What Is Net Book Value?

Net book value refers to the net worth or the carrying value of the company’s assets as per its books of account, which is reported on its balance sheet. It is calculated by subtracting the accumulated depreciation from the original purchase price of the company’s asset. When a particular asset is discarded or retired, its net book value equation must be zero.

Net book value accounting is carried out to precisely evaluate the assets of an organization. It helps the accountant to determine the valuation of the organization and its cash flows. Moreover, finding an organization’s historical value of assets is made easier through this form of accounting. The book value of an asset can increase if the earnings through the asset are enormous.

- Netbook value, which appears on a company’s balance sheet, is the net worth or the carrying value of its assets according to its books of accounts. It is computed by deducting the asset’s total cumulative depreciation from its original purchase cost.

- The NBV of the company is the most popular financial metric used when valuing businesses. It accounts for all assets, including both real ones like buildings, equipment, and machinery and intangible ones like trademarks and copyrights.

- The calculation of book value is highly important since it necessitates adherence to applicable rules and standards; thus, there is a chance that the NBV of the asset needs to be estimated correctly.

- It serves as the foundation for reporting the data on the business’s balance sheet. However, the investor only uses these netbook value statistics to assess the possibility of growth. Therefore, before presenting such statistics in the financial accounts, the enterprises should concentrate on their accurate calculation.

Net Book Value Explained

Net book value is the cost of the asset at which the asset is purchased, including the asset’s purchase price plus all expenses incurred in making the asset ready to use, less the accumulated depreciation or any impairment losses. It is considered the most used financial measure for the valuation of the company, and the netbook value in most cases is different from the asset’s market value.

It is the base of reporting the figures on the balance sheet of the company. However, the investor primarily refers to these netbook value figures only for analyzing the growth potential. Hence, the companies should focus on the correct calculation of such figures before reporting them in the financial statements.

Below are a few significantly important points describing the functionalities and how to arrive at the net book value equation:

- The NBV of the asset keeps on changing, and generally, in the case of the fixed asset, it keeps on declining due to the effects of depreciation or depletion. At the end of the fixed asset’s useful life, the NBV of the fixed asset is equal to its salvage value approximately.

- Generally, the companies value their assets at cost or market price, whichever is lower. In case the market price of the asset is less than its cost, then the NBV of the asset has to be its market price. In such a case, the impairment of the asset is done, i.e., lowering the asset’s net book value to its market price, which leads to a sudden downfall in the asset’s value.

- The asset’s market price is different from its NBV at any point in time. As per the company’s policy, the asset is depreciated quickly or slowly. Suppose the company depreciates its asset using accelerated depreciation, i.e., allowing a higher deduction in the beginning years of the asset than in the initial years. In that case, the asset’s net book value will be less than its market value.

