Part of our Profitability Ratios guide

Net Operating Income Meaning

Net Operating Income (NOI) is a measure of profitability that represents the amount the company has earned from its core operations and is calculated by deducting operating expenses from operating revenue. It excludes non-operating expenses such as loss on the sale of a capital asset, interest, tax expenses, etc.

Net Operating Income Formula Excel Template

Download Excel Template

This is different from that of net income, as net income is bottom-line profit calculated after considering all expenses and revenues. Extraordinary gains and losses, which are one time, Interest, and taxes, can distort the net income sometimes, which will provide a different picture of the business than it is in reality.

- Net Operating income reflects the effectiveness of the business’s core operating performance.

- It does not include revenue from the activities which are not directly related to the business, such as income from investment, gain on the sale of a capital asset, etc.

- The concept of net operating income is essential for the creditors and the investors of the business as it gives them a clear picture of the working of the business that how effectively the operations of the organization is performed and how much income is generated from the core business activities of the business.

Net Operating Income Explained

Net operating income is a profitability metric used to calculate the gains made from an income generating property. It is calculated by deducting operating expenses of the property from the operating revenue.

The parties related to the business like creditors, investors, and the management use the net operating income calculator measure to analyze and evaluate the profitability and efficiency of operations, prospects, and overall health of the business. The higher the company’s net operating income, the higher the chances of the company surviving in the future and paying debts and returns to the lenders and investors, respectively.

The increasing trend in this number of operating income indicates that there is more scope for the company to grow in the future and vice versa. Creditors and investors always want to deal with the increasing trend of the company as the possibility of getting a higher return is higher in that type of business.

Formula

The formula to derive the profits made from a revenue making property and to employ the net operating income calculator is:

