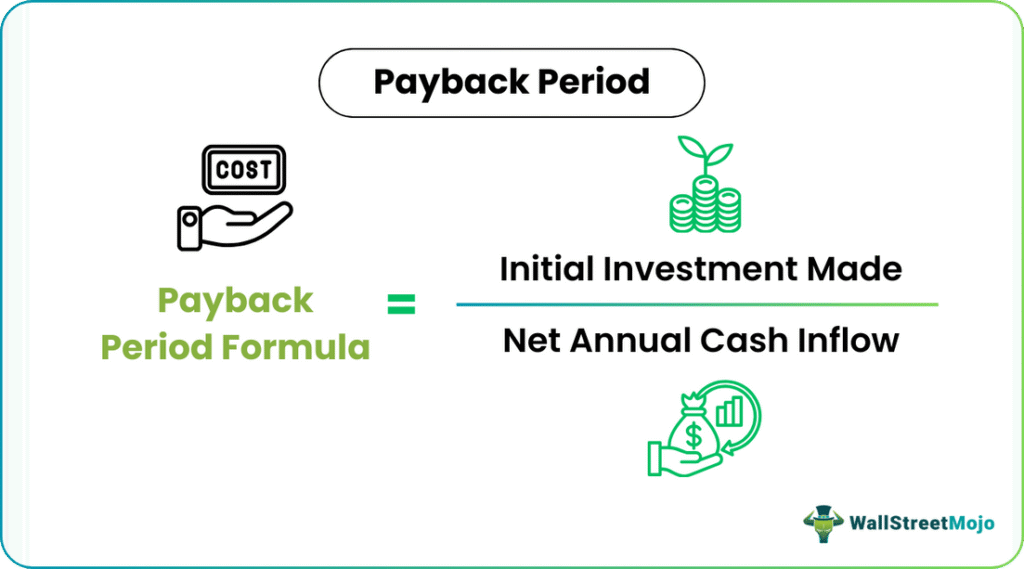

Formula

The payback period formula is one of the most popular formulas used by investors to know how long it would generally take to recoup their investments and is calculated as the ratio of the total initial investment made to the net cash inflows. The below mentioned formula helps to compute payback period.

Explanation of Payback Period in Video

How To Calculate

- The first step in calculating the payback period is determining the initial capital investment and

- The next step is calculating/estimating the annual expected after-tax net cash flows over the useful life of the investment.

#1-Calculation with Uniform cash flows

When cash flows are uniform over the useful life of the asset, then the calculation is made through the following payback period equation.

Payback period Formula = Total initial capital investment /Expected annual after-tax cash inflow.

#2- Calculation with Nonuniform cash flows

When cash flows are NOT uniform over the use full life of the asset, then the cumulative cash flow from operations must be calculated for each year. In this case, the payback period shall be the corresponding period when cumulative cash flows are equal to the initial cash outlay.

In case the sum does not match, then the period in which it lies should be identified. After that, we need to calculate the fraction of the year that is needed to complete the payback.

Examples

Let us understand the concept of how to calculate payback period with the help of some suitable examples.

Example#1

Suppose ABC ltd is analyzing a project which requires an investment of $2,00,000 and it is expected to generate cash flows as follows

| Year Annual cash inflows | |

|---|---|

| 1 | 80,000 |

| 2 | 60,000 |

| 3 | 60,000 |

| 4 | 20,000 |

In this cash payback period can be calculated as follows by calculating cumulative cashflows

| Year | Annual cash inflows | Cumulative Annual cash inflows | Payback period |

|---|---|---|---|

| 1 | 80,000 | 80,000 | |

| 2 | 60,000 | 1,40,000(80,000+60,000) | |

| 3 | 60,000 | 2,00,000(1,40,000+60,000) | In this Year 3 we got initial investment of $ 2,00,000 so this is the pay back year |

| 4 | 20,000 | 2,20,000(2,00,000+20,000) |

Suppose, in the above case, if the cash outlay is $2,05,000, then pa back period is

| Year | Annual cash inflows | Cumulative Annual cash inflows | Payback period |

|---|---|---|---|

| 1 | 80,000 | 80,000 | |

| 2 | 60,000 | 1,40,000(80,000+60,000) | |

| 3 | 60,000 | 2,00,000(1,40,000+60,000) | |

| 4 | 20,000 | 2,20,000(2,00,000+20,000) | The payback period is between 3 and 4 years |

For up to three years, a sum of $2,00,000 is recovered, the balance amount of $ 5,000($2,05,000-$2,00,000) is recovered in a fraction of the year, which is as follows.

