Part of our Income Statement guide

What Is Non-Operating Income?

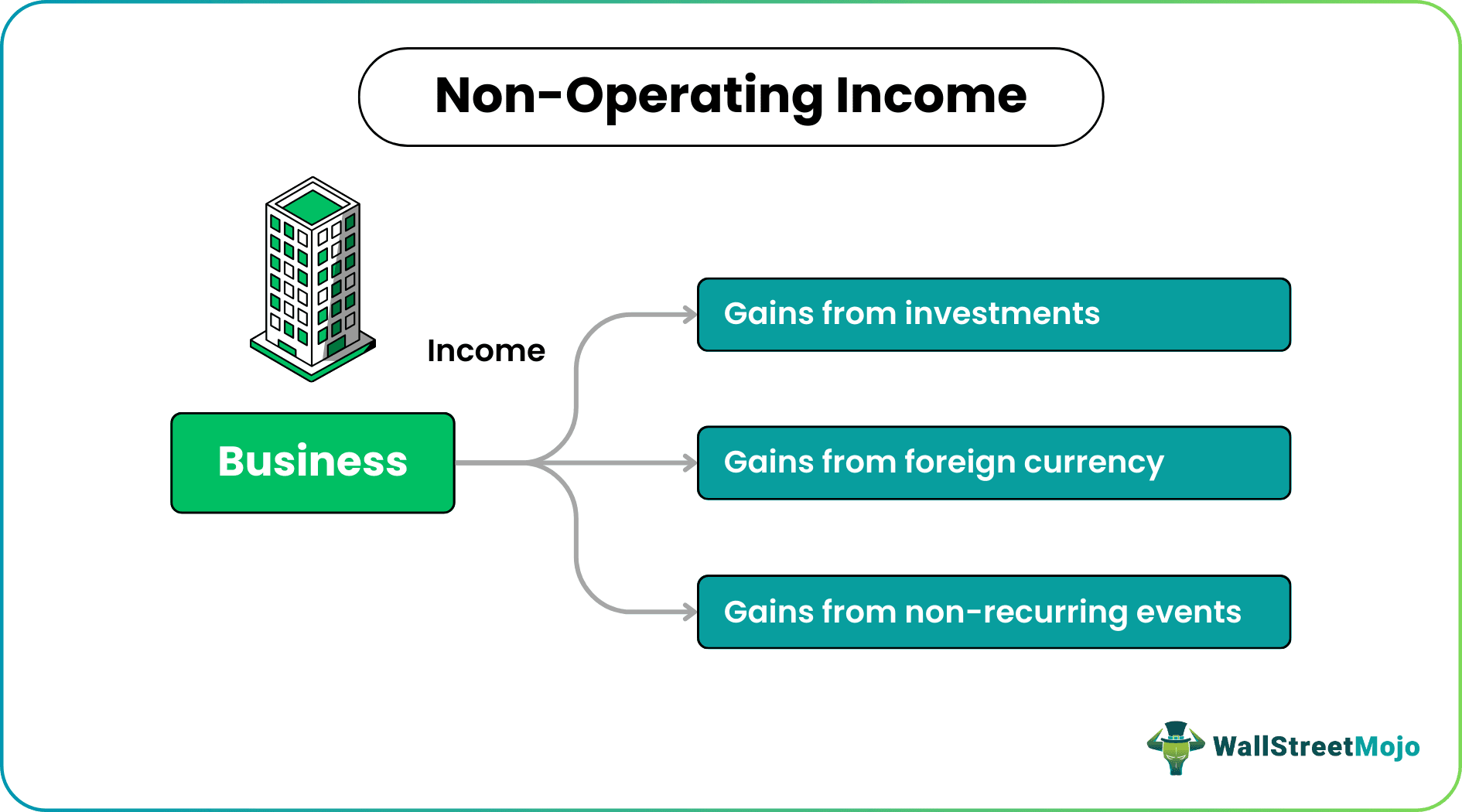

Non-operating income is the income earned by a business organization from the activities other than its principal revenue-generating activity. Thus, it is the income stream on the entity’s income statement driven by activities that do not fall under the core business operations of the entity.

This type of non-core income stream may take many forms like gains or losses due to fluctuation in foreign exchange, asset impairments or write-downs, income from dividends arising out of investment in associates, capital gains and losses from investments, etc. It is also known by the name peripheral or incidental income.

Non-Operating Income Explained

The net non operating income are the ones that the entity earns from sources other than the main business activities of the organization. Some examples include profits/loss from the sale of a capital asset or foreign exchange transactions, income from dividends, profits, or other income generated from the investments of the business, etc. Thus, they are not attributable to the main operation.

They do not occur frequently or regularly and so they are not used to measure how much successful a business it. They are also known as incidental or peripheral income. They also depend on the type of business. Both experience sudden ups and downs as operating performance tends to remain more or less the same for stable companies. It appears at the bottom of the income statement, after the operating profit line item.The net non operating income and expenses are likely to be one-time events such as loss due to asset impairment.

Some non-operating items are recurring in nature but are still considered non-operating as they do not form the core business activities of the entity.

