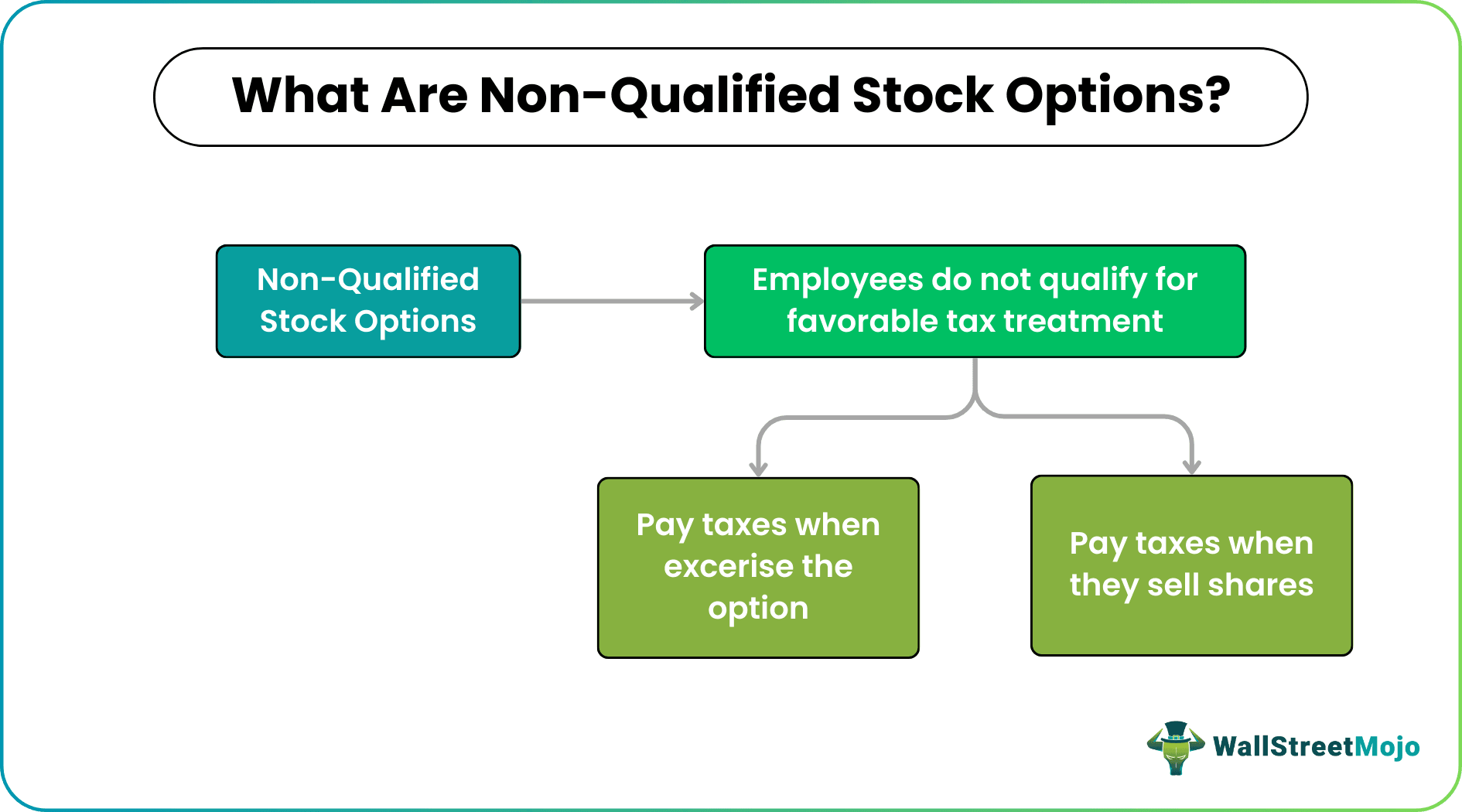

What Are Non-Qualified Stock Options?

A non-qualified stock option is an employee stock option wherein the employee pays ordinary income tax on the difference between the grant price and the fair market price at which he exercises the option.

A non-qualified stock option is one way to reward employees. It also gives greater flexibility to recognize the contributions of non-employees. It is a valuable part of an employee compensation package, especially if the company’s stock has been soaring of late. Non-qualified stock options are also very relevant for the employer. The amount of the compensation element is generally deductible as a compensation expense.

How Do Non-Qualified Stock Options Work?

