Part of our Mergers & Acquisitions guide

Investment in Associates Definition

Investment in associate refers to the investment in an entity in which the investor has significant influence but does not have full control like a parent and a subsidiary relationship. Usually, the investor has a significant impact when it has 20% to 50% of shares of another entity.

- Investment in the associate is an entity where the investor has a significant effect but does not have complete regulation like a parent and a subsidiary relationship. Generally, the investor has a significant impact when it has another entity’s 20% to 50% of shares.

- Accounting for investment in associates is conducted using the equity method. In the equity method, a 100% consolidation is not used. Instead, the proportion of shares owned by the investor is shown as an investment in accounting.

- Investment in associates is typical for companies to utilize the investment to take a lesser stake in another company.

Accounting for Investment in Associates

Accounting for investment in associates is done using the equity method. In the equity method, there is not a 100% consolidation used. Instead, the proportion of shares owned by the investor will be shown as an investment in accounting.

When an investor takes more shares in associates than in the investor’s balance sheet, it is recorded as an “increase in associates,” and the same amount reduces cash. The dividend from the associate is shown as an increase in money for the investor. To record the proportion of the net income of an associate, the investment revenue of the investor gets credit, and investment in the associate account gets debited.

Example of Investment in Associates

Below are some of the basic to advanced examples of investment in associates.

Basic Example

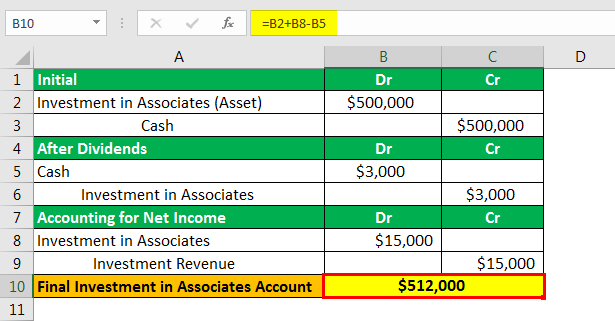

Suppose ABC Corp. has purchased 30% shares of XYZ Co. That means ABC Corp. has significant influence over XYZ Co. Therefore, XYZ Co. can be treated as an associate of ABC Corp. The value of 30% shares is $500,000. So, while making a purchase, below will be an accounting transaction for ABC Corp.

After 6 months, XYZ Co. declares $10,000 dividends to its shareholders. That means ABC Corp. will receive 30% of dividends or $3,000. Below will be accounting entries for the same: –

XYZ Co. also declares a net income of $50,000. Accordingly, ABC Corp. will debit 30% of $50,000 in its “Investment in Associates” account while crediting the same amount as “Investment Revenue” in its income statement.

The ending balance of ABC Corp. “Investments in Associates” account increased to $512,000.

Practical Example – Nestle’s Investment in Associates

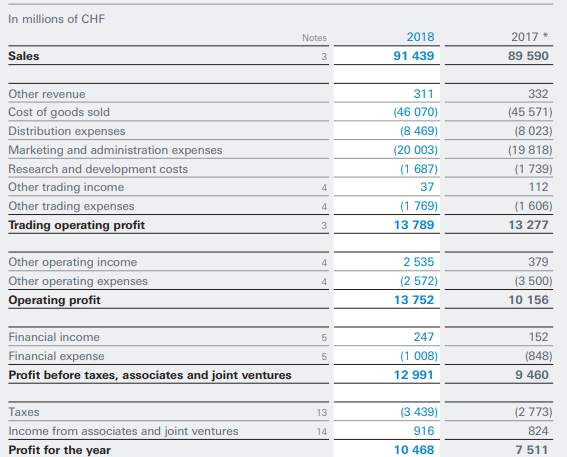

Nestle is a Swiss multinational company headquartered in Switzerland. Nestle, the largest food company, globally had around CHF 91.43 billion in revenue in 2018. Below is the income statement of Nestle as per the 2018 annual report.

Source: www.nestle.com

We can see that income from associates has increased from CHF 824 million to CHF 916 million.

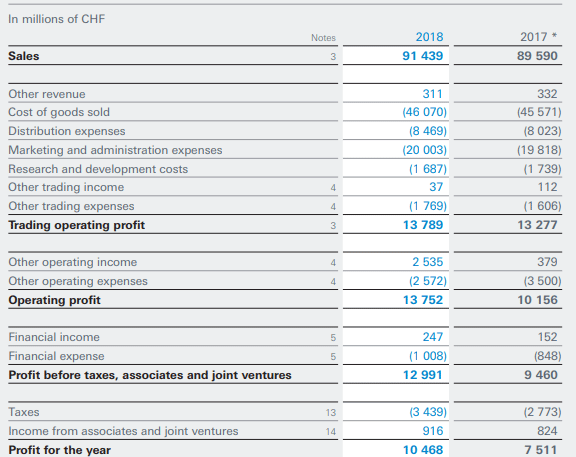

Source:www.nestle.com

Also, as per the balance, their Investment in Associates account has gone down from CHF 11.6 billion to CHF 10.8 billion.

