What Is Business Transaction?

A business transaction is an accounting term that relates to the events that occur with third parties (i.e., customers, vendors, etc.), having monetary value and having tangible economic value to the company’s economy as well as impacting the financial position of the company.

Business transactions are the transactions entered by the assessee for the business purpose with the third party; measured into monetary consideration; recorded in the books of accounts of the assessee. The recording of these transactions into the books of accounts of the assessee depends upon the documents related to the event, which provide proper support to justify the transactions. Business transaction recording helps the assessor evaluate his business income separate from other incomes. The bifurcation helps the assessee file his income tax returns (ITR) for the required period as per the statutory norms.

- A business transaction is described as an activity involving a third party, quantifiable in monetary terms, and financially impacts the firm.

- The transaction could be a ‘Cash’ or a ‘Credit” transaction, depending on the payment terms, or an internal or external trade, depending on the parties involved.

- A small number of transactions indicates that an entity is functioning, but a large number indicates that the business is expanding.

- The transaction recording aids in separating the money derived from company operations from other income sources, including capital gains, lottery winnings, salary income, etc.

Business Transaction Explained

Business transactions are defined as the event occurring with any third party, measurable in monetary considerations, and having a financial effect on the company. For example, in the case of a manufacturing company, the company needs to buy raw materials to be used to produce finished goods. For the same, the company will enter into a transaction with the vendor, which will have a monetary value; this will affect the company’s financials.

Recording of business transaction can be considered to be the very basic thing or the foundation of any financial activity. It plays a very important role in making the business financially strong and contributing to its expansion and growth. Business transactions lead to generation of revenue through increase in sales. This revenue is the source of income that supplies funds for meeting the business expenses, be it for short term or for long term. However, this kind of transaction can also be in the nature of marketing, advertising, payment of interest, bills, etc, which results in cash outflow.

Thus, we see that this concept related to not only income but also expenses made by the company. This is a daily process of any business entity and its volume depends a lot of the size of the organization and the nature of products and services manufactured and sold by it. The larger the organization and operations, the greater is the volume of its transactions.

So, it is extremely important for the company to maintain a proper record of all these transactions so that there is no mismanagement and omission or financial records. Proper documentation and recording of business transaction in accounting leads to creation and maintenance of accurate financial details which can be referred to for future reference and also from the audit point of view.

Characteristics

Now let us look at some of the characteristics of recording of business transaction.

- These transactions are measurable in monetary terms. So there is an exchange of products or services that has some value to both the parties.

- It involves an event occurring between the organization and a third party.

- The transaction is entered for the entity, not for any individual purpose. They are commercial in nature.

- They are supported by the authorized and legitimate documents related to the event or transaction entered, e.g., in case of a sale, sale order & invoice will be considered legal documents for supporting the deal.

- It is necessary for the parties to agree to the rules, terms and conditions of the contract or transaction so that the process can be conducted. This mutual agreement has to be authorized and formalized.

- Sine the process has very significant financial implications for the business, it is important to keep a clear and transparent record of them in the books of accounts.

- The accounting method followed in the concept is dual entry, where there is a debit and a credit. Each transaction has at least two effects or affects two accounts in the business. This follows the accounting equation of assets equal liability and equity.

- Due to the transaction, there is a change in the financial condition of the parties who are involved in the business. Thus, due to sale of goods, the revenue of the selling party will increase and inventory will fall, and the opposite will happen for the buying party.

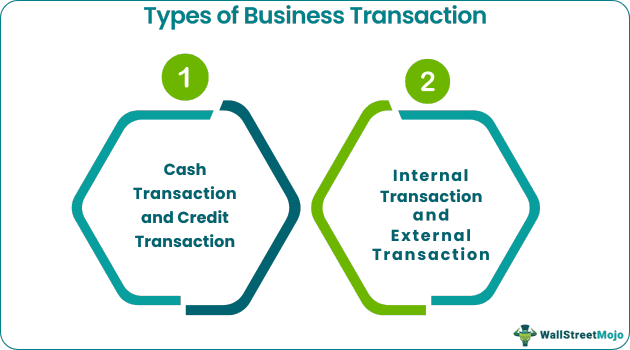

Types

These transactions can be classified on two bases. These bases are described as follows:

#1 – Cash Transaction and Credit Transaction

- Cash Transaction: A transaction in which cash is involved means payment is received or paid at the time of occurrence of the deal. For example, Mr. A paid Rs.10000 as the rent of his premises in cash. This is a cash transaction because it involves cash payment at the transaction time. Similarly, Mr. A bought stationery for Rs. 5000 and paid cash.

- Credit Transaction: In credit transactions, cash is not involved at the transaction time; instead, the consideration paid is after a particular time (termed as credit period). For example, Mr. A sold goods to a customer on a credit basis and provided him a credit period of 30 days. So in this transaction, cash is not involved at the time of sale, but the customer will pay it after a credit period of 30 days.

#2 – Internal Transaction and External Transaction

- Internal Transaction: There is no external party involved in an internal transaction. These transactions do not involve any exchange in value with the other external party, but it has monetary terms or value, i.e., impairment of fixed asset. It reduces the value of fixed assets.

- External Transaction: In an external transaction, two or more parties are involved in the transaction. They are the usual transactions that occur daily. For example, purchasing goods, sales, rent expenses, electricity expenses paid, etc.