Non-qualified stock options definition states that they are the set of ESOPS in which the employee is required to pay income tax at the ordinary rate of income tax on the difference amount of the grant price and the price at which the employee exercises the option.

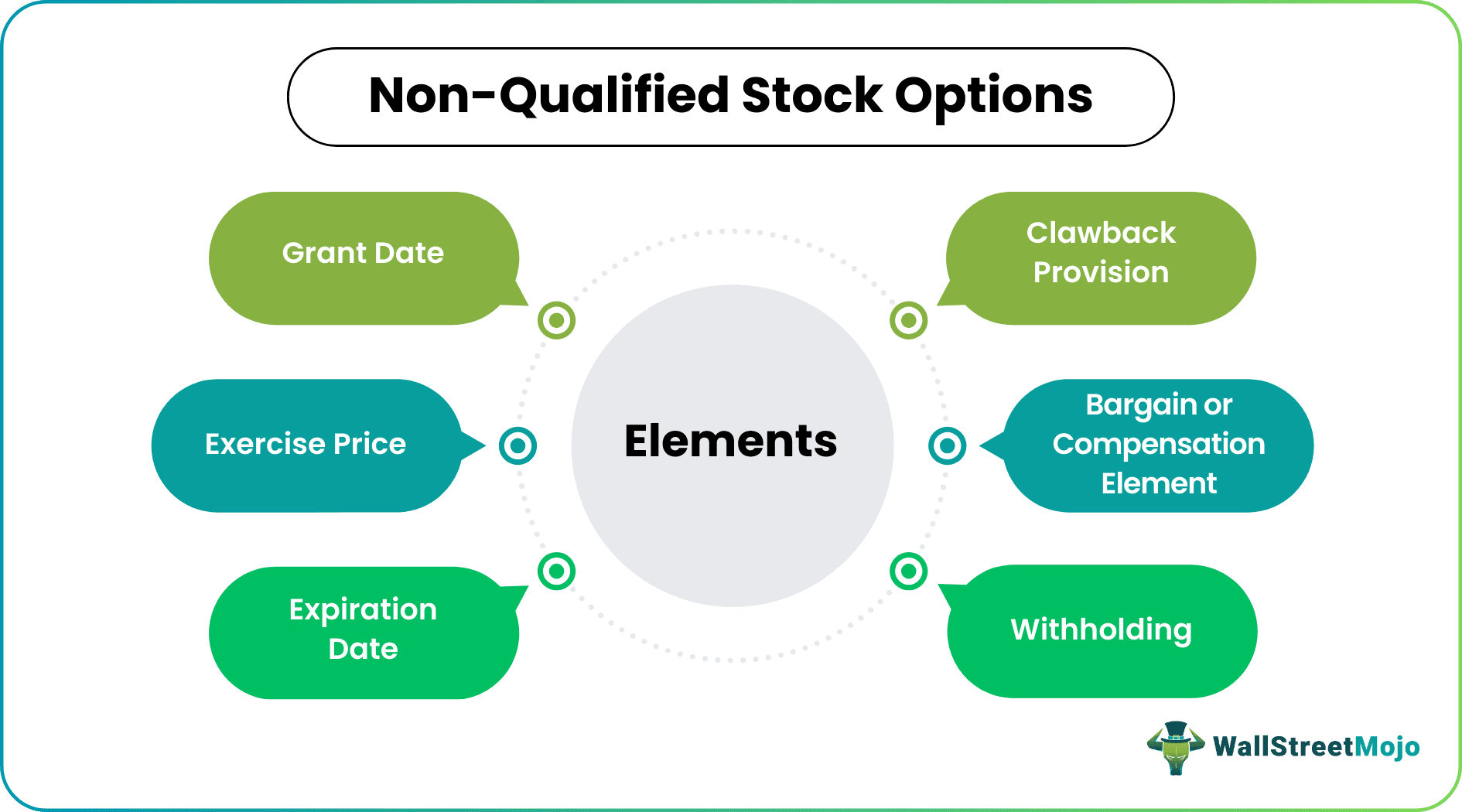

The key elements of such options:

- #1 – Grant Date – It is the date when the employee receives the option to buy the stock.

- #2 -Exercise Price – The price at which the employee can buy the stock from the company.

- #3 – Expiration Date – The last date to exercise the option.

- #4 – Clawback Provision – The clawback provision gives the right to cancel the option given to the employee.

- #5 – Bargain or Compensation Element – The difference between the exercise price and the stock’s market value.

