Part of our Expense Recognition guide

What Are The Non-Operating Expenses?

Non-operating expenses, also known as non-recurring items, are not related to a business’s principal activities and are usually stated on the company’s income statement for the period below the results from the continuing operations.

The person analyzing the company’s financial health generally removes non-operating revenues and expenses to examine the company’s year-over-year performance correctly.

Most Common Examples of Non-Operating Expenses (list)

- Lawsuit Settlements

- Losses from Investments

- Restructuring Costs

- Gains/Losses on Sale of Subsidiary/Assets

- Writedown of Inventory/Receivables

- Damages Caused to Fire

- Expropriation of the company’s property

- Losses as a result of natural calamities like earthquakes, floods, or Tornadoes

- Gain or loss from early retirement of debt

- Intangible Assets Writeoff

- Discontinued Operations

- Changes in Accounting Principles

Case Studies

Let’s see some examples, Case Studies of non–operating expenses to understand them better.

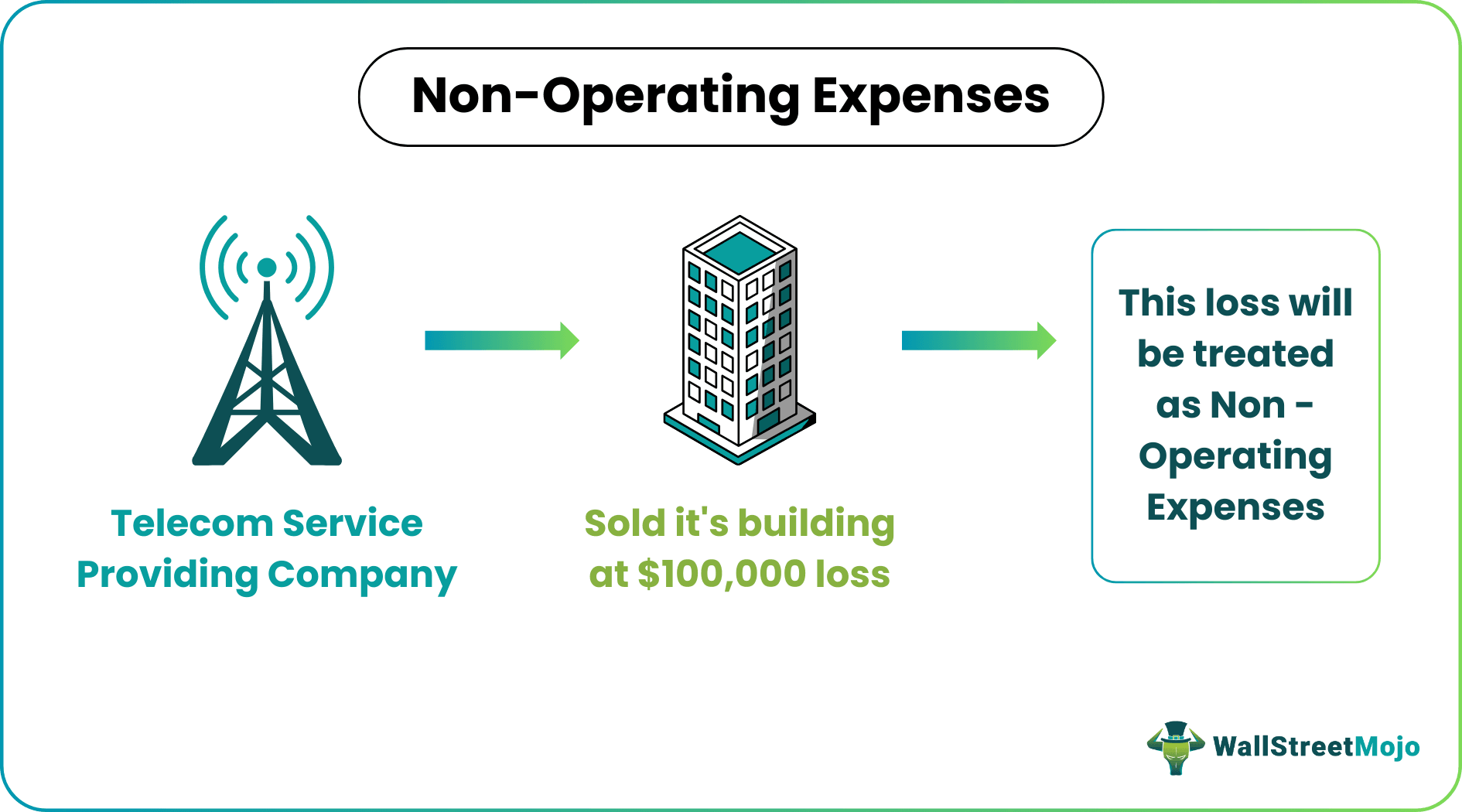

- Company A ltd is in the business of providing telecom services to the customer. During the year, company A sells one of its buildings at a $ 100,000 loss, resulting in its expense. This loss will be treated as the non–operating expense as the same does not arise because of the company’s core operations. Also, during the same period, the company paid the one-time insurance premium at the beginning of the year for the whole year to one of the insurance companies to cover various types of losses that could arise from different types of unforeseen events like floods, theft, and earthquake, etc. This amount paid for the insurance premium will also be treated as the non–operating expense as the same does not arise because of the company’s core operations. All these non–operating expenses of the company will be clubbed together. They will be shown under the head non-operating income in the income statement below the results from the continuing operations.

- A company deals in the international markets for buying and selling its products. These companies conduct transactions using foreign currency, so there are chances of an exchange rate loss or currency loss to these companies. These types of losses happen when wide currency fluctuates in the market, which is unfavorable for the company. So this leads to a currency loss for the company. These exchange rate losses or currency losses are treated as the non-operating expenses of the company. They will be clubbed together and shown under the head non-operating income in the company’s income statement below the results from the continuing operations.

Advantages

