Part of our Income Statement guide

What are Non-Recurring Items?

Non-recurring items are those sets of entries that are found in the income statement that are unusual and are not expected during the regular business operations; examples of which include gains or loss from the sale of assets, impairment costs, restructuring costs, and losses in lawsuits, inventory write-off, etc.

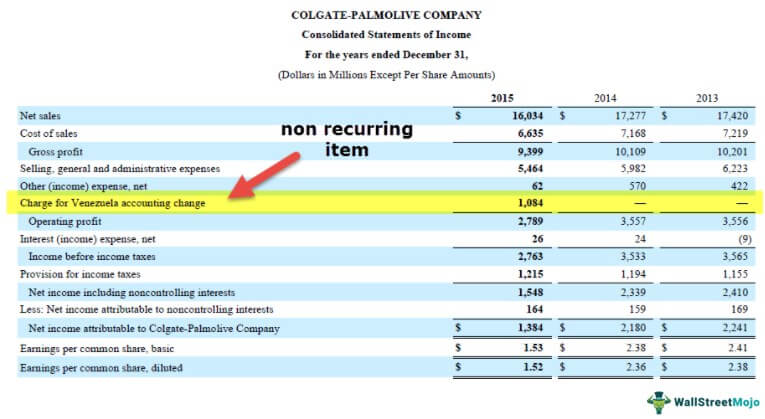

Let us look at the Income statement of Colgate above. In 2015, there was a charge for Venezuela’s accounting change.

If you notice the item highlighted above, we see that the Operating profit decreases significantly due to the presence of this item. Also, this item is not present in the other years (2014 and 2013). This item is nothing but a Non Recurring item, and it can have severe implications on Financial analysis.

Examples of Non-Recurring Items

Here are some cases when Non-recurring items have affected profit favorably or adversely. The companies referred to in these examples are hypothetical.

- XYZ India Bank: The bank reported a drop of 65% in net profit for the September 2015 quarter due to higher provisioning to cover pension, gratuity, and loan losses arising from a higher NPA %.

- ABC Pharmaceuticals Ltd: The Company reported a net loss of $1000 million for the March 2014 quarter though its revenue grew by 30 %. This loss was attributable to impairment loss, in which the company took on its South African arm’s goodwill and other intangible assets of its South African arm.

- XYZ Overseas: The Company reported a growth of 15% in y-o-y revenue, but being an import-export player, it got exposed to currency volatility, which resulted in a loss of $100 million as the net profit dipped by 20%.

- KKK Group: The Company’s December quarter for 2015 showed a growth of 150% in y-o-y profit. There was a sale of an equity stake in one of its subsidiaries within the same period. If we exclude the gains from the equity stake, the actual net profit rose just 20 %.

- Corp PPP Ltd.: The Company was the market leader in the FMCG industry in the US. It reported a profit of 11% in the quarter of December 2015, even after incurring a loss of $150 million due to a one-time gain of $400 million that it recorded from property disposal within the same financial year.

- MMM Associates: The company reported a gain of 8.5% in its revenue y-o-y for 2015, but it suffered a loss as a result of the expropriation of its property in Ireland by the local government. It brought down its Net income to just 3.75% more than last year’s figure.

Video Explanation of Non-Recurring Items

Types of Non-Recurring Items

There are primarily four types of Non-Recurring Items; they are –

- Infrequent or Unusual Items

- Extraordinary Items (Infrequent and Unusual)

- Discontinued Operations

- Changes in Accounting Principles

We will discuss each non-recurring item type in detail.

#1 – Infrequent or Unusual Items

The first type of non-recurring item is Infrequent or Unusual Items. These items are either unusual or infrequent, but NOT BOTH. These items are reported pre-tax, whereas the other three types are reported post-tax.

Infrequent or Unusual Items Examples

- Write-offs or Write Downs of inventory or receivables

- Restructuring costs when acquiring & integrating a new company or implementing changes within an existing one

- Gain or losses from the sale of assets in subsidiaries/affiliates

- Losses incurred from a lawsuit

- The loss incurred from a plant shutdown

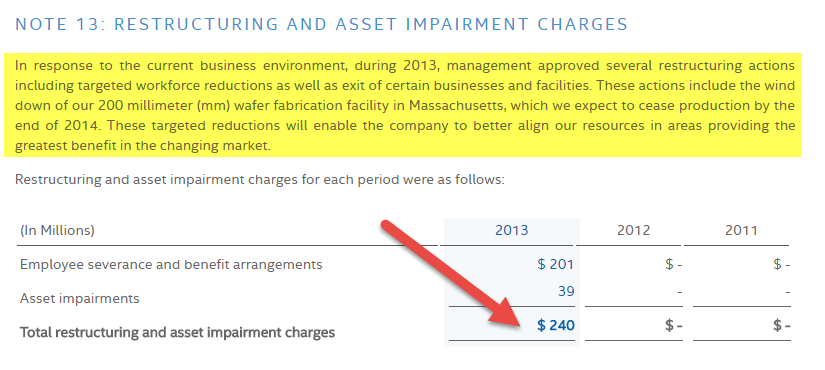

Below is an example of Restructuring and asset impairment charges in Intel.

source: Intel Website

#2 – Extraordinary Items (Infrequent and Unusual)

The second type of non-recurring item is Extraordinary Items (Infrequent or Unusual Items)

Extra-ordinary Items are both infrequent & unusual and are reported net of income tax.