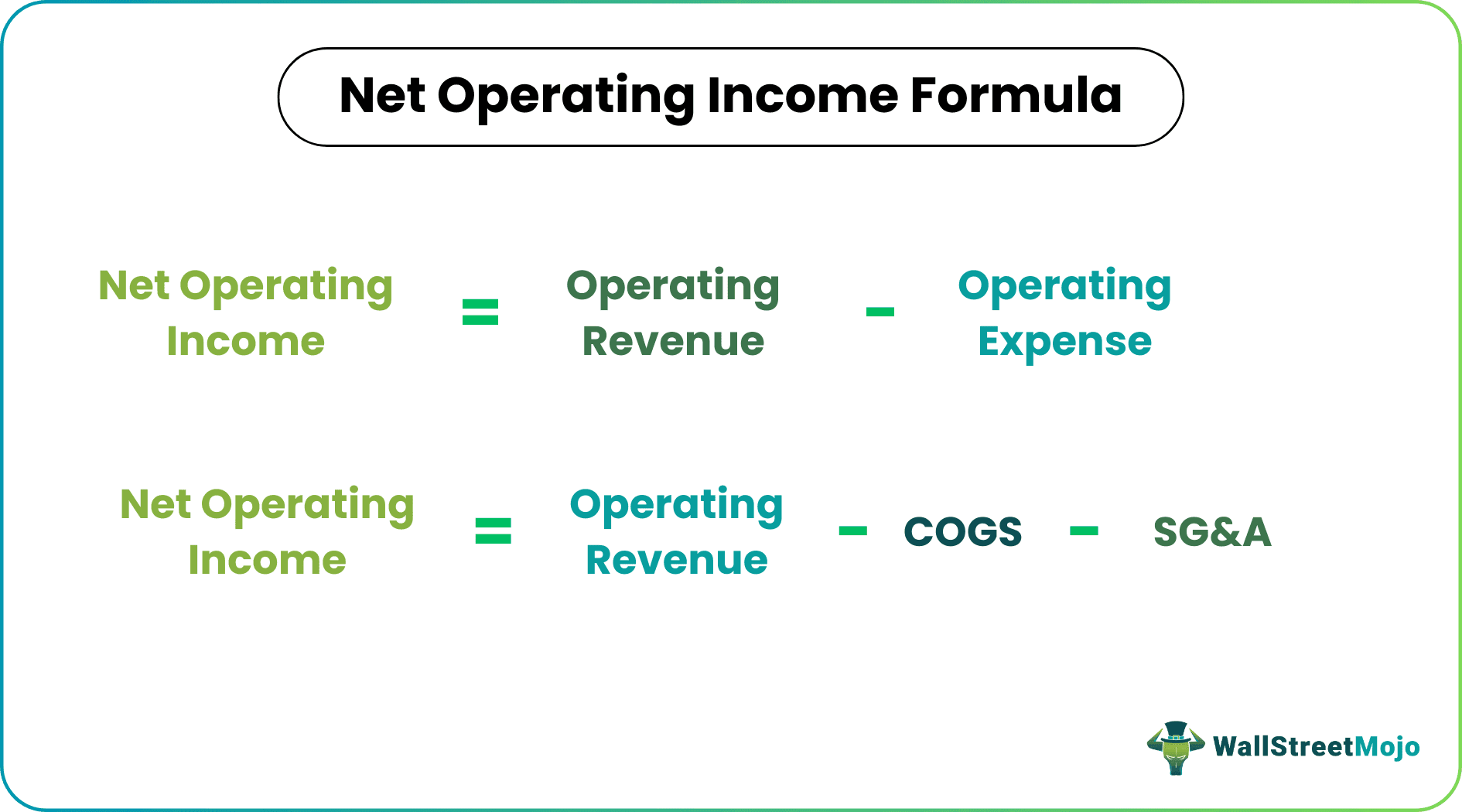

- NOI Formula = Operating Revenue – Operating Expense

- NOI Formula = Operating Revenue – COGS – SG&A

Operating Revenue

Operating revenue is the revenue generated from day to day operations of a business. We can take the example of a company involved in the business of selling mobile phones. Now in a financial year, a company has sold mobiles worth $500,000 and equipment at $100,000, earning a profit of $5000. In the given case, only $500,000 is operating revenue as it is only related to the core activity of the business, and profit on the sale of equipment is not a part of operating revenue. The operating revenue doesn’t include income from extraordinary activities.

Operating expenses

Operating expenses include all the costs or expenses which are directly related to the business activity. In other words, operating expenses include all types of cost, which is required to be incurred in running the day to day operations of the business. Some of the examples of operating expenses are Salary & Wages, Raw material cost, Power & fuel, Rent, utilities, Freight and postage, and advertising. Operating Expenses exclude Income taxes, losses from the sale of assets, interest expense, etc. For instance, suppose you paid $300,000 in cost of goods sold, $15,000 in wages, $25,000 in Rent, $4,000 in utilities, $1,500 in interest and $28,000 in income taxes. Your total operating expenses are $344,000, which excludes the interest and income taxes.

Revenue vs Income Explained in Video

How To Calculate?

Let us understand the steps to calculate the Net Operating Income theory with the help of Colgate Example.

If there are revenue sources other than the core operations of the business, then you must exclude those items.

- Find the Operating Revenue –

Identify the core revenue of the business as given in the income statement. Then, read through the annual report to see what else is included in the company’s Sales / Net Sales figures.We note that sales of Colgate were $16,034 million in 2015 and $17,277 million in 2014.

- Remove other revenues from these items –

If there are revenue sources other than the core operations of the business, then you must exclude those items.In Colgate, we don’t have any such items.

- Find the Operating Expense -Operating Expense can be easily identified from the income statement. It is the total Cost of Goods Sold and Selling, General, and Admin expenses. Any other expense that is directly related to the business should be included. All other expenses should be excluded from the net operating income calculation formula.

In Colgate, we note thatOperating Expense (2015) = COGS + SGA = $6,635 + $5,464 = $12,099 millionOperating Expense (2015) = COGS + SGA = $7,168 + $5,982 = $13,150 million

- Remove other expenses not related to the business -Other expenses unrelated to the business should be not included in the calculation of Net Operating Income

In Colgate, there is another expense of $62 million in 2015 and $570 million in 2014, respectively. In addition, do not include the non-recurring charges of Venezuela accounting changes of $1084 million

- Use NOI formula

Colgate’s NOI (2015) = $16,034 million – $12,099 million = $3,935 millionColgate’s NOI (2014) = $17,277 million – $13,150 million = $4,127 million

Example

Let us understand the concept of net operating income theory in depth with the help of an example.

Let’s take the example of a pizza outlet owned by Mr. X in California that cooks the best pizza in their area. Mr. X is working on the refinancing of his current loans with a nearby bank, so he needs to calculate NOI.

After analyzing the accounting system, Mr. X analysis the following income and expenses incurred in the business:

- Sales: $180,000

- Cost of goods sold: $40,000

- Salary & Wages: $35,000

- Rent: $15,000

- Insurance: $20,000

There has been a fire in the pizza outlet during the financial year. Loss on fire estimated to be $45000. Unfortunately, the insurance company failed to cover all the damages. Therefore, Mr. X would calculate his operating income like this:

Now Mr. X will deduct all the expenses from the revenue, getting $70,000 as a profit from operations. Here the loss on fire of $45,000 is not included because it is an extraordinary business loss, not an operating activity. Therefore, Mr. X will report $70,000 as his net operating income, not $25000 ($70,000- $45000).

Recommended Articles

This has been a guide to Net Operating Income (NOI) meaning. Here we explain its formula, hoe to calculate, examples, and its applications. You may learn more about our articles below on accounting –