What Is Book Value Of Debt?

The book value of debt is the total amount the company owes, which is recorded in the company’s books. It is used in Liquidity ratios, where it will be compared to the total assets to check if the organization has enough support to overcome its debt. This Book value can be found in the Balance Sheet under Long Term Liability and Current liability head.

It is updated quarterly or annually with the company’s financial statement, so only after a quarter or annual financial statement reporting would the investor be aware of how the company’s book value has changed over the time. Howevr, It may be different than the market value of the firm

Book Value Of Debt Explained

Book value of debt is the total money that the company owes and records in its books. It represents the total amount that the business has taken as a loan from stakeholders, is liable to pay back to them, and is reported in the financial statement. For businesses in construction, partnering with VA construction loan lenders can play a significant role in managing such liabilities effectively. The book value is stated as per the historical cost of the debt value.

It is one of the things to look at when we are investing or loaning the money in any company. Yet, it is not an accurate way to calculate the total net debt of the company. We have to consider the market value of debt for a proper understanding of the company.

It is the sum of Long-term debt, the Current portion of long-term debt, and notes payable on the balance sheet. . In the liability side of the balance sheet, the total value of the company’s debt obligation is stated, which includes the short term and long-term debt, notes payable, etc. The sum total represents the book value or book value of total debt and it is useful to calculate the company’s liquidity ratios to see if the organization can support its debt load.

It is useful for financial accounting or reporting purpose and helps in interpreting the capital structure and financial condition of the business. However, other factors are also involved in assessing the true value of the debt and the analysts and investors who successfully invest in opportunities giving good return always evaluate the book value of this liability in combination with other factors.

Book Value, Face Value & Market Value – Video Explanation

Components

It consists of the following components in the balance sheet related to book value of total debt.

- Long term Debt, will be found in the long-term liability head in the balance sheet.

- Current portion of Long-term Debt, will be part of the Current liability head in the balance sheet.

- Promissory Notes (Note Payable), it would be found in the current liability head in the balance sheet.

Formula

Below is the formula to calculate the Book Value of the Debt

Book Value of Debt formula = Long Term Debt + Notes Payable + Current Portion of Long-Term Debt

From the above formula we can successfully calculate the book value of debt on balance sheet which is extremely useful for analysts and investors while making investment decisions.

How To Calculate?

It is calculated to make a sum of money borrowed and is due to be paid on the Balance sheet. All we need to do is add all the long-term Liabilities and some of the components in the Current Liabilities.

Long-term Liabilities include Long term loans from Banks or other financial institutions and Debentures. From the balance sheet, one can easily calculate this Book value.

Example

let’s take one example.

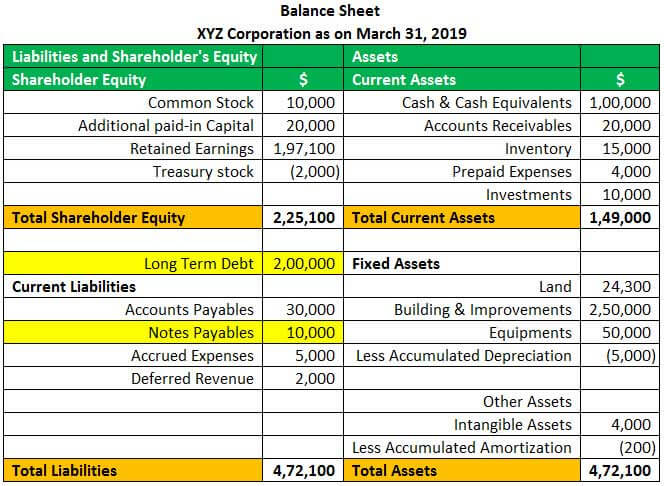

Below is the balance sheet of M/s XYZ Corporation as of March 31st, 2019. We will look at the liabilities side to find out the total debt in the company to understand the book value of debt on balance.

We can see in the above balance sheet of M/s XYZ Corporation that the Total long-term Debt is $200,000, and Notes Payables are $10,000.

The next step is to calculate the book value of debt by employing the above formula,

- Book Value of Debt = Long Term Debt + Notes Payable + Current Portion of Long-Term Debt

- =USD $ 200,000 + USD $ 0 + USD $ 10,000

- = USD $ 210,000

So, we can see that the Debt for XYZ Corporation is $210,000, which would be different from the market value of debt.

