Useful Life Definition

Useful life is the estimated period for which the asset is expected to be functional and can be used for the company’s core operations and serves as an important input for calculating depreciation for assets which affects the profitability and carrying value of the assets.

Useful life is an estimation and the actual life of the asset, maybe even more, or it can be less. It has to be considered after proper evaluation and considering all the factors. It is regarded as a critical element in asset recording and valuation as the depreciation and carrying value of the asset depends on it, and it has a direct impact on profitability. It can always be revised considering the present technology, obsolete assets, higher usage, etc.

Key Takeaways

- Useful life is the estimated time frame when the asset is anticipated to be operational and usable for the company’s primary operations.

- It is a crucial input for calculating asset depreciation, which impacts the assets’ profitability and carrying value.

- Although the asset may last longer than expected, the upkeep cost will rise significantly. In addition, significant repairs may need to be made as the asset ages and becomes obsolete.

- The asset can last longer than its useful life, but the costs of maintaining the assets will rise at a particular point.

Useful Life Explained

The useful life of assets is the estimated number of years an asset can provide helpful service to a company to generate revenue through optimum use of resources and minimum cost. This is also a method to estimate the time period during which the asset’s depreciation will occur.

Every asset has its period of usability, after which it cannot be used, or it will be obsolete. The useful life of investments will vary according to their nature, asset usage, company replacement policy, etc.

Estimations are available based on the nature of the asset provided by the accounting body. Therefore, the company can adopt the same for their purchases or make their assessment based on the proper asset valuation. The estimation of useful life depends on how much it is being used in the organization and for what kind of process, for how long it is being used starting from the date of purchase, and how much advancement of technology has taken place.

Thus it is the duration of the measurement of how much useful and for how long it is useful to the organization. It is used to calculate the depreciation for the entire time period. Sometimes the entity may calculate a greater depreciation value during the beginning of the useful life of assets and towards the end it considers lesser depreciation. However, it is clear that this method is an important component in the business.

Factors To Consider

It estimates a period until which the asset can be put to use, and it contributes to generating revenue. The following are the factors considered in determining remaining useful life –

- Usage of the Asset – If the usage of the asset is more, then the useful life of the asset will reduce due to wear and tear, and it will deteriorate rapidly.

- A newly procured asset will last longer than an already used asset since the same is already being put to use.

- When there are technological advancements, the asset will become obsolete as the same will no longer match the requirements of the current market.

- Any legal restriction or any limits for the usage of the asset;

- The asset may last longer than its estimated useful life, but the cost of maintenance of assets will considerably go high after a point in time. Over time the asset may become obsolete, and significant repairs can happen. It is determined based on how long the asset can be used before replacement.

Formula

Let us understand the formula that is used to calculate the remaining useful life.

Impact On Depreciation

- Useful life for depreciation is the estimated life of a depreciable asset until it can be used for revenue-generating operations. It directly impacts depreciation expense as depreciation is calculated based on years of assets life. More it is, the less the depreciation will be and vice versa.

- Any change in it will alter the depreciation expense, and it will impact the profitability of the business. If depreciation is more, the profitability will reduce. However, depreciation is a non-cash expenditure, so the same will affect the business’s cash flow.

- Depreciation will be considered only when the asset’s life is more than a year. E.g., building, vehicles, etc. When an asset is procured, the entire cost is not expensed off as the same is capitalized, and it is depreciated over its useful life.

Examples

Below are the examples to understand the concept of useful life of equipment in a better manner –

E.g., .#1

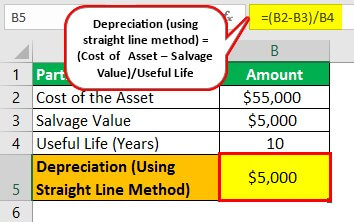

X Corp purchased a vehicle to transport its goods from its factory to the warehouse. The cost of the vehicle is $55,000, its expected useful life is ten years, and the salvage value is $5,000.