Forgetting $20,000 additional cash flows, the project is taking complete 12 months. So for getting additional of $ 5,000($2,05,000-$2,00,000) it will take (5,000/20,000) 1/4th Year. i.e., 3 months.

So, the project payback period is 3 years 3 months.

Example#2

Let us see an example of how to calculate the payback period equation when cash flows are uniform over using the full life of the asset.

A project costs $2Mn and yields a profit of $30,000 after depreciation of 10% (straight line) but before tax of 30%. Lets us calculate payback period of the project.

Profit before tax $ 30,000

Less: Tax@30%(30000*30%) $ 9,000

Profit after tax $ 21,000

Add: Depreciation(2Mn*10%) $ 2,00,000

Total cash inflow $ 2,21000

While calculating cash inflow, generally, depreciation is added back as it does not result in cash out flow.

Payback Period Formula = Total initial capital investment /Expected annual after-tax cash inflow

= $ 20,00,000/$2,21000 = 9 Years(Approx)

Advantages

Some important advantages of the concept of payback period in excel are as follows:

- It is easy to calculate.

- It is easy to understand as it gives a quick estimate of the time needed for the company to get back the money it has invested in the project.

- The length of the project payback period helps in estimating the project risk. The longer the period, the riskier the project is. This is because the long-term predictions are less reliable.

- In the case of industries where there is a high obsolescence risk like the software industry or mobile phone industry, short payback periods often become determining a factor for investments.

Disadvantages

Here are some disadvantages of the method. Let us study them in detail.

The following are the disadvantages of the payback period.

- It ignores the time value of money

- It fails to consider the investment total profitability (i.e. it considers cash flows from the initiation of the project until the payback period and fails to consider the cash flows after that period.

- It may cause the company to place importance on projects which are short payback period, thereby ignoring the need to invest in long-term projects( i.e, A company cannot just determine project feasibility only based on the number of years in which it is going to give your return back, there are number of other factors which it does not consider)

- It does not take into account the social or environmental benefits in the calculation.

Thus, the above are some benefits and limitations of the concept of payback period in excel. It is important for players in the financial market to understand them clearly so that they can be used appropriately as and when required and get the benefit of it to the maximum possible extent.

Payback Reciprocal

Payback reciprocal is the reverse of the payback period, and it is calculated by using the following formula

Payback reciprocal = Annual average cash flow/Initial investment

For example, a project cost is $ 20,000, and annual cash flows are uniform at $4,000 per annum, and the life of the asset acquire is 5 years, then the payback period reciprocal will be as follows.

$ 4,000/20,000 = 20%

This 20% represents the rate of return the project or investment gives every year.

Payback Period Vs Return On Investment(ROI)

Both the above are important financial metrics used by analysts and investors to evaluate the profitability and viability of an investment. However, some differences between them are as follows;

- The former measures the time period whereas the latter measures the profitability of a project.

- The former measures how much time it will take for the initial investment to be recovered whereas the latter calulates the profit earning capacity compared to the cost of the opportunity.

- The former is focussed on the recovery whereas the latter is focussed on the return.

- The former takes into account the cash flows while making the calculation, but the latter takes into account the gains and losses from an investment.

- The former checks how much feasible a project is but the latter checks how well the resources are utilized.

Therefore the above points reflect the basic differences between the two financial concepts.

Payback Period Vs Discounted Payback Period

Both the above are financial metrics used for analysis and evaluation of projects and investment opportunities. But they differ in the technique used for calculation. Let us study the differences.

- The former is a method used to calculate how much time will be needed to recover the money invested in an opportunity initially. But the latter does the same using the discounted cash flow technique.

- The former does not account for the time value of money while the latter does so.

- Ideally, the time calculated by using the former is lower than the time calculated using the latter because the latter accounts for of calculates the current value of all the future cash flow.

- The investors and analysts prefer the latter to the former because of better clarity.

Thus, the above are some noteworthy differences between the two concepts.

Recommended Articles

Guide to what is Payback Period. We explain its formula, how to calculate, example, advantages, disadvantages & differences with ROI.