Extraordinary Items Examples

- Compensation from the expropriation of the company’s property

- Uninsured losses incurred by the company as a result of natural calamities like earthquakes, floods, or Tornadoes

- Weather-related damage to a property at a place where the occurrence of weather phenomenon is less frequent

- Damage caused due to fire in a plant

- Gain or loss from early retirement of debt

- Gain on life insurance/ loss incurred on casualty

- Write-off of intangible assets

International Financial Reporting Standards (IFRS) don’t recognize the concept of extraordinary items.

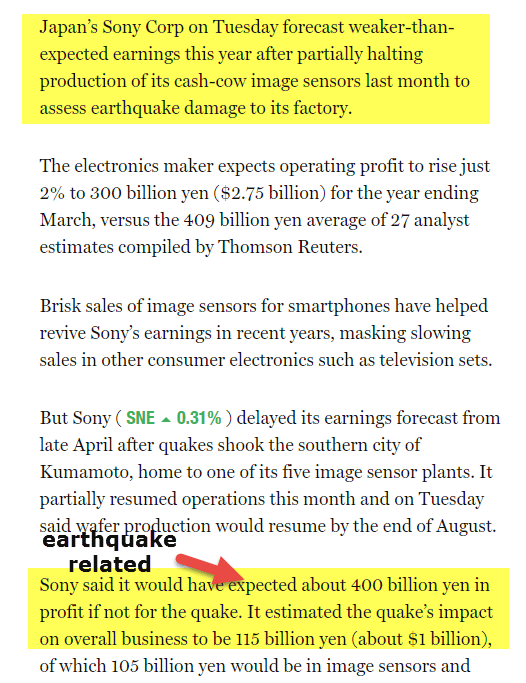

Recently, Japan’s Sony Corp estimated $1 billion as earthquake-related damages.

source: Fortune.com

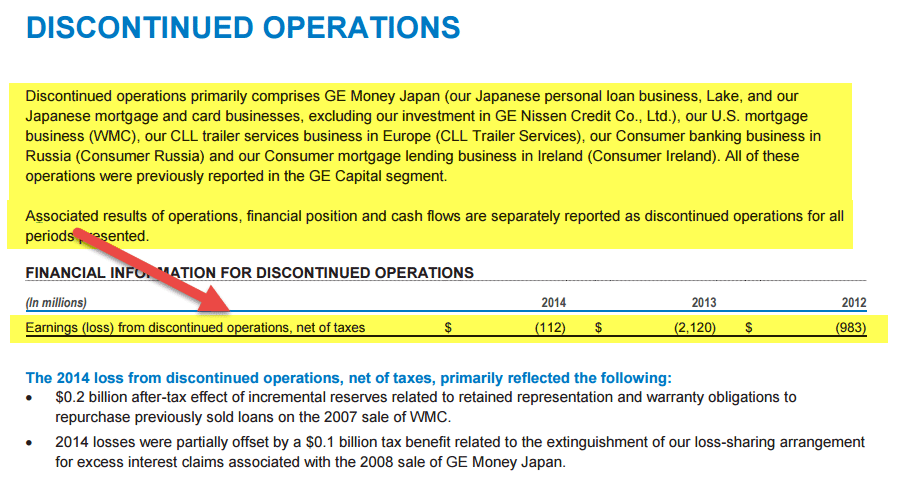

#3 – Discontinued Operations

The third type of non-recurring item is the Discontinued Operations. These non-recurring items are required to be reported in the financial statements if the operation of a part of a firm is either being held for sale or has already been disposed of. For an item to be qualified as a part of discontinued operations, two basic conditions should be fulfilled -:

- Once the component has been successfully disposed of, there is no involvement/ influence by the parent company related to financial/ operational matters within the discontinued component.

- The operations and cash flow from the disposal of the component will be eliminated from the parent’s operations.

The impact of discontinued operations appears in the Income Statement, as seen below.

Examples include -:

- A Company sells an entire product line with an agreement by the buyer to pay x% of sales as a royalty fee. The company will have no involvement/ influence in the operational/financial decision-making of the spanned-off product line.