Solution

Calculation of depreciation will be as follows,

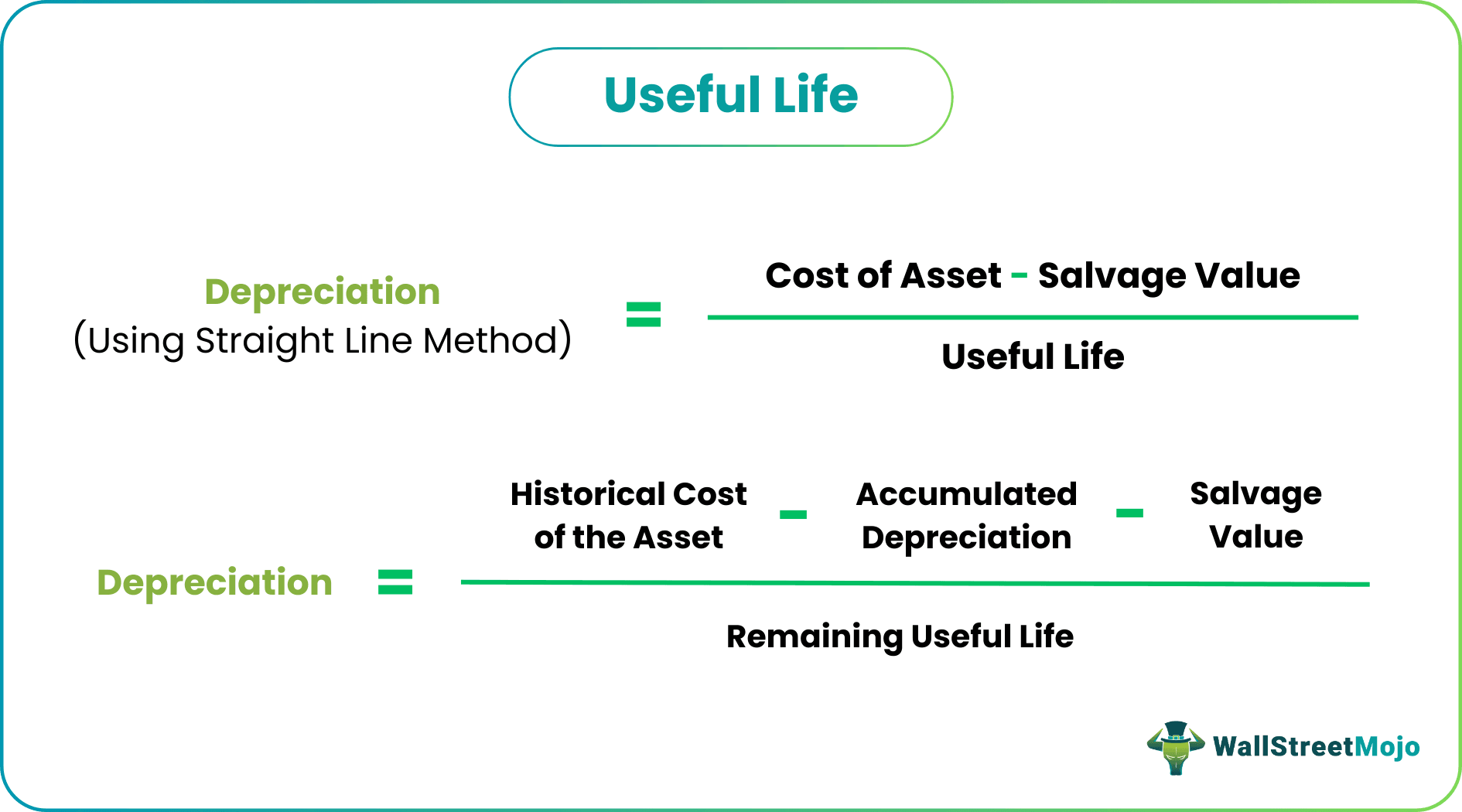

Depreciation under straight-line method = (Cost of the asset – salvage value)/ Useful life

- = ($55,000 -$5,000)/10

- = $5,000 per annum

So the impact of profitability on account of depreciation is $5,000 Per annum.

E.g., .#2

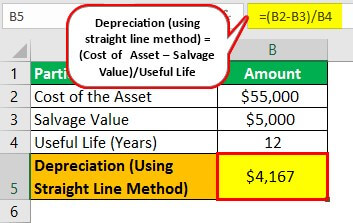

In case the company estimates the vehicle’s useful life as 12 years with the same salvage value. So the revised depreciation calculation will be as follows:

Solution

Calculation of depreciation will be as follows,

Depreciation under straight-line method = ($55,000 – $5,000)/ 12

- Depreciation = $4,167 per annum.

So the impact on profitability will be $4,167 Per annum. So there is an improvement in profitability to $833 per annum.

Change in an asset’s life or any revision is done prospectively and reported no of earlier years need not be changed. The prior period reported values need not be changed as it is not an accounting error, and it is an estimation; change in it is an inherent element.

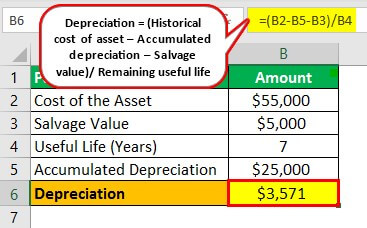

E.g., #3

Suppose the revision of its useful life for depreciation is done at the end of the 5th year, in the above case. The depreciation is already provided for five years as per 10 yrs. The depreciation provided is $25,000 ($5,000 Per Annum* 5 yrs). The book value of a vehicle will be $30,000 since life is revised as 12 years (i.e.) another 7 yrs instead of 5 yrs.

Solution

Calculation of depreciation will be as follows –

Depreciation = (Historical cost of the asset – Accumulated depreciation – Salvage value)/ Remaining useful life

- = ($55,000 – $25,000 – $5000)/7

- = $3571 per annum.

The above depreciation is a non-cash expenditure, the cash outflow happens at the time of purchase of a vehicle, and there won’t be any yearly impact.

It is an allowable expense for tax depreciation, but the method of computation of depreciation is an accelerated method.

Useful Life Vs Physical Life

- Useful life of equipment is the period until which an asset is effectively used in operations. In contrast, physical life is the period until the asset will be in physical form and after which it has no salvage value.

- The asset’s physical life can only be known after its life ends, whereas useful life will be determined even before the asset is put to use based on its usage, nature, and other factors. There can be many factors that make an asset unusable economically, but it will be physically available.

Frequently Asked Questions (FAQs)

What does an asset’s useful life change mean?

A change in an asset’s useful life refers to a change in the estimated period over which an investment is expected to provide economic benefit to its owner.

What is the useful life of rental property?

The useful life of the rental property is the estimated period that the property is expected to generate rental income and benefit its owner before it becomes obsolete or requires significant renovations.

Who determines the useful life of an asset?

The useful life of an asset is usually determined by the company or organization that owns the asset. The company will consider various factors while deciding the valuable life of an asset, such as the expected physical wear and tear of the investment, the level of maintenance required, and changes in technology.

Recommended Articles

This article has guide to Useful Life and its definition. We explain it with formula, example, factors to consider, impact on depreciation. You may learn more about financing from the following articles –