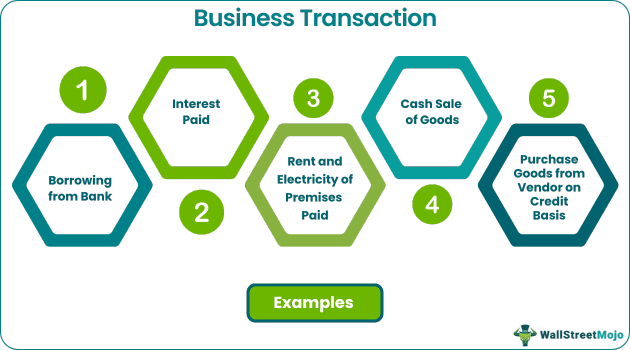

Examples

Let us understand the concept of business transaction in accounting with the help of some suitable examples.

#1 – Borrowing from Bank

This transaction will affect two accounts one is Cash/bank Account (Assets), and the second is Loan Account (Liability)

#2 – Purchase Goods from Vendor on Credit Basis

This transaction will have an effect on two accounts one is Purchase Account, and the second is Vendor Account (Liability); this transaction will also affect the inventory as the inventory stock will increase (Assets).

#3 – Rent and Electricity of Premises Paid

This transaction will affect two accounts, one is Cash/bank Account (Assets), and the second is the Rent and electricity Account (Expenses).

#4 – Cash Sale of Goods

This transaction will affect two accounts; one is Cash/bank Account (Assets), and the second is a Sale Account (Income); this transaction will also affect inventory as inventory stock will decrease (Assets).

#5 – Interest Paid

This transaction will affect two accounts, one is Cash/bank Account (Assets), and the second is an interest Account (Expenses).

Importance

They are day-to-day transactions, and they may occur once a year or more than once a year. But while running a business, it is bound to be multiple times. Because if there is no transaction, then it means that the entity is not working & it is at an obsolete level and will shut down eventually. So having these transactions implies the entity is working.

It also depends on transactions and whether the entity is a downside or growing. If there are few transactions in the entity, it means it is working, but if there are many transactions in the entity, it means it is growing. So these transactions keep the company in existence and larger & frequently, the analysis of business transaction that may relate to more competitive business practices and business interaction with the external and internal environment of the business.

Advantages

The concept has both advantages and disadvantages. Let us look at the advantages first.

- Recording these transactions helps evaluate the effectiveness of business and profit generation by the entity during the respective period.

- The analysis of business transaction and recording helps bifurcate the income produced from the business activities from the other incomes, which may be clubbed with a capital gain, lottery income, salary income, etc.

- They are recorded, and in the year-end or for a specified period, Final Accounts are prepared through them to determine the assessee’s financial position.

- It helps the assessee to record and file his income tax returns as per statutory norms with a proper bifurcation of his income & expenditure into the appropriate heads.

Disadvantages

Some disadvantages of the concept will be as follows.

- Since the process involves multiple parties, it can be considered a complex process with various rules, terms and conditions and also some legal complexities.

- It is important to maintain proper documentation and meet the legal requirements which can be time consuming, costly and involve a lot of procedures.

- Due to a high volume and complex process, there is a chance of misstatement and fraud from the parties involved. There may be misrepresentation of values and the terms of the contract may not be honoured in all cases.

- From the above point we can also conclude that there is always a possibility of legal disputes, financial losses and loss of market reputation for the parties to the transaction.

- It requires some cost to be incurred for the parties. These costs or fees are in the form of administrative expenses, transaction and legal fees, or any other types of cost that affect the profit earning capacity of the parties to the contract.

- There is a possibility of the parties facing disagreements and between themselves which may lead to misunderstandings or disputes. Settling such matters may n=be time consuming and expensive.

- There may be credit issues in the process. The seller may not be in a financial position to make payment on time leading to default and loss of reputation in the market. On the other hand, the buyer will not get the money on time, leading to bad debt and fall in revenue. These result in financial losses.

- If the transactions are not properly maintained and recorded the financial statements are affected in a negative way. Such financial statement data which are widely used by the analysts and investors will be misguided and may take incorrect financial and investment decisions.

However, inspite of having many disadvantages, the concept of national and international business transaction is the basis of every company which contributes to its overall success.

Business Transactions Vs Investment Transactions

Both the above are two types of transactions involving parties who enter into a contract either for the purpose of business or investment. However, there are some differences between them, as follows:

- Business Transactions are usually the transactions entered in by the organization and are like trade, commerce, or manufacturing. Investment transactions are entered into to sell or purchase marketable securities and other assets that may or may not be connected directly to the business.

- National and international business transaction generate income, which is the company’s income and taxable under the “Profit & Gain from the Business property.” In contrast, Investment transactions generate a capital gain, which is taxable under the heading “Income from Capital Gains.”

- Suppose the purchase & sale of an asset is the same as the assessee’s general trading business. In that case, these transactions will be considered business transactions, whereas if the purchase & sale of an asset is an independent activity against the ordinary course of business. The transactions will be considered investment transactions.

- In general, the frequency of these transactions is huge in numbers as they are entered in the course of business compared to the investment transactions entered as they are independent transactions.

Frequently Asked Questions (FAQs)

How are business transactions recorded?

Business transactions are recorded through a thorough book-keeping process involving journal entries, ledger accounts, trial balances, income statements, and the balance sheet. These transactions are recorded using a double-entry system of accounting which ensures that the total amount of debt equals the total amount of credits and helps maintain the accuracy and completeness of the accounting records.

Why is documentation important in business transactions?

Documentation is essential in these transactions for several reasons, including legal protection, clarity and understanding, record-keeping, and compliance. In addition, documentation ensures that these transactions are conducted smoothly, legally, and effectively.

Why do governments tax business transactions?

Government taxes these transactions for various reasons, including revenue generation, supporting economic policy, redistribution of wealth, and serving as a form of regulation.

Recommended Articles

This has been a guide to what is Business Transaction. We explain it with example, types, characteristics, advantages, disadvantages & importance. You may learn more about our articles below on accounting –