What Is Straight Line Depreciation Method?

Straight Line Depreciation Method is one of the most popular methods of depreciation where the asset uniformly depreciates over its useful life, and the asset’s cost is evenly spread over its useful and functional life.

Straight Line Depreciation Formula Excel Template

Download Excel Template

Thus, the depreciation expense in the income statement remains the same for a particular asset over the period. As such, the income statement is expensed evenly, and so is the asset’s value on the balance sheet. The asset’s carrying amount on the balance sheet reduces by the same amount.

Straight Line Depreciation Method Explained

The straight line depreciation method is the process of allocating the cost and the asset over its entire working period in equal amount. A fixed percentage is charged on the initial cost of the asset every year. Therefore, the asset value reduces uniformly, finally reaching its scrap value at the end of the useful life.

This is a very widely used method, which is of course dependent on the type of the asset and the company rules and policies regarding accounting procedure. The calculation is done by deducting the salvage value from the cost of the asset divided by the number of years of useful life.

This straight line method for depreciation helps in allocating or spreading the cost throughout the life in order to find out what should be the probable worth of it after a time period. This is a very easy and involves less complex calculation, which makes it comprehensible for everyone. This process requires some actual data as well as some estimations, which directly involves the financial statements of the business.

There are various accounting softwares that help in calculating the same accurately and quickly. However, this process assumes that the fall in value is equal in all years, which may not always be practical. But it helps in budgeting and financial forcasting in a systematic manner.

Formula

Now let us see how to calculate straight line depreciation method. The straight-line depreciation method can be calculated using the following formula:

Depreciation Per Annum = (Cost of Asset – Salvage Cost) * Depreciation Rate

or

Depreciation Per Annum = (Cost of Asset – Salvage Cost) / Useful Life

The straight-line method of calculating straight-line depreciation has the following steps:

- Determine the initial cost of the asset at the time of purchasing.

- Determine the salvage value of the asset, i.e., the value at which the asset can be sold or disposed of after its useful life is over.

- Determine the useful or functional life of the asset

- Calculate the depreciation rate, i.e., 1/useful life

- Multiply the depreciation rate by the cost of the asset minus the salvage cost

The value we get after following the above straight-line method of depreciation steps is the depreciation expense, which is deducted from the income statement every year until the asset’s useful life.

Examples

Let us understand the concept of straight line method for depreciation with the help of a few suitable examples.

Example#1

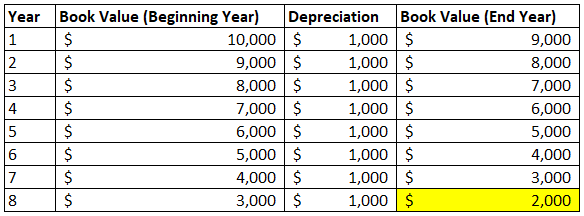

Suppose a business has bought a machine for $ 10,000. They have estimated the machine’s useful life to be eight years, with a salvage value of $ 2,000.

Now, as per the straight-line method of depreciation:

- Cost of the asset = $ 10,000

- Salvage Value = $ 2000

- Total Depreciation Cost = Cost of asset – Salvage Value = 10000 – 2000 = $ 8000

- The useful life of the asset = 8 years

Thus, annual depreciation cost = (Cost of asset – Salvage Cost)/Useful Life = 8000/8 = $ 1000

Hence, how to calculate straight line depreciation method the Company will depreciate the machine by $1000 annually for eight years.

- We can also calculate the depreciation rate, given the annual depreciation amount and the total depreciation amount, which is the annual depreciation amount/total depreciation amount.

- Hence, depreciation rate = (annual depreciation amount/total depreciation amount)*100 = (1000/8000)*100 = 12.5%

The depreciation account of the balance sheet will look like the below over the eight years of the machine’s life:

Example#2

source: Colgate SEC Filings

- Colgate follows the straight-line method of depreciation. Its assets include Land, building, machinery, and equipment; all are reported at costs.

- The useful life of machinery and equipment ranges from 3 to 15 years

- The useful life of the building is a bit longer than 40 years.