- A company sells a product group to a buyer with which cash flows were associated and reported at that level.

Note-: if a company sells just a product from its business portfolio to a buyer, it might not qualify as a discontinued operation if the company is not reporting cash flows at that product level. Also, all contingent liabilities, including interest expenses incurred by the seller in the event of the buyer assuming any debts associated with the disposed of component, adjustments related to the selling price, and any benefit plans associated with the employees, have to be reported by the selling entity under the discontinued operation segment within the same year.

Below is an example of Discontinued Operations for GE

source: www.ge.com

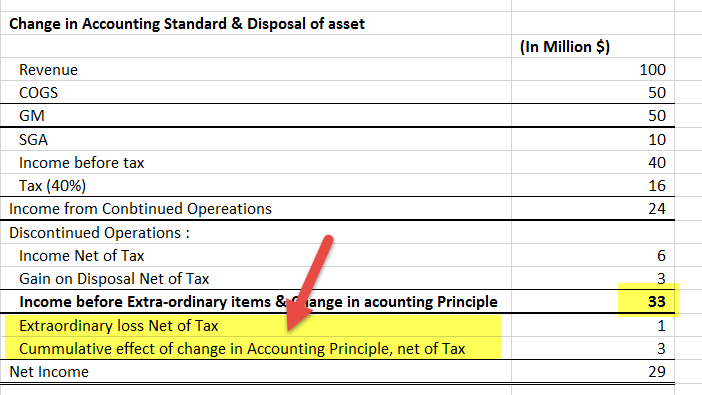

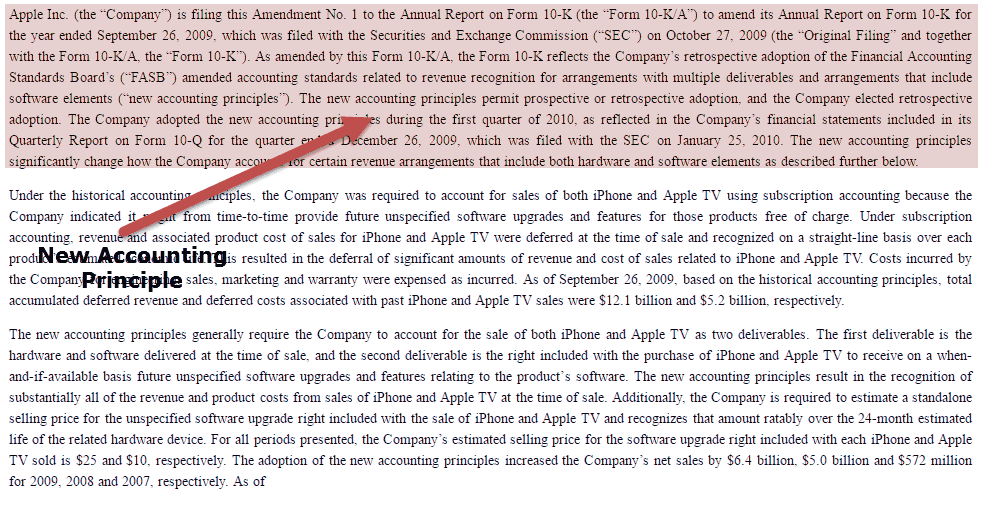

#4 – Changes in Accounting Principles

The fourth non-recurring item is the changes in Accounting Principles.

Accounting principles change when there is more than one principle available for applying to a particular financial situation. Changes should be backed by a rationale that proves their relevance. These changes have an impact not only on the current year’s financial statements but also on adjusting the prior period’s financial statements as they have to be applied retrospectively to ensure uniformity. The retrospective implementation ensures proper comparisons between the financial statements of different periods can be made. Usually, an offsetting amount is adjusted to capture the cumulative effect of such changes.

Changes in Accounting Principles Examples

- Change in inventory management principles from LIFO to FIFO or Specific identification method of inventory valuation or vice versa leads to a significant change in the inventory cost.

- Change in the depreciation method from the Straight-line method to the Sum of digits or hours of service method also leads to a significant change in how depreciation amount is reported.

In the below-mentioned example, we can see how a P&L statement should represent Extraordinary items, Gain/Loss from Changes in accounting principles, and gains from the disposal of assets. They all are captured below the line, i.e., after calculating income from Continued Operations. Such a separation helps an analyst to identify the true earnings of an organization.

source: investor.apple.com

What problem do nonrecurring items pose to Investors and Analysts?

- Investors and analysts perform financial statement analysis to estimate future earnings from current earnings.

- In reality, the profits reported in the statements are noisy, i.e., they get distorted by the inclusion of gains & losses from non-operating and non-recurring items. This problem is referred to as “the issue of Earnings Quality.”

