What is the Lower of Cost or Market Rule?

Lower cost or market (LCM) is the conservative way through which the inventories are reported in the books of accounts, which states that the inventory at the end of the reporting period is to be recorded at the original cost or the current market price of the inventory, whichever is lower.

It simply means that the carrying amount of inventories on the balance sheet should be written down if the reported inventory value exceeds the market value.

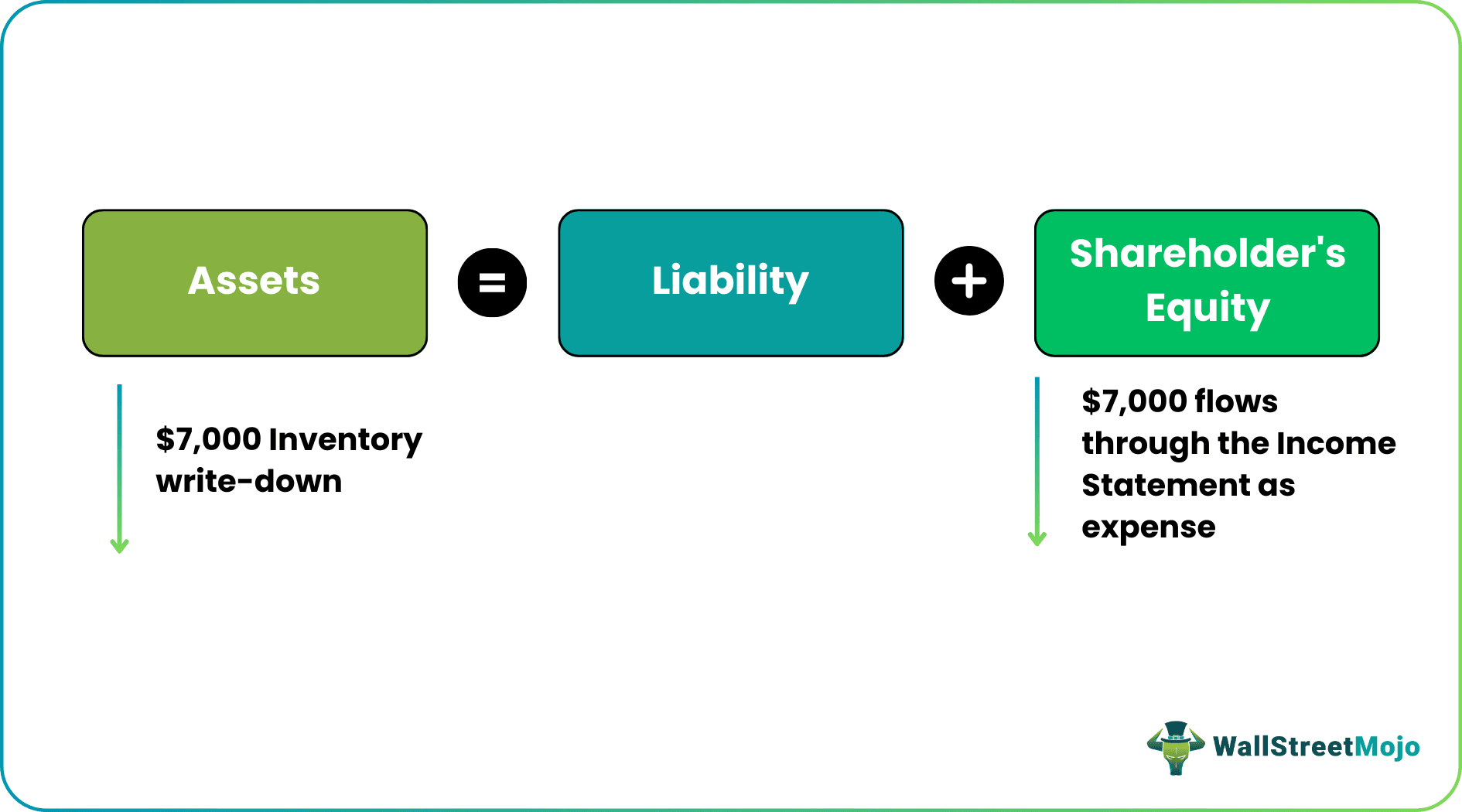

Such adjustment to inventory value affects the financial statements –

- Inventory Write down to the current market value reduces the inventory and total assets.

- Inventory Write-down comes as an expense in the income statement.

- When the inventory value rises, the gains are ignored, and inventory is valued at cost.