- #6 – Withholding – The company must withhold a certain amount of cash. It is mainly to cover federal and state income tax withholding and the employee’s share of employment taxes.

Examples

Below are some examples of non-qualified stock options:

Example #1

A.B Food is a UK-based company listed on the London Stock Exchange. Assume the share price of the company is $10. It grants an NQSO at a $10 exercise price. The share value is $20 after one year.

Employees have the following options:

- Exercise, sell immediately: Immediately sell the stock for $20. They will have $10 per share as income.

- Exercise, hold for more than a year, sell: If they sell it for $25, the bargain element is $10 (fair value- exercise price) and is taxable when exercised. They will have a $5 long-term capital gain (S.P of $25-Value at exercise date $20).

- Exercise, hold for less than 12 months, then sell: Here, $5 gain becomes a short-term capital gain.

- Employees can exercise an option even if the value is less than the exercise price. Usually, it happens when there is a chance to increase value in the future, but the expiration date is nearing.

Example #2

Mr. Bill is an employee of a US-based company named Marvell Technology Group Ltd. He receives options on a stock that is actively traded on NASDAQ.

He purchased 1,000 shares of company stock and was granted the option to purchase stock. It’s taxable only when he exercises those options and later sells the stock he purchased.

Tax Implications

Here are the four scenarios based on Example – 2 above to depict the non-qualified stock options tax treatment more clearly:

1. Exercises then hold

The exercise date is 30th June 2017. Bill exercised the option for $20. The current price is $40. It has not yet sold. There are 100 shares in total.

The compensation element can be calculated as:

Difference between the Exercise Price and Current price multiplied by several shares bought.

$(40 – 20) = $(20 x 100)= $2,000.

Now, the employer will include this compensation element amount ($2,000). Therefore, Mr. Bill will be taxed on the compensation element.

2. Exercises and sells the shares on the same day

The exercise date and sales day are the same as 30th June 2017. The exercise price is $20. The current market price is $40 and the sales price. And $10 is a commission paid for sales. There are 100 shares in total.

The compensation element will be the same as $2,000, and the employer will include $2,000 in income.

He sold the stock right after he bought it; the sale counts as short-term, and $10 is a short-term capital loss.

He sold the stock for $4,490 that he purchased for only $2,500.

3 – Exercises and sells them within a year

The exercise date is 30th June 2017. The exercise price is $20.

The current market price is $40. He sells the shares before 30th June 2018 at $50 and $10 is the commission. So there are 100 shares in total.

The bargain element of $2,000 is taxable income. The stock sale, here, is a short-term transaction deal because he owned the stock for less than a year. The short-term capital gain is the difference, i.e., $490.

4. Exercises then sell them after more than a year

In the examples above, if the shares are sold post one year. Again, the gain will be long-term capital gain.

The bargain element is $2,000. The stock sale gain is $490. So he has to pay a marginal tax on the capital gain.

Advantages

- It’s an alternative compensation to employees, thus reducing cash compensation.

- It encourages loyalty to the company.

- Smaller and younger businesses with limited resources become a recruiting tool to make up for shortcomings in the salaries offered when hiring talent.

- It shares the risks and diversifies them in a growing business.

- It provides increased compensation when an organization can’t afford to raise salaries.

- It recognizes the contributions of key employees.

- It avoids the complexity of incentive stock options.

- It issues stock options to employees who aren’t eligible for ISO.

Disadvantages

- If cash compensation is removed, insufficient cash salaries may be an obstacle to recruiting suitable employees.

- It does not give special tax treatment to employees like ISO.

Non-Qualified Stock Options Vs Incentive Stock Options

| Basis | Incentive Stock Options | Non-Qualified Stock Options |

|---|---|---|

| Availability | Only available for employees; | It is available for employees, consultants, and advisors. |

| Tax Treatment | Qualifies for special tax treatment; | The compensation element is treated as an ordinary income in the hands of the employee. |

| Benefit for employee | Usually seen as more advantageous for the employee; | It is not advantageous to the employee as it is taxable based on a certain condition. |

| Benefit for Employer | The employer does not prefer it. | Employers prefer it because the issuer is allowed to take a tax deduction equal to the amount the recipient is required to include in his or her income. |

Recommended Articles

This article is a guide to what are Non-Qualified Stock Options. Here we explain vs incentive tax options, examples, and tax implications. You may learn more about accounting from the following articles –