- Many companies are increasing their Non-operating income as it helps them hide the losses they incur from their normal business operations.

- An analyst’s immediate job is to identify the main sources of revenue and expenses and the extent to which the company’s earnings depend on them.

- Non –Recurring items are an important source of distortion when identifying high-quality earnings.

- It is suggested that all Non-Operating items (including Non-Recurring items) should be segregated by the analysts so that the resulting earnings represent the true picture of future earnings from regular and continuous business activities.

- It helps in getting a more accurate valuation of a company.

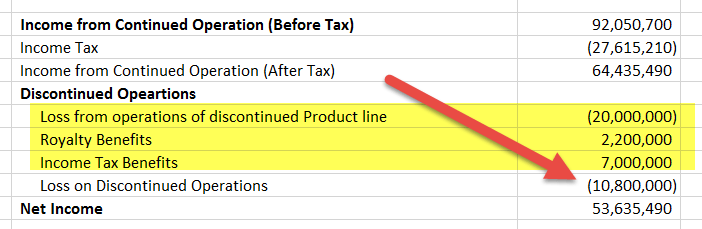

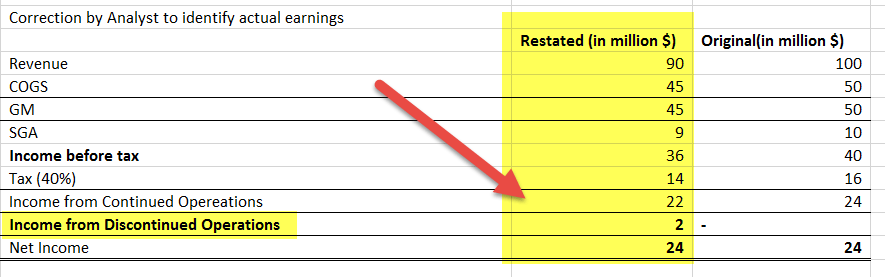

The below-mentioned example shows a re-stated Income statement due to Discontinued Operations. Though the Net Income remains unchanged, the re-stated statement allocates the income between Income from Continued Operations and Income from Discontinued Operations.

Also, Investors and analysts must always be aware of the management’s decision to make accounting changes and adjustments as they drastically impact a company’s valuation.

- Senior management is well aware of critical decisions. E.g., when to spin off a business or close a service line, and it uses this very advantage to cover up the quest for future profits by bunching up adjustments and using them at the apt time—I.e. when the earnings are expected to be the weakest.

- Also, when there is a management change, old projects are written off mainly to show big changes and improvements for future periods.

- Therefore, investors and the Security & Exchange board need to ask questions regarding the relevance of such changes and sell-offs.

- A security analyst should consider all such scenarios while carrying out a company valuation as they encapsulate hidden motives that are strong enough to distort the valuation figures.

Remedies for dealing with Non-Recurring Items

Reporting standards follow different approaches when it comes to displaying the Non-Recurring items. IFRS ignores extraordinary items completely but reports all other types, whereas GAAP reports all types of non-recurring items. These items are well explained in the footnotes of financial statements.

Generally, there are three methods to deal with non-recurring items while performing financial analysis/valuation. They are as follows -:

#1 – Allocate them within the Single Financial year

This approach talks about reporting a non-recurring item within the same financial year. Though allocating gains or losses to a single year doesn’t seem to be the right way to handle such items, it is still preferred when dealing with items that have small amounts attached to them or have very little impact on valuation matrices like EBITDA or Net Income.

#2 – Use Straight line spreading (Distributing them historically)

This approach emphasizes the principle of spreading the non-recurring items over the past accounting periods to estimate the real earning power of the company. The only demerit that it carries is that it may misrepresent the economies within a financial period

#3 – Exclude them all together

Though it seems to be the easiest of the three approaches, it involves a lot of rationalization and logical thinking by the analyst while deciding which item they should exclude. There has to be a proper justification for the exclusion, and when they do this, there must be a proper tax adjustment to nullify the gain/loss attached to the item. For example –: An early retirement of debt can be excluded from the current year.

A consistent and rational approach would be the one that emphasizes more the nature of the non-recurring item for deciding which of the three methodologies mentioned above have to be used rather than using one on a standalone basis.

It is suggested that -:

- Small items with less impact on Net Income should be accepted within a financial year.

- If an item is altogether excluded, the proper adjustment should be made while reporting the income tax.

- Items excluded from the single-year analysis should be included in a historical statement, which encompasses different accounting periods, using the straight-line spreading approach. This averages out their effect, just like capitalization averages out the revenue/expenses of a newly acquired asset (PP&E) over its useful life.

Recommended Articles

For more on Income Statement, explore these related articles from our Income Statement guide.