Let us take a simple example –

- Assume that a company has inventory on its balance sheet at $55,000, and the management learns that the inventory’s replacement cost is $48,000.

- As per the LCM method, management writes inventories down to a balance of $48,000.

- We note that the inventory write-down of $7000 reduces the Asset Size.

- The write-down reduces the net profit by $7000 (assuming no taxes).

- This reduced net profit reduces the Shareholders Equity (as it flows through retained earnings).

Inventory Valuation Using Lower Cost or Market Rule

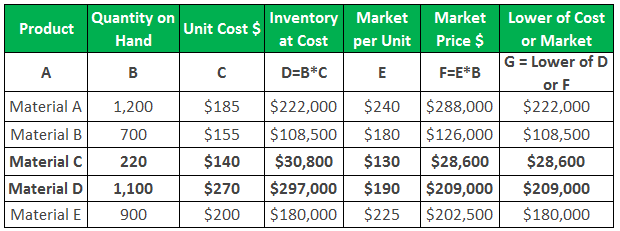

Let us understand in the below table how we should take the stock price of any product: For materials A, B & E, the cost price is lower than the Market price, so we have taken the cost price as the stock price. For material C & ED, the cost price is higher than the Market price, so we have taken the Market price as the stock price.

It is very important to analyze the reasoning behind this accounting policy. The accounting policies globally state that revenue or gains should be shown in the books when there is a high certainty of realizing it. However, all the foreseeable expenses or losses should be accounted for immediately. The lower cost or market price policy follows this closely.

The stock can be in the form of raw material inventory, work in progress inventory, and finished well. It is widely known as Closing Stock/Inventory. The closing stock is shown as an asset in the Trial balance, and while preparing financial statements, the closing stock is shown on the credit side of the Profit & Loss and asset side of the Balance sheet.

Examples of Lower Cost or Market Price Rule

Let us understand the following examples:

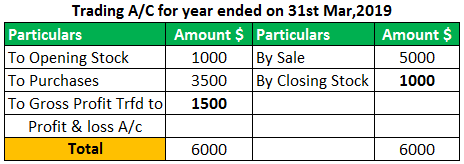

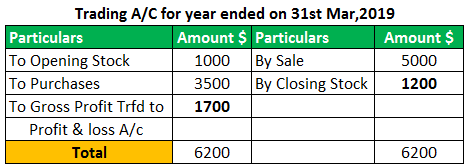

Consider Cost Price $1000 and Market Price $1200.

Example #1

In this case, when stock is valued at a cost price of $1000, Gross Profit is $1500:

Example #2

In this case, when the stock is valued at a Market price of $1200, Gross Profit is $1700:

For example, 1, when we have valued stock at a lower cost or a Market Price of $1000, the Gross Profit is $1500, whereas in example 2, when we have valued stock at a higher cost or a Market Price of $1200 the Gross Profit is $1700. In the second example, just because the stock is valued at a high price, the profit increases by $200.The organization will pay taxes and comply with other statutory obligations on this amount.

Even if we say that at some point, the organization will realize this $200, it is only going to be in the next accounting period, and that is where it should be shown as sales. Showing stock at a Market price of $1200 also goes against the periodicity concept where we are showing revenue in one period and realizing it in another.

Note: $200 is not yet realized by the organization.

Advantages

Some of the advantages of lower cost are as follows:

- Lower of cost follow the periodicity and conservatism concept of accounting.

- It allows for more expensive items to be absorbed.

- Lower cost saves an organization from paying extra taxes.

- Inventory valuation can be used as collateral for short term loans.

- Inventory valuation is also useful at the time of business sell-off.

Limitations

Some of the limitations of lower cost are as follows:

- Lower cost ignores the time factor, leading to over or understating profit.

- The selection of the correct method of valuation is always a complicated process.

- Any change is the valuation method must be informed to auditors and regulatory bodies.

- Stock counting and physical verification of stock are time-consuming processes.

Points to Note

- You need to analyze if a change is short or long-term.

- The valuation method leads to a change in inventory value – it should be consistent with prior years.

- Any loss in value should be accounted for immediately.

- Any gain should not be accounted for unless realized or has a certainty of realization.

Conclusion

Lower of cost or market (LCM) is a method of inventory valuation. It helps in reporting the true and fair view of the financial statements of any organization to all the stakeholders. This accounting standard policy should be followed diligently to avoid any discrepancy in the audit process and reporting of financial statements.

Recommended Articles

This article has been a guide to the Lower Cost or Market. Here we discuss the LCM Accounting Rule along with practical examples, advantages, and disadvantages. You can learn more about accounting from the following articles –