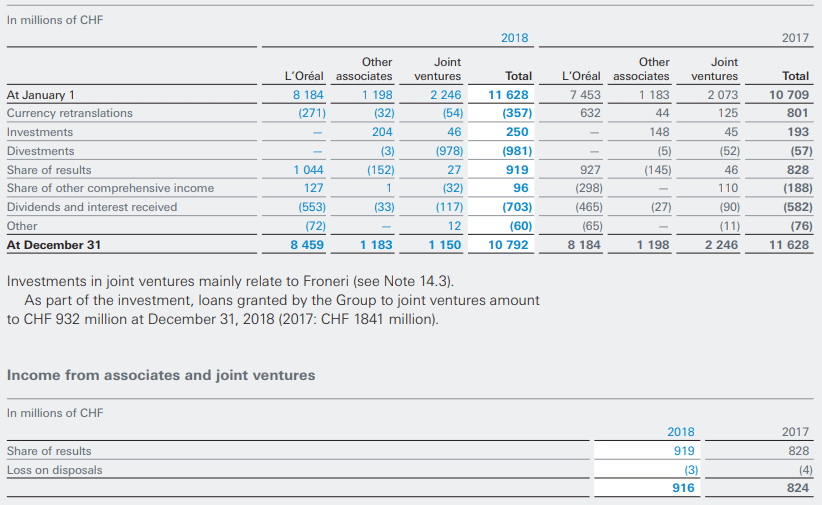

Below is the more detailed information on associates for Nestle: –

Source: www.nestle.com

In L’Oreal, Nestle has 23% shares after eliminating its treasury shares. Nestle holds another number of associates also, but that is not material. Major factors in investment in associates are share of results with CHF 919 million.

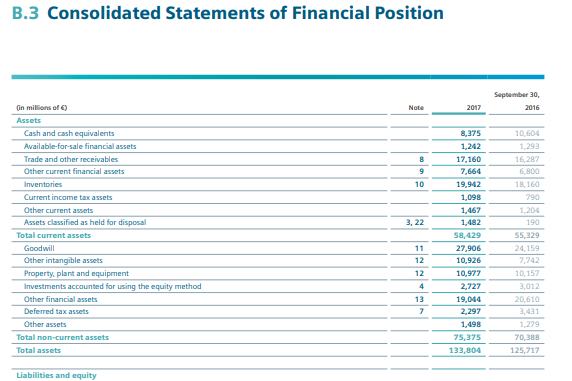

Practical Example – Siemens AG

Siemens AG is a German multinational company headquartered in Berlin and Munich. Siemens AG mainly operates in energy, healthcare, and infrastructure. Their revenue is around €83 bn as per the 2018 annual report. Below is the balance sheet snippet for Siemens AG, which shows its investment in associates, which is shown under “Investment in Accounted for using the equity method.”

Source: siemens.com

As we can see, their associates’ investment has changed from €3 billion to €2.7 billion.

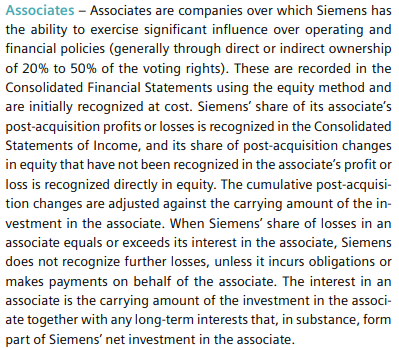

We can see below their definition of associates also.

Source: siemens.com

As we have mentioned above, they treat the investment as associates in which they have 20% to 50% shares, and they are using the equity method to account that investment is recognized at cost.

Advantages

- With these investments, investors show an accurate and reliable income balance. In addition, it shows the percentage of earnings from its investment.

- Since the investor shows the only percent of income or investment in an associate, it is easy to reconcile the accounts.

Disadvantages

- It is a bit complex to do the accounting for this method. A lot of time is required to gather and analyze, evaluate the figures, and get the correct information.

- The investor cannot show dividends from associates as revenue. It can only be treated as a “reduction to investment” amount and not as a dividend income.

Important Points to Note about Change in Investment in Associates

- A company is treated as an associate when the share in investee is between 20% and 50%.

- The equity method is used to do the accounting.

- Investment is treated as an asset, and only the percentage of shares bought is treated as an investment.

- Dividends are treated as a change in investment, not the dividend revenue.

Conclusion

Investment in associates is common for companies to use their investment to take a lesser stake in another company. The equity method is useful for the accounting process for these investments. Though companies can show the net income of the associate company as part of their revenue, dividend income won’t be part of it, and it would be a reduction in the “investment in associate” asset.

Frequently Asked Questions (FAQs)

How do you test for impairment of investment in associates?

Suppose the investment carrying amount in an associate or joint venture increases its recoverable amount. As a result, an impairment loss is identified. However, the loss is allocated to the investment as a whole and not to the underlying assets of the investee that make up the carrying amount of the investment.

Is investment in associates a current asset?

Investments in associates using the equity method are classified as non-current assets. As a result, the investor’s profit or loss shares of associates and the carrying amount of those investments are separately revealed.

Why subtract investment in associates from enterprise value?

The minority interest value is added because it shows the claim on assets consolidated into the firm. The value of associate companies is deducted as it shows the claim on assets consolidated into other firms.

How do you account for investment in associates?

Investments in associates using the equity method must be classified as long-term investments and revealed distinct in the consolidated balance sheet. Accordingly, the investor’s share of the profits or losses of such assets should be disclosed separately in the consolidated statement of profit and loss.

Recommended Articles

This article has been a guide to investment in associates and its definition. Here, we discuss how accounting for investments in associates is done along with examples, advantages, and disadvantages. You can learn more about financing from the following articles: –