- Also, you should note that depreciation is not reported separately in Colgate. They are included in the Cost of Sales or Selling, general, and admin expenses.

Accounting

How do you adjust the depreciation charges on the Balance sheet, Income statement, and cash flow statement?

As seen from the above table – At the end of 8 years, i.e., after its useful life is over, the machine has depreciated to its salvage value.

Now, we will look into how this expense is charged on the Balance sheet, income statement, and cash flow statement. Let us take the above example of the machine to understand the straight line method depreciation schedule:

- When the machine is bought for $10000, the cash and cash equivalents are reduced by $ 10000 and moved to the Property, plant, and equipment line of the balance sheet.

- At the same time, the cash flow statement shows an outflow of $ 10000.

- Now, $ 1000 will be charged to the income statement as a depreciation expense for eight straight years. Although all the amount is paid for the machine at the time of purchase, the expense is charged over time.

- Every year $1000 is added to a contra account of the balance sheet, i.e., Property, plant, and equipment. It is called accumulated depreciation. This is to reduce any carrying value of the asset. Thus, after the 1st year, the accumulated depreciation will be $ 1000; after the 2nd year, it will be $ 2000; until the end of the 8th year, it will be $ 8000.

- After the machine’s useful life is over, the asset’s carrying value will be only $ 2000. The management will sell the asset, and if it is sold above the salvage value, a profit will be booked in the income statement, or else a loss if sold below the salvage value. The amount earned after selling the asset will be shown as the cash inflow in the cash flow statement, and the same will be entered in the cash and cash equivalents line of the balance sheet.

Advantages

Let us look at some of the advantages and disadvantages of the concept of straight line method depreciation schedule in a detailed way. The advantages are as follows:

- It is the simplest method of depreciating an asset. The asset is charged equally with the depreciation amount every year, making the entire calculation simple and easy to understand.

- It is the most commonly used and easy-to-understand method. Many companies use it to make the process less complex and this leads to easy understanding by the management as well other stakeholders.

- It does not involve complex calculations; hence, the chances of errors are less. The amount is easy to compute and depreciation is equally distributed among all accounting years in same amount. This reduce mistakes.

- Since the asset is uniformly depreciated, it does not cause the variation in the Profit or loss due to depreciation expenses. In contrast, other depreciation methods can impact Profit and Loss Statement variations.

- In this straight line method depreciation expense method the value of the asset can be written off completely since the amount is same every year. Finally, the value of the asset comes down to zero with no left-over scrap value at the ending of accounting life. Thus, this results in writing off the asset account completely.

- It is very suitable method in case there is a fixed life term for the asset. There are many such assets whose benefits can be derived for a fixed period. Straight line method is best in such cases.

Disadvantages

Some of the disadvantages of the concept of straight line method depreciation expense are given below:

- This method does not take into account any extra usage and wear and tear that take place. The amount is a fixed percentage of the original cost, distributed over the years equally each year.

- It does not account for the interest loss on the investment made on purchasing the asset. The business could have invested this interest amount somewhere else to earn a higher return, but this factor is not taken into consideration.

- Ideally as the time passes there is a lot of wear and tear of the asset which should result in higher depreciation over the years. But this fact is totally ignored in this calculation. In the initial years, the total cost of maintenance is less and the asset is in good condition, which means less depreciation. But later years this amount rises, which should be correctly adjusted to get a fair value of the asset.

- It is not an easy task to determine the scrap amount of the asset after many years from the date in which it ihas started its work.

Thus, the above are some of its advantages and disadvantages. It is upon the accounting method followed by the company and also the type of asset that has to be depreciated. In the article, we have seen how the straight-line depreciation method can depreciate the asset’s value over the useful life of the asset. It is the easiest and simplest method of depreciation, where the asset’s cost is depreciated uniformly over its useful life.

Straight Line Depreciation Video

Recommended Articles

This article has been a guide to what is Straight Line Depreciation Method. We explain its formula, along with examples, accounting, advantages & disadvantages. In this, we discuss the Straight-line method along with practical examples (Colgate) and its impact on the Income Statement, Balance Sheet, and Cash Flows. You may also learn more about basic accounting from the following articles –