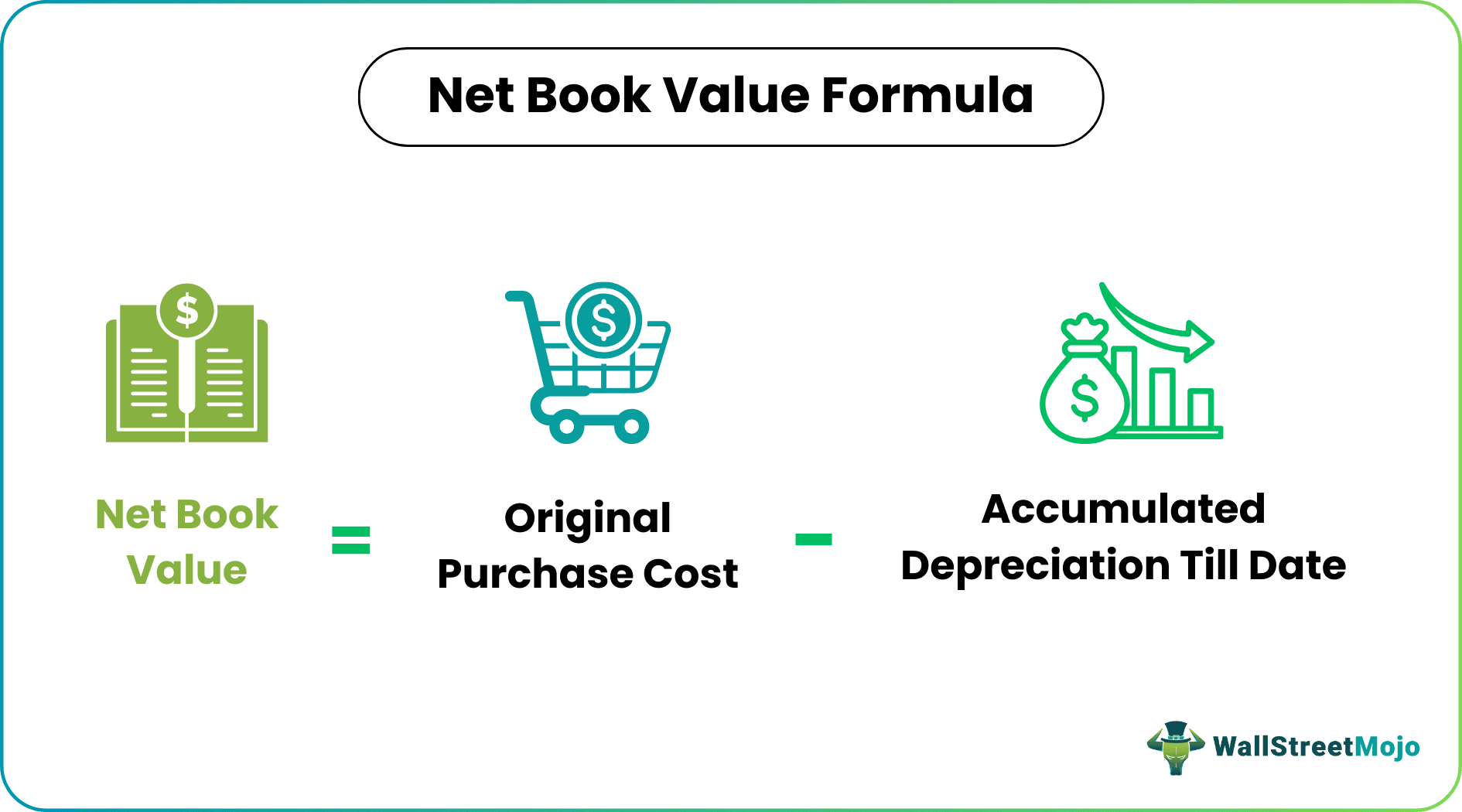

Formula

The formula used to calculate the net book value of the assets is as below:

Net Book Value formula = Original Purchase Cost – Accumulated Depreciation

- Original Purchase cost here means the purchase price of the asset paid at the time when the company purchased the assets.

- Accumulated depreciation here means total depreciation charged or accumulated by the company on its assets till the date of calculating the net book value of the asset.

Net Book Value Video Explanation

Calculation Example

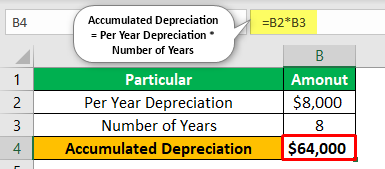

Let’s assume that the company Jack ltd purchased plant and machinery on January 1, 2011, worth $800,000, having a useful life of 10 years. The company has the policy to depreciate all assets annually using the straight-line method of depreciation. Calculate the asset’s net book value for the financial year ending on December 1, 2018.

Answer

For the company’s case, as given above, the asset’s purchase price was $800,000 on January 1, 2011. The asset’s useful life is ten years, and the company has the policy to depreciate all assets annually using the straight-line method of depreciation. So, we calculate the depreciation, which will be charged every year, by dividing the asset’s purchase price by the useful life of the asset.

In order to calculate the net book value, accumulated depreciation charged till the financial year ending on December 1, 2018, will be calculated for the 8 years.

So, the NBV of the asset at the end of the financial year 2018 that will be reported on the company’s balance sheet comes to $16,000.

Advantages & Disadvantages

Let us understand the fundamentals, functionalities, and applications that prove to be advantages or disadvantages through the discussion below:

Advantages

- The NBV of the company is the most used financial measure while valuing the companies and is measured for all the assets, whether they are tangible assets like buildings, plants & machinery, or intangible assets like a trademark, copyright, etc.

- At the time of liquidation of the company, the company’s valuation is based on its NBV of the assets, and it is the main base for measuring assets value.

- The net book value is used for calculating various financial ratios. These ratios, calculated using the net book value of an asset, help know the company’s market returns and stock market price.

Disadvantages

- The main disadvantage of the company’s net book value is that it is not the same as the market value of the company as it is the cost of an asset less accumulated depreciation and is generally far away from the market value, or maybe it can be close to the asset’s market value but generally never equals to the market value.

- It is considered while evaluating the growth of the company. Still, it is not a correct indicator for measuring the company’s growth prospects as the book value can be lower than the company’s earning potential.

- There is a possibility that the NBV of the asset is not calculated correctly as the calculation of the book value is very critical as it requires various compliances with applicable laws and standards. So deriving actual book values is sometimes difficult, and using them as a base for evaluation may lead to wrong decisions.

- This changes over time. Therefore relying completely on the NBV can make the asset valuation inappropriate.

Frequently Asked Question (FAQs)

How do book value and net book value differ?

The stock price of a specific firm is evaluated using book value per common share, also known as book value per equity of share or BVPS. In contrast, the equity holdings in a mutual or exchange-traded fund are evaluated using net asset value, or NAV (ETF).

What occurs when NAV is high?

Accordingly, a larger NAV indicates that the scheme’s investments have performed very well. Or the scheme has been in existence for a while. Only your potential number of units is affected by NAV.

Is an asset’s net book value a current one?

According to net book value, often known as book value, $60,000 of the noncurrent asset’s cost still needs to be deducted for depreciation. Therefore, other than fixed assets, noncurrent assets can also be referred to by the terms net book value or book value.

Should the NAV exceed the share price?

It is referred to as trading at a “premium” if the share price is higher than the NAV per share. It suggests that investors favor the trust and that there is a market for the shares. It is referred to as trading at a “discount” if the share price is less than the NAV per share.

Recommended Articles

This article has been a guide to What is Net Book Value. Here we explain its formula using a calculation example along with its advantages & disadvantages. You can learn more about it from the following articles –