List Of Non-Operating Income

Dividend income arising due to investment into associates

Gains due to investment in financial securities

Gains due to transactions in foreign currency and hence are affected by fluctuations in foreign exchange rates

Any gains which may be a one-time non-recurring event

Any gains which are recurring but non-operating

Revenue vs Income Explained in Video

Formula

Let us look at how to calculate non operating income. It is usually shown as a “Net Non-Operating Income or Expense” at the bottom of the income statement. Most of the time, it appears after the “Operating Profit” line item.

It can be calculated, as shown below:

Net Non-Operating Income

= Dividend Income

– Losses due to asset impairment

+/- Gains and Losses realized after selling the investment in financial securities

+/- Gains and Losses due to transactions in foreign currency

+/- Gains and Losses due to non-recurring one-time events

+/- Gains and Losses due to recurring but non-operating events

It may not have some fixed formula as it is more dependent upon the classification of the line item as operating or non-operating activity.

The calculation can also be done by –

Net Operating Income = Net Profit – Operating Profit – Net Interest Expense + Income Tax.

This is a back-calculation to decipher the value of non-operating income and expenses from the entity’s income statement. Some companies report such income and expenses under a different head. Thus, the above is the non operating income formula.

Examples

Let’s look at some examples to understand how to calculate non operating income.

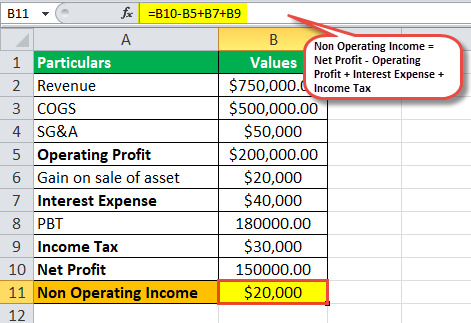

Example #1

Let’s assume a fictitious company ABC with an income statement as shown below:

Now in order to calculate the non-operating income from the above income statement, we can follow the back-calculation approach as follows:

Net-Operating Income = $150,000 – $200,000 + $40,000 + $30,000

= $20,000

Now, if we look closely at the income statement shown above, it is quite obvious to point at the non-operating line item, i.e., Gain on sale of the asset. But to come to this line item’s value based on some formula, we used a back-calculation formula, which gives the same value as for the Gain on the sale of assets.

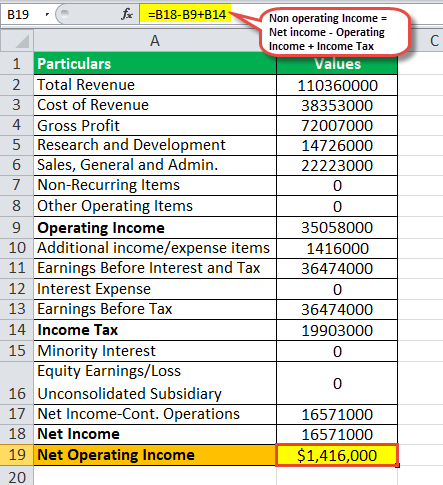

Example #2

Now let’s look at a real-life income statement of Microsoft.

= $16,571,000 – $35,058,000+ $19,903,000

=$1,416,000

The above formula helps us to find out non operating income.

Advantages

- Non-operating income estimates the proportion of income due to non-operating activities. It allows bifurcating the peripheral income and expenses from the mainstream income from the company’s core operations. It allows the stakeholders to compare the pure operating performance of the company and draw a comparison across the peers.

- From the entity’s point of view, reporting such income and expenses shows that the entity has nothing to hide. It establishes a transparent image of the entity, and all the stakeholders, including employees and investors, feel more comfortable taking the risk along with the entity’s growth plans. So, it is necessary to find out non operating income.

- Reporting the non-operating expenses also represent the non-core activities that can be cut down in dire need. Such line items show value in the entity’s income statement.

- It also helps the stakeholder assess more realistic figures instead of forgetting them and making plans based on fictitious numbers.

Disadvantages

- The non operating income formula. It does not reflect the entity’s operating performance as it comprises non-core business transactions. It may represent a false impression due to one-time events. Some companies may use it to inflate or deflate the profit to pay fewer taxes or lure investors into raising money from the market.

- Companies may disguise such transactions under other heads to manipulate the bottom line of the entity’s income statement. Investors should be cautious while analyzing line items arising from the non-core business transaction.

- Reporting of net operating income and expenses can be counter-effective as well as companies with a higher level of net operating income are regarded as having poorer earnings quality.

- It does not have any significance in measuring the operating prowess of the entity and hence may only serve as a line item that needs to be analyzed in isolation as it is derived from non-core activities that do not form the mainstream income for the entity.

Non Operating Income Vs Operating Income

Non operating income are generated from activities not related to the business and operating income is generated from the core business operation. Let us look at the differences between them.

| Non Operating Income | Operating Income |

|---|---|

| Generated from activities not related to business. | Generated from activities related to business. |

| It is a non-operatng income. | It is the earning before interest and tax. |

| Gain due to investment in foreign currency, dividend from associate companies, etc. | Gain after selling the products and services. |

| It is not very useful in taking company performance related decisions. | It is used in management decision making. |

Recommended Articles

This has been a guide to what is Non-Operating Income. We explain it with example, formula, list, differences with operating income & advantages. You may learn more about financing from the following articles –