Advantages

It has many advantages as compared to any other method of valuation of Debt. Below are the main advantages one can see with it.

- Easy to Calculate: It is easy to calculate; as per the above formula, we can calculate it by looking at the company’s balance sheet. We have to add all book value of long term debt and current liabilities, which will give the Book value of the Debt.

- It gives us the actual value of debt that a company owes to its lenders or other stakeholders, which is recorded in the books.

- This book value of long term debt changes only when the company updates its financial statements quarterly or annually, and it does not change as per the market situations.

Disadvantages

As we have seen some of the advantages, this has some disadvantages as well; some of them are as follows:

- The book value of Debt is not so accurate when compared with the Market value of Debt. It is derived directly from the financial statements, so it is not affected by current market situations or interest rates.

- It changes over periodical intervals, i.e., monthly, quarterly, or annually. If someone wants to know the current book value of Debt, he has to wait for updated financial statements.

- Book value of debt is the accounting value of the debt, which was recorded as per the historical data or amortization schedule of the debt, which will have less relevance at the time when the company is looking for a merger or acquisition or looking for any other external investors for the company.

- One of the major issues with the Book value of Debt is that all financial statements are updated quarterly or annually. If one wants to see the exact amount of debt from the financial statement, one has to wait for the company’s quarterly or annual financial statements from the company.

- It would be adjusted per the accounting standards and subject to adjustment, which is difficult to understand and track.

- It does not give the exact position of the net debt that the company would have actually. To get the exact position of the net debt, we have to consider the market value of Debt.

- It could be used for empirical finance only as it does not consider the current market situations and interest rates for calculating a net debt for the company.

- It does not help stakeholders and investors calculate the company’s total Enterprise Value.

- The book value of debt is accounted for in the financial statements based on the amortization schedule of the debt or historical cost.

Thus, the above are some limitations of the Book Value of Debt which should be considered equally along with the advantages, while making the financial analysis, so as to take informed decisions regarding the investments.

Effect Of Changes In Book Value Of Debt

It is the sum of the total debt recorded in its balance sheet and is useful in calculating the firm’s liquidity ratios. So changes in the book value of Debt will affect in the following manner,

- Changes in this Book value will affect its liquidity ratios. Liquidity ratios are useful in knowing the firm’s capability to support its total debt.

- Suppose the Book value of debt has increased over time. In that case, the company’s capability has decreased to support its total debt, which means that compared to its total assets, the company has more debt on its balance sheet. It would be difficult for the company to pay off its debt in the future.

- The company has to put its assets as collateral with the banks or other financial institutes, so changes in this book value will also affect the value of the collateral securities with the banks or other financial institutes.

Book Value Of Debt Vs Market Value Of Debt

Both the above methods are two different ways to identify and measure the value of loan of the business. However, there are some important differences between them as follows:

- The former shows the value of the debt of a business as per the books of accounts or the financial statements but the latter show the current price of the loand in the market if they were to be purchased or sold in the open market.

- The former does not always show or reflect the current market value or the perception of the market regarding the debts, but the latter is the market value by itself.

- The market value takes into account the credit worthiness, the interest rate changes and change in market condition which is not accounted for when we calculate book value of debt. The book value records the loans as per the historical cost.

- The book value will not fluctuate since it is based on the original value of the debts whereas since the market value refelects the current price of the loans, there is a possibility of fluctuation or changes over time, which can make it significantly different from book value.

- Market value is generally considered to be a more relevant measure of the loan compared to when we calculate book value of debt since it reflects the true economic value.

- Market value gives a more realistic picture of the company’s debt as compared to book value and shows the true financial position.

- Book value can be obtained easily from the financial statements of the business, but the market value has to be obtained by accessing different market data, using various models for calculation which is tedious and time consuming.

Thus, the above are some basic differences between the two methods of assessment of loan value, each having their own uses and limitations. Which method will be used depends on the context for which the data will be used and who is the user of it.

Recommended Articles

This has been a guide to what is Book Value Of Debt. We explain it with formula, differences with market value of debt, how to calculate, component & example. You can learn more about financing from the following articles –