- The person analyzing the company’s financial health generally calculates the company’s non-operating expenses and deducts the same from the company’s income from its operation to examine the company’s performance and estimate its maximum potential earnings.

- When the non-expenses are calculated separately and shown separately in the income statement of the company, then it presents a clear, detailed picture of the company to all its stakeholders and helps to assess the actual performance of the business in a far better way and if any problem concerning such non-operating expenses occurs then the same could also be brought in the notice of the management of the company.

Disadvantages

- Some expenses sometimes create confusion in the mind of the person bifurcating the expense and whether they should be treated as the operating and non-operating costs. So, the person doing bifurcation of the expense should have proper knowledge about the operating expenses and expenses that are non-operating for the company then, only it is worth bifurcating the same.

- One expense can be non-operating for one company, whereas the same could be operating for another company. So, there are no standard criteria for its bifurcation. It requires the person’s time and effort to segregate the expenses properly.

Important Points

- They are the expenses that occur outside of the company’s day-to-day activities.

- Once the total of all the items of the non-operating head is derived, it will be deducted from the operation’s income to get the company’s net earnings during that period.

- These company expenses also include the one-time expenses incurred or the unusual costs.

- When the non-expenses are calculated separately and shown separately in the income statement of the company, then it presents a clear, detailed picture of the company to all its stakeholders.

Conclusion

As some of the events are uncertain, it is completely possible for companies that run a sound business to incur unusual expenses. These expenses are generally treated as non-operating expenses as these expenses do not arise because of the company’s core operations. When non-operating expenses are shown separately on its income statement, it allows the managers, investors, and other company stakeholders to assess the actual performance of the business in a far better way. Suppose any problem concerning such non-operating expenses occurs. In that case, the same could also be brought to the notice of the company’s management so that necessary corrective actions could be taken on time.

Recommended Articles

This article has been a guide to non-operating expenses and their meaning. Here we discuss the most common examples of non-operating expenses along with advantages and disadvantages. You can learn more about financing from the following articles –